Housing is certainly more expensive than in the past. I have written about this several times, including a post from last year showing that between about 2017 and 2022 housing started to get really expensive almost everywhere in the US, not just on the West Coast and Northeast (as had previously been the case). I don’t think the housing affordability crisis is in serious doubt anymore, and it can’t be explained over the past few years by increasing size and amenities, since those haven’t changed much since 2017 (though it is relevant when comparing housing prices to the 1970s).

But why did this happen? Knowing why is crucial, not merely to blame the causes, but because the policy solution is almost certainly related to the causes. I and many others have argued that supply-side restrictions, such as zoning laws, are the primary culprit. The policy solution is to reduce those restrictions. But a recent op-ed titled “Why your parents could afford a house on one salary – but you can’t on two,” the authors place the blame for housing prices (as well as the stagnation of living standards generally) on a different factor: Nixon’s 1971 “severing the dollar’s link to gold.” The authors have a book on this topic too, which I have not yet read, but they provide most of the relevant data in this short op-ed.

Does their explanation make sense? I am skeptical. Here’s why.

But as Jeremy often points out here, young adults have actually been doing pretty well at building wealth. So why are they so gloomy?

Since I’ve now aged out of the young adult category, I’m obligated to start by wondering if kids these days are just whinier, and need to quit doomscrolling and toughen up. But if I try to see things their way, here’s what I can come up with for why their pessimism could be rational:

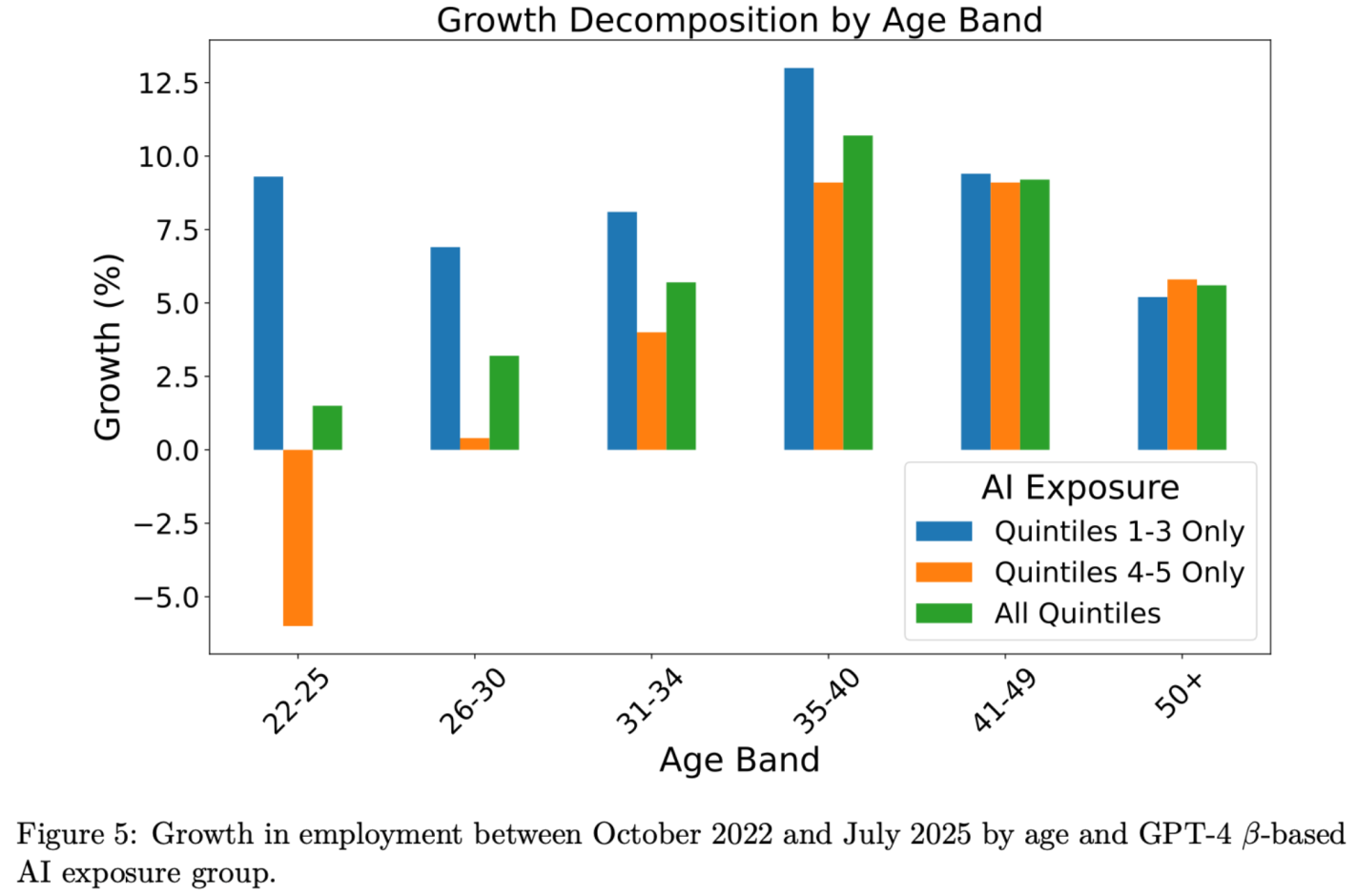

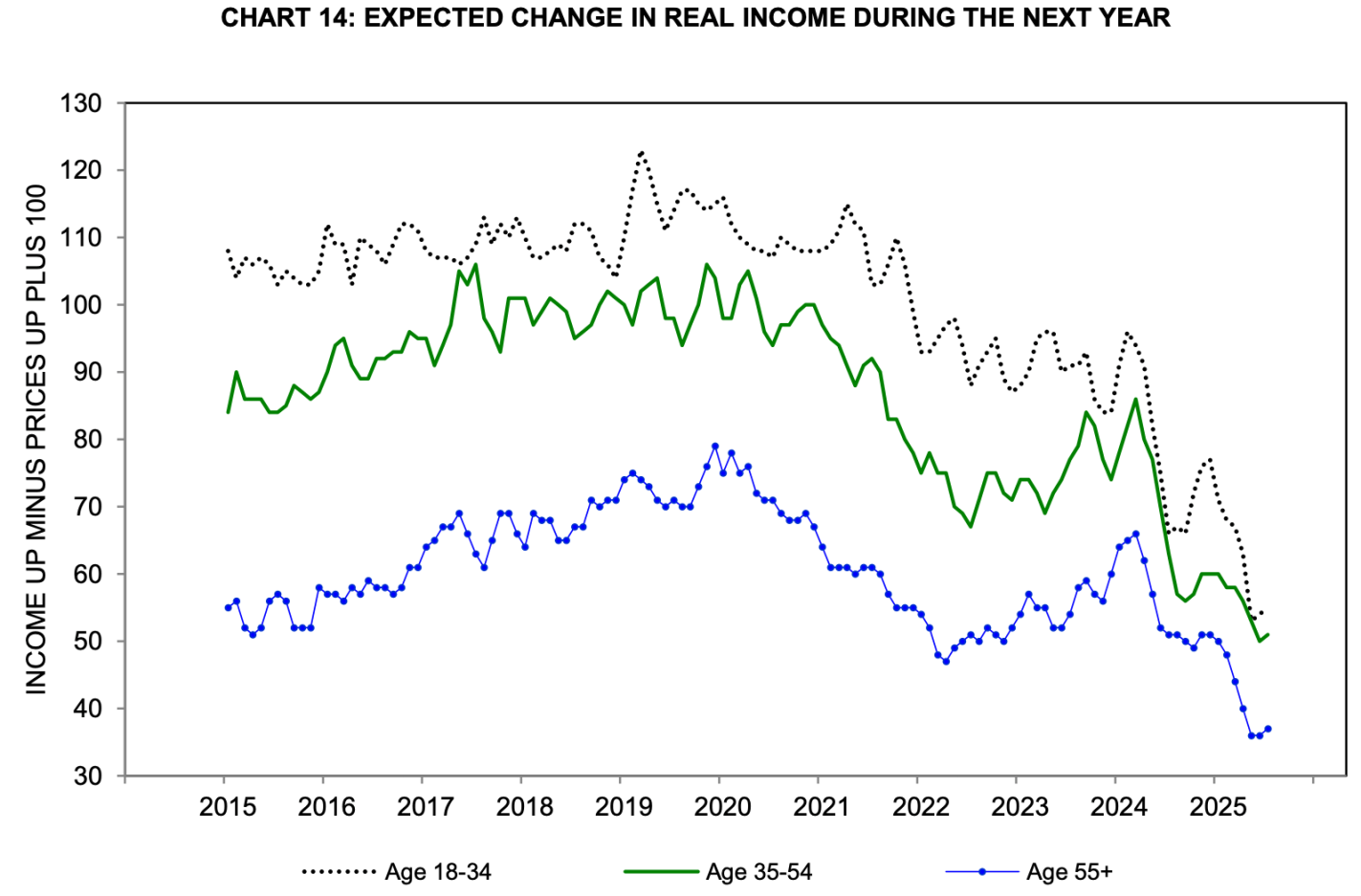

It’s About The Future: Sure things have been fine, but that is about to change. The more farsighted youth know they will be the ones expected to pay back the big deficits the Federal government is running. They have student loans to pay today now that payments have fully resumed. I predicted after the 2022 student loan forgiveness that we would be back to all-time highs in student debt by 2028, but in fact we are there already. The youth unemployment rate is now 10.5%, up from 6.6% in April 2023, and could rise a lot more if AI really starts displacing jobs:

Source: Brynjolfsson, Chandar and Chen 2025.Source: Michigan Consumer Survey

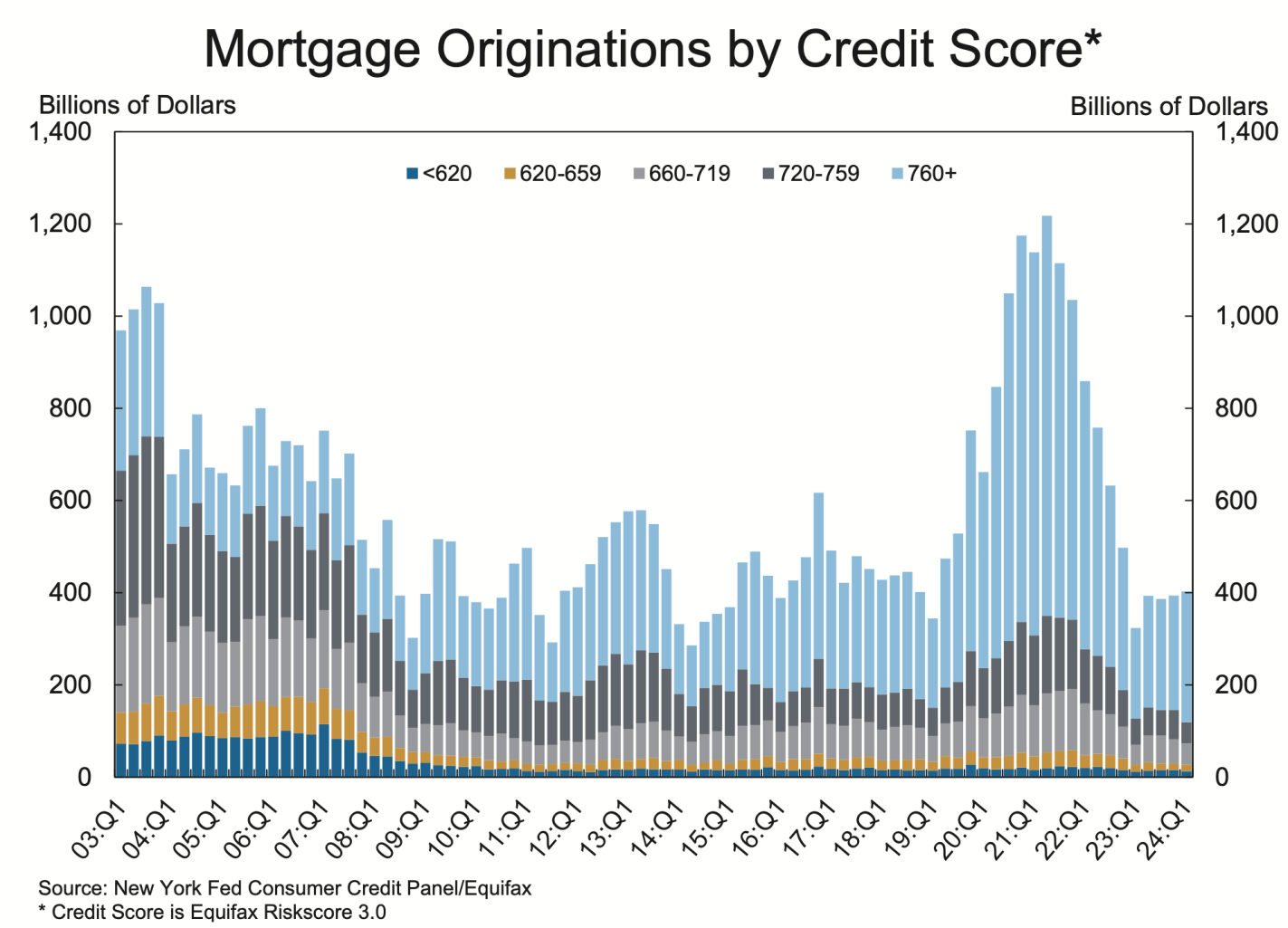

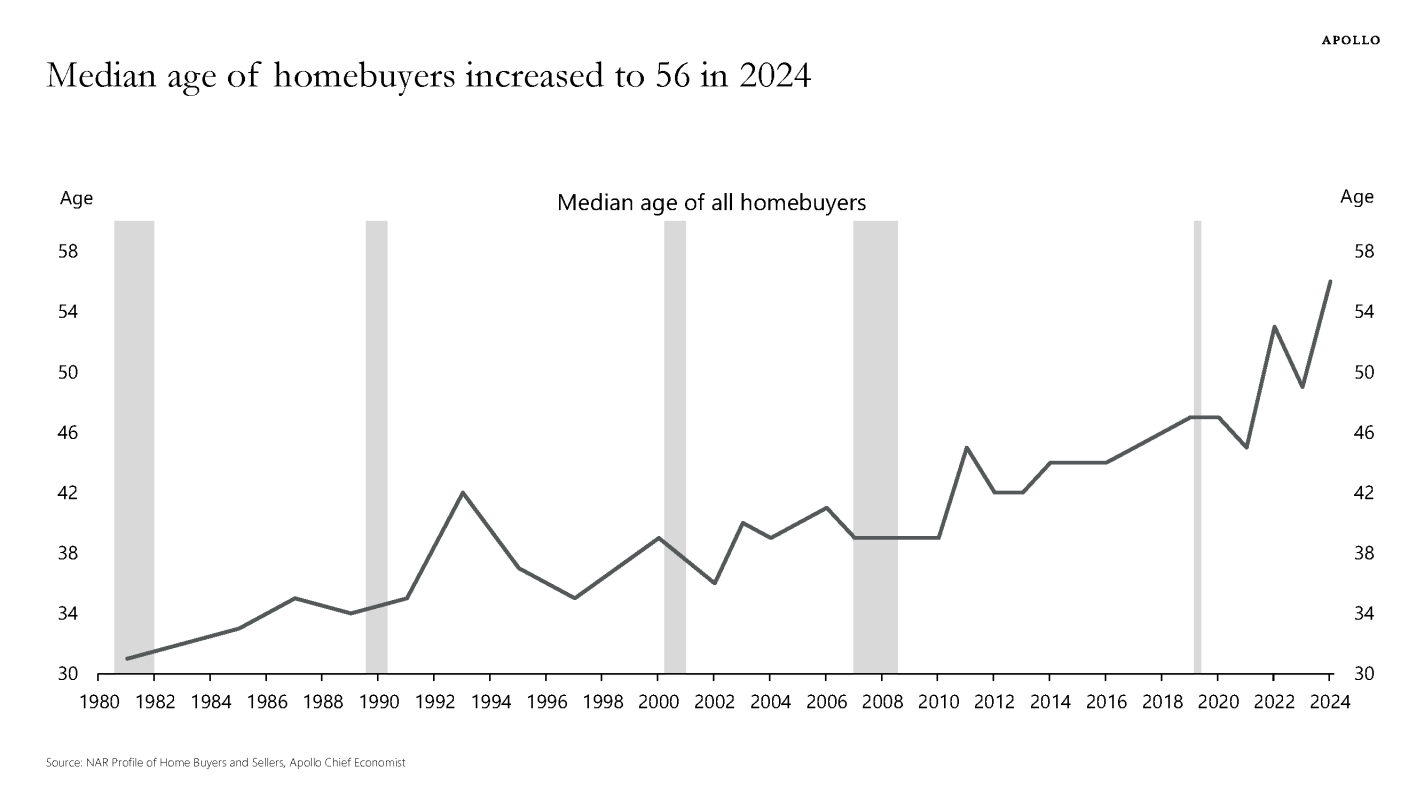

2. It’s About Housing: House prices are at all time highs (far above the prices during the 2000s “bubble”). Mortgage rates remain high, and to the extent that Fed rate cuts push them down, they will likely push prices higher, leaving homes hard to afford. High credit standards post-Dodd-Frank mean younger buyers in particular find it hard to get a mortgage; homeownership rates are falling while the average age of homeowners shoots upward. Most older people already own a house, while most young people want to buy but see that as increasingly out of reach.

Good luck getting a mortgage without super-prime creditEveryone thinks it’s a bad time to buy a house, but this matters most if you’re young and don’t already own oneThe median American is 39 years old but the median homebuyer is 56

This is post coauthored with Jack Cavanaugh, Ave Maria University Graduate of 2025.

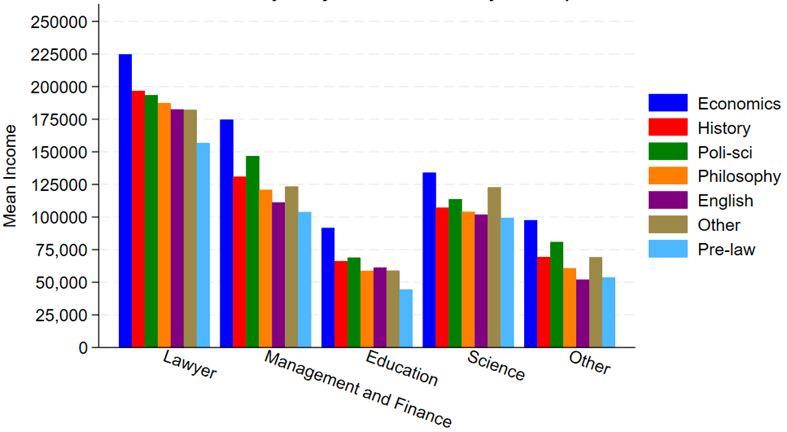

Say that you want to become a successful lawyer. What does that mean? One possible meaning is that you are well-compensated. Money is not everything, but it does give people more options for how to spend their time and resources. Law degrees are a type of graduate degree. So, what bachelor’s degree major should one choose in preparation for law school? We lack rich administrative data on college majors and LSAT scores.

Luckily, the 2023 American Community Survey (ACS) comes to the rescue. It has all of the typical demographic covariates, income, occupation, and college major. So, if we make the small leap that well-prepared law school students become high-performing lawyers who are ultimately paid more, then what college major puts you on the right path? What should your major be?

We don’t look at an exhaustive list. We place several occupations into bins and examine only a few alternative majors. Any unlisted major falls under ‘other’. Below are the raw average incomes by occupational category and college major. Note two majors in particular. First, Pre-law literally has the word ‘law’ in the name and is marketed as preparation for law school. However, it is the undergraduate major associated with the lowest paid lawyers. For that matter, Pre-law majors have the lowest pay no matter what their occupation is. Second, Economics majors are the most highly paid in all of the occupations.

This is from the latest Census release of CPS ASEC data, updated through 2024 (see Table F-23 at this link). In 1967, only 5 percent of US families earned over $150,000 (inflation adjusted).

Addendum: Several comments have asked how much of these trends can be explained by the rise of dual-income households. The answer is some, but not all of it, which I have written about before. Dual-income households were already the most common family structure by the 1980s. There hasn’t been an increase in total hours worked by married households since Boomers were in their 30s. You can explain some of the increase up until the Boomers by rising dual-income households, but this doesn’t explain the continued progress since the 1980s. And as Scott Winship and I have documented, even if you look just at male earnings, there has been progress since the 1980s.

The Federal Reserve will probably cut rates next week:

I can’t advise them on the complexpolitics of this, but based on the economics I think cutting would be a mistake. I see one good reason they want to cut: hiring is slow and apparently has been for a year. But that could be driven by falling labor supply rather than falling demand, and most other indicators suggest holding rates steady or even raising them.

Most importantly, inflation is currently well above their 2% target, 2.9% over the past year and a higher pace than that in August. Inflation expectations remain somewhat elevated. Real GDP growth was strong in Q2 and looks set to be strong in Q3 too, and NGDP growth is still well above trend.. The Conference Board’s measure of consumer confidence looks bad, but Michigan’s looks fine.

Financial conditions are loose, with stocks at all time highs and credit spreads low. Its only September and we’ve already seen more Initial Public Offerings than in any year since 2021 (when the last big bout of inflation kicked off):

Crypto prices are back near all time highs and crypto is becoming more integrated into public stocks through bitcoin treasury companies and IPOs from Gemini and Figure.

The Taylor Rule provides a way of putting all this together into a concrete suggestion for interest rates. Some versions of the rule say rates are about on target, while others including my preferred Bernanke versionsuggest they should be closer to 6%. To me this is what the debate should be- do we keep rates steady or raise them? I see good arguments each way, but the case for a cut seems very weak.

I look forward to finding out in a year or two whether I or the FOMC is the crazy one here.

* The Usual Disclaimer, hopefully extra obvious in this case: These views are mine and I’m not speaking for any part of the Federal Reserve System.

Are you tired of hearing about revisions to jobs data? Well, there was another hot one released by BLS yesterday. Known as the “preliminary estimate of the Current Employment Statistics (CES) national benchmark revision to total nonfarm employment,” this change isn’t yet incorporated into the official jobs data. But it will, possibly slightly modified, be included with the January 2026 jobs release, altering jobs data back to April 2024. It is part of the normal annual process of reconciling the monthly, survey-based jobs data with the near-universe data from unemployment insurance records. Normally, this is a quiet affair, especially the preliminary estimate which is just giving a heads up to researchers about what will be coming in a few months.

I wrote about these preliminary figures last year, when the initial estimate was a negative revision 818,000 jobs. When revised and actually incorporated into the data, it was a somewhat smaller 598,000 jobs, which I then used in a post just last month to show that BLS hasn’t been getting worse at estimating jobs. If anything, they have been getting better. Yesterday’s report showed that the revision could be negative again, this time 911,000 jobs. That’s a little bigger than last year, but maybe it will end up being smaller in the final number. So, no big deal again?

Maybe not. The 911,000 jobs revision would actually be much larger than last year’s revisions because it’s coming on top of a slower growing labor force already. The initial report for March 2024 showed 2.9 million jobs added in the past year, so the 818,000 revision was a much smaller share than this most recent data, since the March 2025 initial report showed just 1.9 million jobs added in the prior year. And the March 2025 jobs numbers have already been revised down by over 100,000 jobs since the initial report, meaning that potentially half or more of the initially reported job gains would be lost due to the revision, as opposed to about 20 percent last year.

Is losing half of the job gains large? Yes. In fact, almost unprecedented:

(note: I am trying out a new chart template. Let me know what you think!)

Bar codes have been common in retail stores since the 1970s. These give a one-dimensional read of digital data. The hardware and software to decode a bar code are relatively simple.

The QR code encodes information in a two-dimensional matrix. The QR code, short for quick-response code, was invented in 1994 by Masahiro Hara of the Japanese company Denso Wave for labelling automobile parts. It can pack far more information in the same real estate than a bar code, but it requires sophisticated image processing to decode it. Fortunately, the chip power for image processing has kept up, so smart phones can decode even intricate QR codes, provided the image is clear enough.

Like most QR codes, it has three distinctive square patterns on three corners, and a smaller one set in from the fourth corner, that give information to the image processing software on image orientation and sizing.

As time goes on, more versions of QR codes are defined, with ever finer patterns that convey more information. For instance, here is a medium-resolution QR Code (version 3), and a very high resolution QR code (Version 40):

My phone could not decode the Version 40 above; the limit may be how much detail the camera could capture.

QR codes use the Reed–Solomon error correction methodology to correct for some errors in image capture or physical damage to the QR code. For instance, this QR code with the torn-off corner still decodes properly as the URL for Wikipedia (whole image shown above):

Getting down a little deeper in the weeds, this image shows, for Version 3 (29×29) QR code, which pixels are devoted to orientation/alignment (reddish, pinkish), which define the format (blueish), and which encode the actual content (black and white):

Uses Of QR Codes

A common use of QR codes is to convey a web link (URL), so pointing your phone at the QR code is the equivalent of clicking on a link in an email. Here is an AI summary of uses:

They are used to access websites and digital content, such as restaurant menus, product information, and course details, enabling a contactless experience that reduces the need for printed materials. Smartphones can scan QR codes to connect to Wi-Fi networks by automatically entering the network name (SSID), password, and encryption type, simplifying the process for users. They facilitate digital payments by allowing users to send or receive money through payment apps by scanning a code, eliminating the need for physical cash or cards. QR codes are also used to share contact information, such as vCards, and to initiate calls, send text messages, or compose emails by pre-filling the recipient and message content. For app downloads, QR codes can directly link to the Apple App Store or Google Play, streamlining the installation process. In social media and networking, they allow users to quickly follow profiles on platforms like LinkedIn, Instagram, or Snapchat by scanning a code. They are also used for account authentication, such as logging into services like WhatsApp, Telegram, or WeChat on desktop by scanning a code with a mobile app. Additionally, QR codes are employed in marketing, event ticketing, and even on gravestones to provide digital access to obituaries or personal stories. Their versatility extends to sharing files like PDFs, enabling users to download documents by scanning a code. Overall, QR codes act as a bridge between the physical and digital worlds, enhancing efficiency and interactivity across numerous daily activities.

Note that your final statement in this world might be a QR code on your gravestone.

Security with QR Codes

On an iPhone, if “Scan QR Codes” (or something similar) has been enabled, pointing the phone at a QR code in Camera mode will display the first few characters of the URL or whatever, which gives you the opportunity to click on it right then. If you want to be a bit more cautious, you can take a photo, and then open Photos to look at the image of QR code. If you then press on the photo of the QR code, up will come a box with the entire character string encoded by the QR code. You can then decide if clicking on something ending in .ru is what you really want to do.

Accessing a rogue website can obviously hurt you. And even if you aren’t dinged by that kind of browser exploit, the reader’s permissions on your phone may allow use of your camera, read/write contact data, GPS location, read browser history, and even global system changes. The bad guys never sleep. Who would have thought that a QR code on a parking meter posing as a quick payment option could empty your bank account? Our ancestors needed to stay alert to physical dangers, for us it is now virtual threats.

ACKNOWLEDGEMENT: The bulk of the content, and all the images, in this blog post were drawn from the excellent Wikipedia article “QR code”.

Many people take a basic statistics course in college. Those course usually include an overview of standard graphs and best practices for visualizing data.

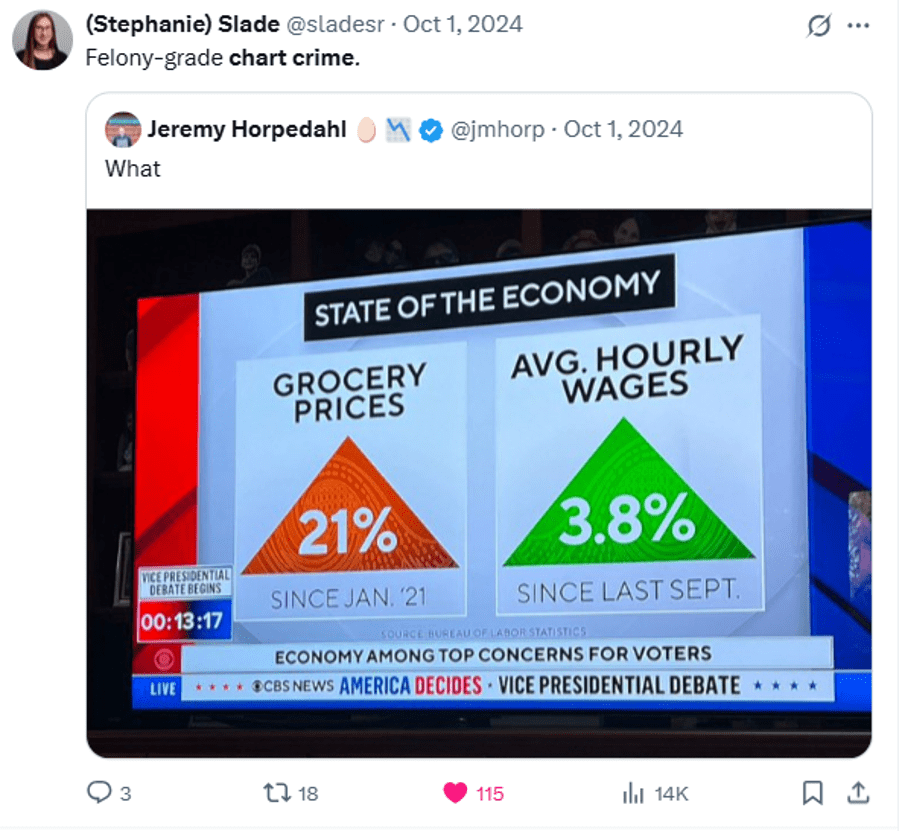

To keep that section from getting boring (“here’s a line graph… here’s a bar chart…”) you can borrow my slides on #chartcrimes Teaching people best practices is more engaging when you can show real examples of charts gone wrong.

These are pictures I dropped directly into slides and talked through:

P.S. Joke I made about this section of my textbook:

My textbook includes a slide specifically telling people not to use techniques thought to be cutting edge in 1998. "Perplexing depth" and "distracting art" 💀 pic.twitter.com/Pk5baBZvK1

I’m piggy-backing off of the FRED blog and off of Jeremy’s post with yet more data. Let’s set the stage.

FRED blog, using BLS data from the Current Population Survey (CPS), shows that the labor force participation rate (LFPR) fell by about 1.4pp for people 55 years and older between 2017 & 2023. CPS data is released quickly, but the sample sizes are not massive. There are 3.4 million people in the 7 years of monthly data (so, a little over 40k people age 55+ per monthly observation).

Also using CPS data, Jeremy shows that FRED commits the fallacy of composition because there are very different people who are 55 and older. Specifically, he illustrates that the LFPR for people ages 55-64 have experienced about a 1.3pp *higher* LFPR in 2023 vs 2017. The implication is that something is happening to the people older than 64.

I use annual CPS instead. Why? Because it can be corroborated with the annual American Community Survey (ACS) data for 2017-2023.

“Both younger and older workers withdrew from the labor force in large numbers during the pandemic: In fact, their participation rates plummeted. Yet, within two years, the younger workers had bounced back to their pre-pandemic participation rates. But the older workers have not.”

They include a chart which seems to back up that assertion:

However, if you look closely, you will see that the older workers’ age group is open-ended. It includes 55-year-olds, as well as 95-year-olds. Given that the US population is aging, this seems like a poor choice.

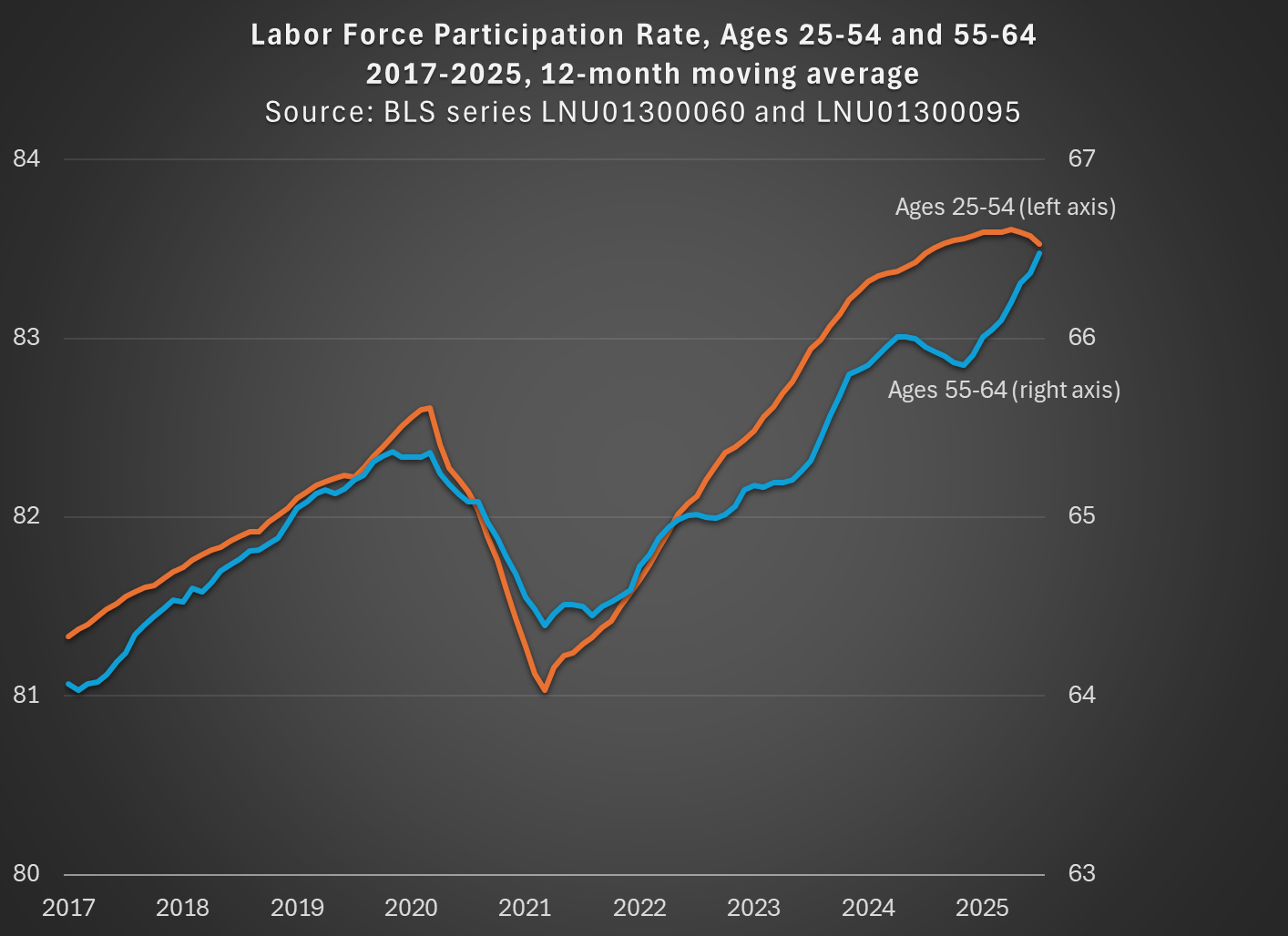

While not available currently in the FRED database, there is data from BLS available for older workers that is not open-ended. For example, we can look at workers ages 55-64, who are older but still young enough that they are mostly below traditional retirement age. I use that data and compare with the 25-54 age group (note: because the 55-64 data isn’t available seasonally adjusted, I use the non-adjusted data for both age groups, then use a 12-month average, so my chart doesn’t exactly replicate the chart above):

By using a closed-end age group for older workers, we see that labor force participation has not only recovered from the pandemic, but it exceeds the pre-pandemic peak for both prime-age and older workers, and had done so by the Spring of 2023. In fact, both are now about 1 percentage point above February 2020. If we want to go to the first decimal place, older workers have actually increased their labor force participation slightly more: 1.1 vs 0.9 percentage points. But these are close enough, given that this is survey data, to say the recovery has been roughly equal.

The St. Louis Fed blog concludes by saying that early workforce retirements “will continue to depress the labor force participation rate of workers aged 55 and older for the foreseeable future.” But it’s not true that the LFPR of older workers is depressed! Provided that we exclude those 65 and older.