US GDP fell for the second straight quarter according to statistics released this week by the Bureau of Economic Analysis. This means that by one common definition we’re now in a recession, which has ignited a debate about whether “two consecutive quarters of negative GDP growth” is the best definition (as opposed to ‘when the NBER says there’s one’, like I generally teach and Jeremy argued for here, or something else).

Naturally this debate has political overtones, since the party in power would be blamed for a recession, so we’ve seen the White House CEA argue that we’re not in a recession, many on the other side argue that we are, and plentiful hypocrisy from people who should know better.

But in political terms, the fight over the binary “are we in a recession” call won’t be the big economic factor in November’s elections- that will be inflation and GDP, especially 3rd quarter GDP. One of the oldest and best predictors of US elections is the Fair Model, which uses inflation and the number of recent “strong growth quarters”. Fair’s update following the recent Q2 GDP announcement states:

the predicted vote share for the Democrats is 46.70, which compares to 48.99 in October. The smaller predicted vote share for the Democrats is due to two fewer strong growth quarters and slightly higher inflation

By Election Day we’ll have 3 more months of economic data making it clear whether inflation is getting under control and whether economic activity is picking back up or continuing to decline. Monthly data releases on inflation and unemployment will be closely watched, but the most discussed release will likely be third quarter GDP. It will summarize 3 months instead of just one, it will be of huge relevance to the debate over how severe the recession is or whether we’re even in one, and it will likely be released less than two weeks before election day. The NBER almost certainly won’t weigh in by then; they tend to take over a year to date recessions, not adjudicate debates in real time.

So when BEA does release their Q3 GDP estimate in late October, what will it say? Markets currently estimate at least a 75% chance it will be positive (they had estimated a 36% chance of positive Q2 GDP just before the latest announcement). That sounds high to me, the yield curve is still inverted and I bet investment will continue to drag, but forecasting exact GDP numbers is hard. Its a much easier bet that whatever the number turns out to be will loom large in political debates just before the elections. Perhaps we’ll get the Q3 GDP growth number that would make for the most chaotic debate: 0.0%.

I heard on a radio interview that spending by the bottom quartile is way down in 2022, while it is holding up merrily for the upper two quartiles. My mind jumped to the thesis:

“Hmm, the bottom quartile probably (proportionately) felt the benefit of the three COVID stimulus packages more, plus they would have benefited more, proportionately, from the enhanced 2020-2021 unemployment benefits, which (I gathered from anecdotal observations) often paid them more for staying home than they used to receive for working. But…by 2022, all that extra money may be running out.”

I spent some time poking around the internet, trying to find some pre-made figures or tables to support or disprove this thesis. What I found tended to support it, but this is not rigorous data-mining. So, for what it is worth, here are some charts.

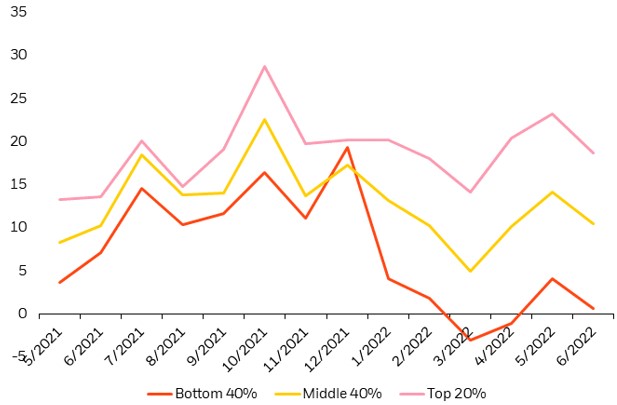

First, about the spending in 2022. This chart indicates that discretionary service spending by the bottom 40% income cohort is indeed down sharply in 2022, and now sits a little lower than a year ago, while the upper 20% cohort is spending actually more than a year ago. Spending by the middle 40% trended up in 2H 2021, then back down in 1H 2022, to end about even over the past 12 months:

Discretionary service consumption by income cohort. (I don’t what the units are for the y-axis, but presumably they show the trends). Source: Earnest Research, as of June 30, 2022, as reproduced by Blackrock.

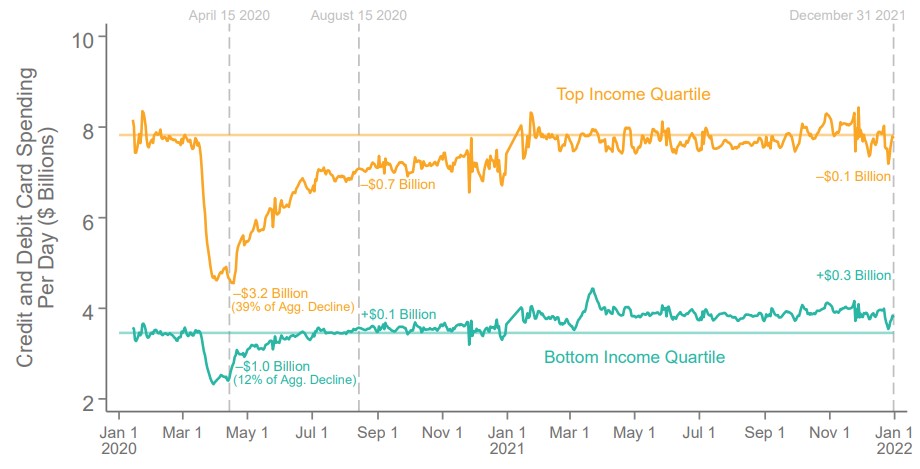

And what about 2020-2021? The next two charts indicate (a) that consumer spending was HIGHER in 2021 that it was pre-COVID for the bottom income quartile, even though (b) their employment in 2021 remained some 20% LOWER than pre-COVID. Looks to me like a lot of spending of stimmie checks was going on in 2021, but (see above) that money has run out in 2022.

Some reader here may have access to a more consistent data set, so I am happy to see this thesis tested further.

The truth is, we don’t know. But let’s be clear: whether we are or not doesn’t depend on the 2nd quarter GDP report. Though two consecutive quarters of declining GDP is often cited as the definition of a recession, it’s not the definition economists use. And with good reason.

Instead, the NBER Business Cycle Dating Committee uses this definition: “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.” And they explain why GDP is not their preferred measure, which includes several reasons but this one seems most germane to our current moment: “[the] definition includes the phrase, ‘a significant decline in economic activity.’ Thus real GDP could decline by relatively small amounts in two consecutive quarters without warranting the determination that a peak had occurred.”

If not GDP, what do they look at? I’ll get into more detail later, but in short, they look at monthly measures of income, consumption, employment, sales, and production (a direct measure of production, which GDP is not — it’s a proxy).

However, the American public seems convinced that we are in a recession. The most recent poll I can find on this is from mid-June, which is useful because (as we’ll see below) we have most of the relevant measures of the economy for June 2022 already. In that poll, 56% of Americans say we are in a recession. And while there is some partisan bent to the responses, even 45% of Democrats seem to think we are in a recession. For those that say we are in a recession, 2/3 cite inflation as the primary indicator that we are in a recession.

Already here we can see the difference between the general public and NBER: the rate of inflation is not one of the measures that NBER considers when defining a recession. So, what are the measures they use?

I have written three blogs on the TV show Severance this summer. My newest post is up at the Online Library of Liberty.

I discuss how job perks are portrayed in the show. The bosses in the show are creepy and we come to find out that they are totally evil. Given the way everything feels in the show, you could come to the conclusion that perks are generally manipulative and false. Someone implied that in an op-ed published by the NYT.

My argument is that free adults can use “perks” to motivate themselves and each other to do the right thing.

We are all just trying to get that dopamine, in the short term. Should people only feel happy when they are doing drugs or playing video games? Should bosses not be allowed to create a fun moment at work?

Trivial gifts and prizes must be cheap, so that their cost does not start to outweigh the benefits of incentivizing things we should be doing anyway. Finding ways to make a responsible life exciting is in fact the key to maintaining our liberty. Most people do not want to be martyrs. They want life to be fun.

The following tweet shows the character Dylan and his performance prize.

— OutofContextSeverance (@SeveranceOutof) June 24, 2022

Behavioral scientists have documented lots of quirks in human behavior. We aren’t solely motivated by our (real wage) salaries to produce effort. The good news is that we are capable of self-reflection. We can make these quirks work for us. Lots of successful people will promise themselves a small reward at the end of the week if they accomplish something hard.

Perks aren’t all bad at work, but, on the other hand, Severance could make you more alert to genuine manipulation that is out there.

Watching Severance prompts good questions. Who are you? (That’s the opening line of the show.) What are you doing with your life? Whose purposes are you serving?

I liked the show because it has great characters, funny moments, and it gets you thinking. If you watch the show, don’t take it too seriously. Ben Stiller is a co-director. The man (the genius) brought us Zoolander (2001).

One give-away that this ain’t the new 1984 is a plot hole concerning how the main character Mark decided to sever himself and join the evil corporation. According to the show, his wife died and he was so sad that he quit his job as a history professor after three weeks of feeling sad. I know a lot of academics. History professors have worked too hard and too long to quit their jobs after three weeks of feeling sad. Take everything with a grain of salt from these writers. Mark’s general lack of executive control is at odds with the backstory that he once obtained a job as a history professor.

Severance is described as science fiction but it clearly takes place in the United States of America. For one thing, a “senator” has a role. For another thing, the work schedule is pretty American. This is a funny video on how Europeans view the American work schedule:

What Finland thinks an American workday looks like

I have no idea how far down the rabbit hole the writers will feel like they have to do in Season 2. Will there be a role for a POTUS?

The second blog was posted to EWED: my thoughts about relating Severance to Artificial Intelligence.

A question this raises is whether we can develop AGI that will be content to never self-actualize.

And, back in May, OLL ran my first blog about Severance and drudgery.

The first line in the show is, “Who are you?” Themes about identity and purpose are explored alongside the thrilling hijinks of the prisoner innies. Outie Mark has nothing except his personal life to think about, which in his case is tragic. Innie Mark has nothing but work. Neither man is happy or complete.

Michael Maynard and I wrote about giving a good gift. A good gift is one in which the giver has an information advantage. Gifting an object or a service can provide a consumption bundle to the recipient that they didn’t know was even possible or that they didn’t know that they would prefer. They would have chosen the items themselves, if only they had known about them. Giving a gift card can be similar if the recipient did not know about the vendor previously. Cash is a good gift when the giver does not have an information advantage over the recipient.

In our previous post, we showed diagrammatically that ‘better off’ was indicated by the higher utility. But this spurs an important question:

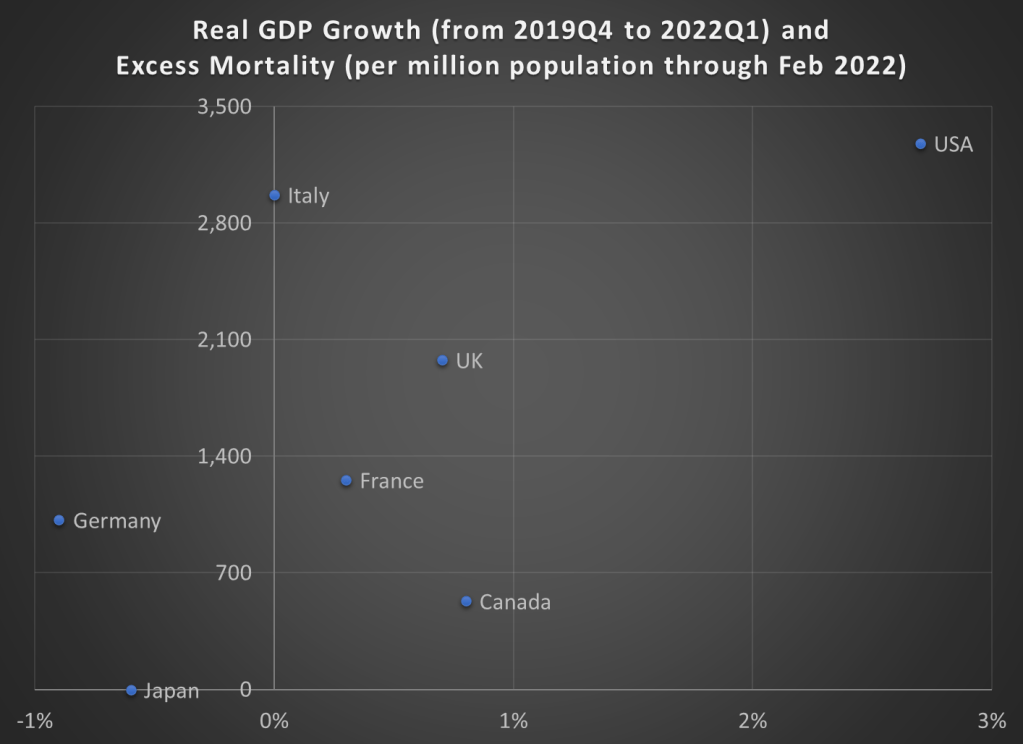

Today, my chart looks at the G7 countries (representing roughly half of global wealth and GDP), showing both their economic performance (as measured by real GDP growth) and health performance (as measured by excess mortality through February 2022).

The US has clearly had the best economic performance. But the US also had the highest level of excess deaths per capita (not all of this is from COVID — US drug overdoses are also way up — but even using official COVID deaths, the US still tops this group).

Japan had the best health performance, in fact amazingly no cumulative excess deaths through February 2022 (this has risen very slightly since then, but I stopped in February so all countries had complete data). However, Japan also had slightly negative economic growth.

Which country ends up looking the best? Canada! Very low levels of excess deaths, and at least some positive economic growth. Not as much growth as the US, but Canada is the second best performer in the G7.

To give some context of just how low the level of deaths have been in Canada, first recognize that the US had 1.1 million excess deaths in the pandemic through February 2022. If instead our excess deaths had been roughly equal to Canada on a per capita basis, we would have only had 180,000 excess deaths in the US, saving over 900,000 lives.

Some of Canada’s COVID policy have been overly restrictive, such as the vaccine mandates that sparked protests in February 2022. But by then, Canada had already largely achieved it’s COVID victory over the US and most other G7 nations. Compare excess mortality in Canada with the US: the only big wave in Canada that came close to the US was the Spring 2020 wave. After that, Canada was always much lower.

Ah, the delicious crypto bubble of 2021. Major cryptocurrencies like Bitcoin and Ethereum more than tripled in value. Every week, some new coin would get minted, letting early adopters 10X their money in a month. Decentralized finance (DeFi) based on blockchain technology was The Next Big Thing. Move over, stodgy old Bank of America.

That was then, this is now. The chart below of Bitcoin price serves as a proxy for the fortunes of the whole sector:

This has the smell of a bubble bursting. First, why did crypto soar in 2021? I think COVID gets some credit for that. Most adults in the developed world sat home for many months in 2020-2021, and in countries like the U.S. were handed thousands of dollars of stimulus money, in addition to giant unemployment checks. Much of that money went to buying “stuff” on Amazon, but much of it went into financial assets like stocks and crypto. Something like half of men in the United States between the ages of 18 and 49 dabbled in crypto. As you saw your friends making money effortlessly, classic tulip bulb FOMO set it.

All bubbles end eventually. Crypto has imploded from a $ 3 trillion market to a $ 1 trillion dollar market in just a few months. That is two trillion (with a “t”) gone. If Bitcoin were the only significant factor in the crypto universe, the latest bust would be a fairly trivial matter. Since Bitcoin goes up and Bitcoin goes down, that is nothing new. But part of the hype of 2021 was all the breathless commentary on how DeFi would sweep the world and Change Everything. No more centralized banking controlled by old men in suits – – power to the people! And in fact, a whole industry of lending and borrowing in the crypto world has sprung up. That is where some more consequential problems have shown up.

Warren Buffet is known for the saying, “When the tide goes out, you find out who is swimming naked.” The rapid fall in crypto valuations has set off a cascade of failures in DeFi. A key event was the implosion of the Luna/Terra (un!)stablecoin, in April-May 2022, which we wrote about here. A more widespread problem has been the unwinding of the crypto lending/borrowing system. Various firms loaned out the coin holdings of their customers to parties that wanted to trade (speculate) with them, and who were willing to pay something like 4-9% interest for get ahold of these coins. The parties doing the lending thought they were keeping themselves safe by requiring excess collateral for these loans.

Oversimplified example: I will lend you $100 (real dollars) if you deposit $140 of Dogecoin with me. If Dogecoin falls in value to close to $100, I would require more collateral from you within say ten days, or else I would sell your Dogecoin into the market and get my $100 back (and you eat the $40 loss). The big problem comes if Dogecoin falls so fast that by the contracted grace period ends, its value is down to $80. Now I as well as you realize losses, and widespread panic ensues. Now, if I have been lending out your Dogecoin to yet more parties who (it turns out) can’t pay me back in full, I am doubly hosed. And now the solid customers start withdrawing their funds/coins from these firms, and we have an old-fashioned bank run. It doesn’t help that Celsius Network froze customers’ accounts last month, so they could not withdraw the coins they had deposited. That sort of thing really gets clients nervous.

And so a number of significant DeFi firms are going bust, and calls get louder for more government regulation, which is largely antithetical to the whole DeFi enterprise. I will paste below a summary of this carnage, and then in the interests of full disclosure, tell how it has affected me personally:

The crypto and the DeFi industry boomed over the past few years but the recent crypto crash has plundered the fortunes of several crypto companies. The following crypto companies have recently encountered financial difficulties:

Vauld

Business Today broke the news on Monday that Vauld, the Singapore-based crypto lending and investment firm operating in India announced that it has halted withdrawals and deposits for its more than 8,00,000 clients. Vauld’s CEO Darshan Bathija said in a blog post that unstable market circumstances had created “financial challenges” for the company. The CEO also announced that investors had withdrawn over $197 million in the past few months.

Terraform Labs

Terraform Labs was the company that had triggered the recent crypto crash. They created the algorithmic stablecoin TerraUSD which de-pegged from the US Dollar and led to the crash of Terra Luna another token of the ecosystem causing massive panic and sell off in the crypto markets.

Terra co-founder Do Kwon announced a “recovery plan” in May that included infusion of additional funding and the rebuilding of TerraUSD so that it is backed by reserves rather than depending on an algorithm to maintain its 1:1 dollar peg.

Voyager Digital

On July 6, the American crypto lender disclosed that it had filed for bankruptcy. In its Chapter 11 bankruptcy petition, Voyager stated that it had over 1,00,000 creditors, assets between $1 billion and $10 billion in value, and liabilities in the same range.

Three Arrows Capital (3AC)

The Singapore-based cryptocurrency hedge firm went bankrupt on June 29, just two days after receiving a notice of default on a crypto loan from lender Voyager Digital for failing to make payments on an approximately $650 million crypto loan. The company filed a petition for protection from its creditors under Chapter 15 of the United States’ bankruptcy code on July 1. This section of the code permits overseas debtors to safeguard their U.S.-based assets.

Celsius Network

Celsius Network also suspended withdrawals and transfers last month due to “extreme” market conditions. They also hired consultants in preparation for a future bankruptcy filing. The American-Israeli business reportedly disclosed on July 4 that a quarter of its workers had been let go.

Babel Finance

The Hong Kong-based cryptocurrency lender stated on June 17 that it had temporarily halted crypto-asset withdrawals as it scrambled to reimburse consumers. According to the company, “Babel Finance is suffering unprecedented liquidity issues due to the current market situation,” emphasising the severe volatility of the market for cryptocurrencies.

CoinFLEX

In a blog post published on Thursday, CoinFLEX’s CEO Mark Lamb announced that the company would temporarily halt withdrawals due to “extreme market conditions” and uncertainty about a certain counterparty. The company is facing serious financial troubles and there seems to be no way out.

My Confessions

Briefly — I bought into Bitcoin and Ethereum in the form of the funds GBTC and ETHE towards the end of 2020. As crypto started to unwind this year, I sold out of ETHE to de-risk, coming out a little ahead there. I decided to hang in with the Bitcoin fund, riding it up, and now down, down, down. I am so far in the red on this one that I am just going to hold it indefinitely, hoping for some recovery someday.

I bought into Voyager (see above, it has recently crashed and burned) and sold half after it doubled, and the rest at about breakeven price, so came out ahead there. Another, similar firm, Galaxy Digital, I bought has also plummeted to near zero. I got out of that, but waited too long and lost about 30% there.

Readers with exquisite memories might recall that I wrote an article some months back here on EWED touting the DeFi model as a great way to earn interest to keep up with inflation: “Earning Steady 9% Interest in My New Crypto Account.” I chose BlockFi rather than Celsius Network to put my funds in for this, since Celsius (an offshore enterprise) seemed a little shady, whereas BlockFi made a point of being audited and compliant with U.S. regulations. Good choice, in light of Celsius’ recent freeze on customer withdrawals.

Now, even solid firms like BlockFi are hurting. Customers spooked by all the other crypto drama are withdrawing assets “just to be on the safe side.” BlockFi is seeking cash infusions from white knight Sam Bankman-Fried to stay afloat. The 30-year old crypto billionaire looks to be able to acquire the firm for pennies on the dollar, wiping out the initial (private) investors in BlockFi. I am one of these BlockFi customers withdrawing funds (half of my deposit there) – – just to be on the safe side.

We are living in volatile times. With covid-19, big federal legislation packages, and the Ruso-Ukrainian conflict disruptions to grain, seed oils, and crude oil, relative prices are reflecting sudden drastic ebbs of supply and demand. I want to make a small but enlightening point that I’ve made in my classes, though I’m not sure that I’ve made it here.

Economists often get a bad rap for being heartless or unempathetic. Sometimes, they are painted as ideologues who just disguise their pre-existing opinions in painfully specific terminology and statistics. Let’s do a litmus test.

Consider two alternative markets. One is a perfect monopoly, the other has perfect competition. All details concerning marginal costs to firms and marginal benefits to consumers are the same. In an erratic world, which market structure will result in greater price volatility for consumers? Try to answer for yourself before you read below. More importantly, what’s your reasoning?

Extreme Market Power

A distinguishing difference between a competitive market and a monopoly concerns prices. While firms maximize profits in both cases, the price that consumers face in a competitive market is equal to the marginal cost that the firms face. There is no profit earned on that last unit produced. In the case of monopoly, the price is above the marginal cost. Profits can be positive or negative, but the consumer will pay a price that is greater than the cost of producing the last unit.

Below are two graphs. Given identical marginal costs of production and benefits that the consumers enjoy, we can see that:

The monopoly price is higher.

The monopoly quantity produced is lower.

But static models only go so far. What about when there is volatility in the world?

Volatile Costs

Oil and gasoline are important inputs for producing many (most?) physical goods. Not only that, they are short-lived, meaning that they disappear once they are used, making them intermediate goods. Therefore, changes in the price of oil constitutes a change in the marginal cost for many firms. If the price of oil rises, or is volatile otherwise, then which type of market will experience greater price and quantity volatility?

Below are two figures that illustrate the same change in the marginal cost. We can see that:

Monopoly price volatility is lower (in absolute terms and percent).

Monopoly quantity produced volatility is lower (in absolute terms, though no different as a percent).

The take-away: While monopoly does constrict supply and elevate prices, Monopoly also reduces price and output volatility when there are changes in the marginal cost.

Volatile Demand

That covers the costs. But what about volatile demand? A large part of the Covid-19 recession was the huge reallocation of demand away from in-person services and to remote services and goods. What is the effect of market power when people suddenly increase or decrease their demand for goods?

Below are two figures that illustrate the same change in demand. We can see that:

Monopoly price volatility is higher (in absolute terms, though no different as a percent).

Monopoly quantity produced volatility is lower (in absolute terms, though no different as a percent).

Monopolies Don’t Cause Inflation

Economists know that inflation can’t very well be blamed on greed (does less greed beget deflation?). Another problematic story is that market concentration contributes to inflation. But the above illustrations demonstrate that this narrative is also a bit silly. Monopolistic markets cause the price level to be higher, it’s true. But inflation is the change in prices. Changing market concentration might be a long term phenomenon, but can’t explain acute price growth. If demand suddenly rises, monopolies result in no more price growth than perfectly competitive markets. If the marginal cost of production suddenly rises, monopolies result in less price growth.

All of this analysis entirely ignores welfare. Also, no market is perfectly competitive or perfectly monopolistic. They are the extreme cases and particular markets lie somewhere in between.

Did you guess or reason correctly? Many econ students have a bias that monopolies are bad. So, in any side-by-side comparison, students think that “monopolies-bad, competition-good” is a safe mantra. But the above illustrations (which can be demonstrated mathematically) reveal that economic reasoning helps to reveal truths about the world. Economists are not simply a hearty band of kool-aid drinking academics.

Most Americans are covered by employer-sponsored health insurance, either through their own job or a family member’s. This can make it difficult to switch jobs- the new job might not offer insurance, or might have a worse insurance plan or network- locking people into their current job.

Economists have documented since at least the 1980’s how our insurance system seems to reduce job mobility. Several reforms have tried to improve the situation- COBRA, HIPAA, and most recently the Affordable Care Act.

In a paper published this week, Gregory Colman, Dhaval Dave and I evaluate how the extent of “job lock” has changed over time. In short, we find that job lock remains substantial and the Affordable Care Act doesn’t appear to have done anything to improve the situation. The paper has many tables of regression results, but the pictures tell the basic story:

Trends in job mobility for those with and without employer-sponsored insurance (ESI) using Current Population Survey data

The details differ a bit depending on which dataset and identification strategy we use, but a few things are clear:

Macroeconomic factors are dominant in the short run; mobility falls during recessions like 2001 and 2007, then recovers.

The long run trend has been toward lower job mobility for those with AND without employer-based insurance

Those without employer-based insurance are still much more likely to switch jobs (we find 25-45% more likely)

To the extent that this gap has closed since the year 2000, it has come through falling job mobility for those without employer-based insurance more than rising job mobility for those with employer-based insurance

Why does the Affordable Care Act appear not to have improved things? This remains unanswered, but we conclude the paper with some hypotheses:

In fact, our point estimates suggest that job lock actually got stronger following the ACA. One possible explanation for our finding is that the ACA’s individual mandate made insurance even more desirable by fining the uninsured. Another possibility is that workers continue to value employer-provided health insurance more over time as premiums continue to rise

I’m on vacation this week. But no, I’m not just saying this to get out of posting this week, or to brag. Americans really have started going back to the normal routine of vacations after a long break during the pandemic.

You might think that the high price of gasoline will slow down summer travel. Not so, according to estimates from AAA. While the total number of estimated travelers for Independence Day weekend is still slightly below Summer 2019 (by about 1 million travelers), travel by car is predicted to be just above 2019 levels (by about 0.5 million travelers), with 42 million Americans traveling by car. Air travel has been a mess lately and quite expensive (even compared to pre-pandemic levels), and is predicated to be about 0.5 million below 2019. Bus/train/cruise travel is still the big loser, well above the past two summers, but still 1 million travelers below 2019. (These are all estimates, of course, but AAA is in the business of knowing this data well.)

What gives? Basic economic theory would tell us that if the price of something increases, people should buy less of it. And traveling by car is much more expensive than in Summer 2019. We should also think about substitutes, and airline travel is certainly a substitute for car travel. But if we look at what has happened to both airfares and gasoline prices since July 2019, we can see that gasoline prices have increased much more (about 60% vs. 25% for airfares).

So, do we just throw up our hands and say: “it’s just too complicated, lots of factors at play”?