Released this April, but I just heard about it today. Researchers did the painstaking work of going through all 50 states to determine which steps must be taken in each state before new regulations can take effect. For instance, it turns out half of states require economic analysis for new regulations, and half don’t. The paper is here: https://www.mercatus.org/publications/regulation/50-state-review-regulatory-procedures

8 Billion

That’s it. That’s the post. Read more.

My BlockFi Crypto Account Is Frozen Due to Monster FTX Exchange Blowup

About a year ago, I posted some articles touting the use of BlockFi as an alternative checking account. It paid around 9% interest (this was back when interest rates were essentially zero on regular savings accounts), and allowed withdrawal or deposit of funds at any time. Nice. BlockFi is associated with respected firm Gemini, and (unlike many crypto operations) is U.S. based, with consistent formal auditing. They earned interest on my crypto by lending it out to “trusted counter-parties”, always backed by extra collateral. What could possibly go wrong?

In July I wrote about a big cryptocurrency meltdown, in which a number of medium-sized players went bust. At that time, BlockFi assured its customers that its sound business practices put it above the fray, no problemo. They did make it through that juncture OK. But I withdrew a third of my funds, just to be on the safe side.

The huge news in crypto this past week has been the sudden, total implosion of major exchange FTX (more on that below). FTX is a major business partner with BlockFi. No worries, though, as of Tuesday of last week, BlockFi COO Flori Marquez tweeted that “All BlockFi products are fully operational”. Then the hammer dropped: On Thursday (11/10), BlockFi froze withdrawals, due to complications with FTX. My remaining crypto is stranded, most likely for years of legal proceedings, and I may never get it all back. I’m not going to starve, but the amount is enough to hurt.

In this case, I don’t really blame BlockFi – by all accounts, they have been trying to run an honest, responsible business. Before last week, nobody had much reason to think that FTX was totally rotten. My bad for not connecting the FTX-BlockFi dots earlier, and pulling out more funds when I had the chance.

The Great FTX Debacle

The star of this show is Sam Bankman-Fried, the (former) head of FTX:

James Bailey posted here on EWED on the FTX crash last week. CoinDesk author David Morris summarized the downfall of Bankman-Fried’s crypto empire:

FTX and Bankman-Fried are unique in the stature they achieved before self-immolating. Over the past three years, FTX has come to be widely regarded as a reputable exchange, despite not submitting to U.S. regulation. Bankman-Fried has himself become globally influential, thanks to his thoughts on cryptocurrency regulation and his financial support for U.S. electoral candidates – not necessarily in that order.

… Facts first uncovered by CoinDesk played a major role in the events of the past week. On Nov. 2, reporter Ian Allison published findings that roughly $5.8 billion out of $14.6 billion of assets on the balance sheet at Alameda Research, based on then-current valuations, were linked to FTX’s exchange token, FTT.

This finding, based on leaked internal documents, was explosive because of the very close relationship between Alameda and FTX. Both were founded by Bankman-Fried, and there has been significant anxiety about the extent and nature of their fraternal dealings. The FTT token was essentially created from thin air by FTX, inviting questions about the real-world, open-market value of FTT tokens held in reserve by affiliated entities.

Negative speculation about a financial institution can be a self-fulfilling prophecy, triggering withdrawals out of a sense of uncertainty and leading to the very liquidity problems that were feared.

Customers started a “run on the bank”, withdrawing billions of dollars of assets, leading to total insolvency of FTX:

The Financial Times reported that FTX held approximately $900 million in liquid crypto and $5.4 in illiquid venture capital investments against $9 billion in liabilities the day before it filed for bankruptcy.

If FTX had been run as an honest exchange, this withdrawal should not have been too much of a problem – – just give customers back the coins they had deposited with FTX. Apparently, though, FTX had taken customer assets and transferred them over to a sister company, Alameda, to trade with. The valuable customer crypto assets left the FTX balance sheet, and were largely replaced by the self-generated (and now nearly worthless) FTT token:

It remains worryingly unclear, though, exactly why even such a dramatic rush for the exits would have led FTX to seek its own bailout. The exchange promised users that it would not speculate with cryptocurrencies held in their accounts. But if that policy was followed, there should have been no pause to withdrawals, nor any balance sheet gap to fill. One possible explanation comes from Coinmetrics analyst Lucas Nuzzi, who has presented what he says is evidence that FTX transferred funds to Alameda in September, perhaps as a loan to backstop Alameda’s losses.

It doesn’t help that on Friday (11/11) some $477 million was outright stolen from FTX wallets. (The Kraken exchange said it has identified the thief and are working with law enforcement).

Where does the FTX saga go from here? There seems little in the way of assets left for the bankruptcy judge to distribute to former customers and creditors. In the case of BlockFi, they are dependent on a $400 million line of credit extended to them by FTX back in June, to keep operating. And who knows how much of BlockFi assets were stored with FTX – – since FTX was to be their white knight, BlockFi would not be in a position to withdraw deposits from FTX like other customers did.

I predict that nothing really bad will happen to Bankman-Fried and his buddies who ran this thing. Although its operation was apparently dishonest, it is not clear how much is subject to U.S. federal or state legal jurisdiction. Bankman-Fried and friends ran their empire from a big apartment suite in the Bahamas. Plus, he is pretty well-connected. Beside his massive campaign contributions, his business and sometimes romantic partner Caroline Ellison (she is CEO of Alameda) is the daughter of MIT professor Glenn Ellison, the former boss (as colleagues at MIT) of the U.S. Securities and Exchange Commission chair Gary Gensler. These relations were captured in an impish tweet by Elon Musk:

The long tail of American politics

The Democratic party won more elections than was broadly anticipated last week, though results fell roughly within a standard deviation of the highest regarded forecasts. There were, however, some patterns worth noting. Election deniers seemed to have systematically underperformed expections. Conservative democrats seem to have overperformed expectations, sometimes radically so.

Putting aside forecasts based on polls, make no mistake: the Democrats should have been slaughtered in these elections. High inflation, high gas prices, a frozen housing market, a declining stock market? I’m not Ray Fair, but his inflation+income+incumbency model has been accurately forecasting elections for 50 years for a reason. If Democrats overperformed as massively as it appears they have, then the most likely explanation is that Republicans did something wrong.

First, as is tradition, let us render tribute unto the median voter theorem by whispering Anthony Downs name before taking a sip of coffee. Now, again as is tradition, let us cast mild aspersions upon those who declared the theory obsolete at best, comically reductive and coarse at worst, a relic of a less sophisticated era of social science. Yes, politics exists in more than just the single liberal-conservative dimension and we are all characterized by multi-dimensional preferences. But the liberal-conservative spectrum is the dominant political shorthand for a reason. If politics really were a played out on a single dimension with single-peaked preferences, then the candidate closest to the preferences of the median voter would always win. That has to count for something.

But that’s all just (mildly silly) social scientific gloating. What might we have learned, if anything, from the last two elections? What I think I’ve learned is that the elections– not the discourse, elections, are moving to the center relative to six years ago, and the forces behind it are the same ones that gave us Amazon and the golden age of television. The fixed costs of serving the long tail of consumer demands.

Quick refresher. Amazon succeeded as a retailer not by selling you the 90% of things that everyone else buys, but by offering the 10% of things that you want that relatively few other people want. Once you enter into the long tail of consumption, its extremely difficult for a brick-and-mortar to offer everyone what they want because the opportunity cost of stocking and shelving are to high relative to the small number they will sell. Similarly, in the age of 5 channels, the opportunity cost of niche entertainment is too high. You can’t make Mad Men for 2 million people when you have the potential to air a show that is close enough to the median viewer to grab the attention of 40 million. When the marginal cost of a product listing approaches zero, though, when a 500 channels cut audiences into thousands of slices, however, the math changes. Now the opportunity lies not in serving the lowest common denominator, but giving each person exactly what they want. That’s easier said than done, of course, just ask current Netflix shareholders.

And this appears to be exactly that is happening in the political discourse. The conversation around politics is becoming more niche and, yes, in many cases more extreme. Yes, we are increasingly living in echo chambers served by content producers more than happy to produce bespoke information bundles that will confirm your pre-existing beliefs at the highest possible pitch and volume. But elections are not the discourse. Elections are still played out in a one person, one vote construct and politics is still reducible to a single coarse dimension. Politicians have incentive to incite the id of voters, especially their base, to rile them up to turn out in greater numbers, but that is not without cost. Aligning yourself with your party’s id distances you from the true median voter, who through the forces pushing and pulling political brands will always find herself wary of the most extreme elements of clubs she isn’t particularly interested in joining.

Parties continue to exist and thrive for the same reason that Amazon does. Super-niche product sellers and echo chambers can thrive independently, but when the moment of aggregation arrives, scale matters. Where decision-making bottle necks, either with a credit card or a ballot box, there’s an enormous advantage to having a brand that lowers information costs and mitigates risk. Amazon wins because it’s boring. Amazon mitigates the risk of buying from a million niche producers, some of whom you might only buy from once in your life, but at the end of the day you know everything is almost definitely going to show up. Democrats won more last week than they should have because they’re boring. Voters knew the candidates, some of whom they may never vote for again, would show up to govern and maintain longstanding institutions. The Republican party, in their independent efforts to serve specific niches within their coaltition, let their collective brand deteriorate and, in doing so, failed to mitigate the risk facing the median voter.

Republican’s got caught up serving the discourse, fractured across a thousand channels, but elections aren’t carried out on a thousand channels. There’s still just one ballot box in every election. The median voter theoreom may be based on an unchanging analog model, but so is our democracy.

New Double Auction Paper

This weekend I am at the Economic Science Association meeting.

Most of the economists in this group use experiments as part of their empirical research. In this post I will highlight some recently published work that is in the tradition of Vernon Smith, who influenced all of us so much.

Martinelli, C., Wang, J. & Zheng, W. Competition with indivisibilities and few traders. Experimental Economics (2022). https://doi.org/10.1007/s10683-022-09772-9

Abstract: We study minimal conditions for competitive behavior with few agents. We adapt a price-quantity strategic market game to the indivisible commodity environment commonly used in double auction experiments, and show that all Nash equilibrium outcomes with active trading are competitive if and only if there are at least two buyers and two sellers willing to trade at every competitive price. Unlike previous formulations, this condition can be verified directly by checking the set of competitive equilibria. In laboratory experiments, the condition we provide turns out to be enough to induce competitive results, and the Nash equilibrium appears to be a good approximation for market outcomes. Subjects, although possessing limited information, are able to act as if complete information were available in the market.

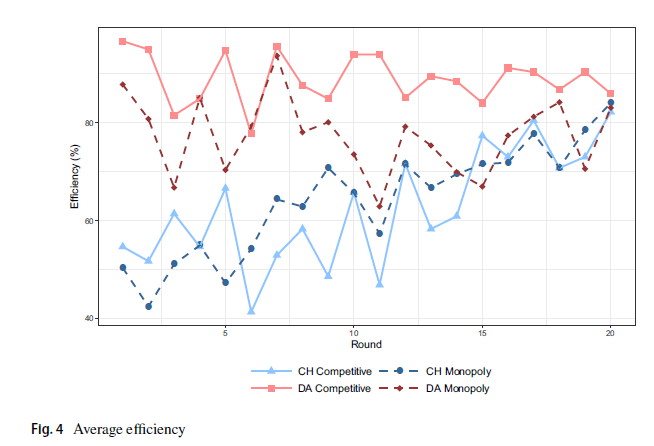

This small excerpt from their results shows a market converging toward equilibrium over time, under different treatment conditions. With some opportunities for practice and feedback, agents create surplus value by trading.

Figure 4 plots the average efficiency in each round in the four treatments. Efficiency is defined as the percentage of the maximum social surplus realized. … learning takes longer under the clearing house institution; hence, average efficiency under the clearing house institution presents a stronger upward trend over time. Under the clearing house institution, the average efficiencies start at levels lower than under the double auction institution, and remain statistically lower in the second half of the experiment. Nevertheless, we can observe from Fig. 4 that the upward trend of the efficiencies in clearing house treatments persist over time, and at the end of the experiment, the efficiency levels from the two institutions are close.

The Price of Food: Farm to the Table

If you’re like me, then you are very fond of food. What determines the price of food? Supply and demand of course!

We can consider food as a commodity because just about anyone can buy and sell it. Almost all foods have partial substitutes. Therefore, the long-run price in the competitive market for food is largely dictated by the marginal cost. Demand has an impact on the price only in the short run.

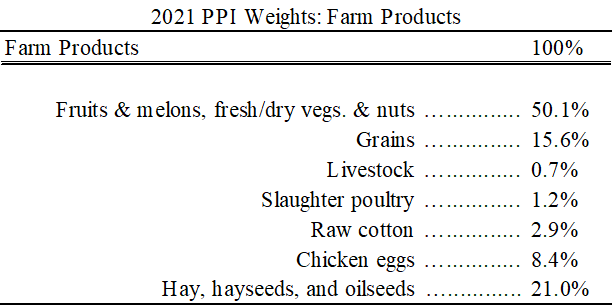

A long-run driver of food prices are the costs that food producers face. The US Bureau of Labor Statistics divides the Producer Price Index into multiple categories that are relevant for a variety of sectors and points within the production process. Below is a table of the most fundamental, relatively unprocessed farm products and their weight among all farm products in December 2021. Cotton is a relatively large component for farm products even though it’s not a food and I include it for completeness. Fruits, veggies, and nuts makeup the overwhelming proportion of the cost of farm products. I was at first surprised that grains composed such a small proportion. But, being dirt cheap, it makes sense.

We all know that inflation has been in the news. It’s been elevated since the second quarter of 2021. Consumer prices tend to lag producer prices. One indicator of where food prices will be in the near future is where the producer prices are now. Below is a graph that displays the above seasonally adjusted farm product prices since the start of 2021*.

Continue readingTwo Types of News: Elections vs Crashes

Some events are like elections: it was obvious that some big political news would break on Election Day, we just had to wait to find out what exactly would happen. Others are like market crashes: you might know in principle they’re a thing that can happen, but you don’t really expect any particular day to be the day one happens, so they seem to come out of the blue. As it turns out, for one of the largest crypto exchanges the day of the crash also happened to be Election Day.

FTX.com is facing a bank run sparked by competitor Binance tanking the price of the token that backed some of their assets. Customers are having issues withdrawing their money, Binance has withdrawn its offer to bail out FTX by taking them over, and bankruptcy seems likely. Supposedly this doesn’t affect Americans using FTX US, but I’d be nervous about any funds I had there, or indeed with funds in any centralized crypto exchange or stablecoin (Tether and even USDC seem to be having issues holding their pegs). All this was especially shocking because many considered FTX founder Sam Bankman-Fried one of the most trustworthy people in the often sketchy world of crypto. He was always meeting with US regulators and lawmakers, and seems not to be motivated by greed; he had already begun to give away his fortune at scale.

After any surprising event like this, some people claim it was actually obvious and they saw it coming (despite usually never having said so beforehand), while others start looking back for warning signs they missed. The most interesting one is something that shocked me when I first heard it March, but I never considered the risk it implied for FTX until the crash:

Going forward, red flags to watch out for seem to be topping a list of youngest billionaires (as Elizabeth Holmes also did) and buying naming rights to a stadium.

In contrast to this crash, the election happened right when we all expected, and at least largely how I expected. Like markets, I underestimated Democrats a bit; polls overall were impressively accurate this year, though they of course missed on some particular races. Votes are still being counted, and as of now we don’t even know for sure which party will control Congress (PredictIt currently gives Democrats a 90% chance in the Senate and a 20% chance in the House). But here are some early attempts to assess forecast accuracy. As I said, some polls were quite good:

Some polls weren’t so good, which means its important to weight better pollsters more heavily when you aggregate them. Some attempts at that were also quite good:

Oddly, some no money (Metaculus) / play money (Manifold Markets) forecasting sites seem to have done better than the real-money prediction sites:

But Who Will Build the Roads? 19th Century Edition

In the United States and much of the developed world today, most roads are publicly provided, i.e., they are built and operated by governments. This is not exclusively true, as many private toll roads exist, but the vast majority of roads are owned and operated by governments. Must it be this way?

A recent working paper by Alan Rosevear, Dan Bogart, and Leigh Shaw-Taylor looks at a very important case study: Britain in the 19th century. Britain is important because they were the leading economy in the world at the time, at the forefront of the Industrial Revolution. How were roads built and improved in England and Wales at this time? Here’s what the authors have to say in the abstract:

“non-profit organizations, known as turnpike trusts, built more new roads by attracting private investors and capable surveyors. We also show the Government Mail Road had the highest quality. Nevertheless, most turnpike trust roads were good quality, indicating their practical achievements.”

In the conclusion of the paper, they further add:

“Our analysis demonstrates that turnpike trusts were responsible for building 4,000 miles of new, good quality road in England and Wales, much of it between 1810 and 1838. On a directly comparable basis, the not-for-profit trusts built thirty times the mileage than had been built with direct Government funding during the early 1800s.”

To be clear, this paper is not a completely new discovery. It was already well-known that private companies built roads in Britain, as the authors make clear in their literature review. Similarly, there were many private turnpikes and toll roads in the US in the 19th century, as summarized in an encyclopedia entry by Klein and Majewski.

The Rosevear et al. paper adds new important details. First, they document the extent of private road building and improvements in the 19th century. Second, they show that these roads were generally of good quality, or at least they were of good quality for the time. Prior research had not documented these facts, thus making this a very important advance in our understanding of this time period. But perhaps more importantly, we see the possibility that many more roads today could be privately built and funded with user fee, especially considering that we are much, much wealthier today than 19th century Britain, we have more extensive and functional capital markets for raising the funds, etc.

The Sins of TikTok, Part 1: Extreme Privacy Theft by China-Based Company

Social media apps are nosy by nature; it is no secret that their main business model is to snoop out information about you, the user, and package and sell that information to advertisers who can target you. But there is one wildly popular app which goes beyond the norms of intrusiveness and privacy invasion AND is targeted largely at children and adolescents AND is based in China and thus is subject to Big Brother’s request for any and all data. That app is TikTok.

To avoid a bunch of re-wording, I will largely share excerpts from “ The Privacy Risks of TikTok – Why This Invasive App is So Dangerous “ by Priscilla Sherman at VPNOverview. Other articles echo her concerns with TikTok:

TikTok is an extremely popular social media video app owned by the Chinese tech company ByteDance. On TikTok, users can create and share short-form videos using a variety of filters and effects. The platform is full of dancing, comedy, and other entertaining videos….

Several agencies and news outlets are now sounding the alarm and reporting on the many problems that have surfaced. ByteDance claims to want to break away from its Chinese background in order to serve a global audience and says it will never share data with the Chinese government. This claim, however, seems impossible now that new security laws have been introduced in Hong Kong.

TikTok’s user base mostly consists of children and adolescents, which many consider to be vulnerable groups. This is a main reason for different authorities to express their worries. However, it isn’t just the youth that might be in danger from TikTok. From December 2019 onwards, U.S. military personnel were no longer allowed to use TikTok, as the app was considered a ‘cyber threat’…

[Hacker group] Anonymous has published a video listing the many dangers of TikTok. They quote a source that has done extensive research on TikTok: “Calling it an advertising platform is an understatement. TikTok is essentially malware that is targeting children. Don’t use TikTok. Don’t let your friends and family use it. Delete TikTok now […] If you know someone that is using it, explain to them that it is essentially malware operated by the Chinese government running a massive spying operation.”

These claims fit in with the recent developments surrounding TikTok. For example, Apple researchers announced that TikTok deliberately spies on users.

Claims keep piling up, showing that TikTok is a very invasive application that poses a substantial privacy risk. It seems that the data collection at TikTok goes much further than other social platforms such as Facebook or Instagram. This is surprising, since both of these companies have already faced backlash for the way they’ve dealt with user privacy. TikTok seems to collect data on a much larger scale than other social media platforms do. This, combined with TikTok’s origins makes it quite plausible that the Chinese government has insight into all of this collected data…..

Research from a German data protection website has revealed that TikTok installs browser trackers on your device. These track all your activities on the internet. According to ByteDance, these trackers were put in place to recognize and prevent “malicious browser behavior”. However, they also enable TikTok to use fingerprinting techniques, which give users a unique ID. This enables TikTok to link data to user profiles in a very targeted way.

Unfortunately, this happens with a great disregard of privacy – perhaps intentionally so. The German researchers indicate, for example, that IP addresses aren’t anonymized when TikTok uses Google Analytics, meaning your online behavior is directly linked to your IP address. An IP address provides information about your location and, indirectly, about your identity…

A user on Reddit used reverse engineering to figure out more about TikTok. Anonymous quoted the results in the video we mentioned earlier. The Reddit user discovered that TikTok collects all kinds of information:

- Your smartphone’s hardware (CPU type, hardware IDs, screen size, dpi, memory usage, storage space, etc.);

- Other apps installed on your device;

- Network information (IP, local IP, your router’s MAC address, your device’s MAC address, the name of your Wi-Fi network);

- Whether your device was rooted/jailbroken;

- Location data, through an option that’s turned on automatically when you give a post a location tag (only happens on some versions of TikTok);

Additionally, the app creates a local proxy server on your device, which is officially used for “transcoding media”. However, this is done without any form of authentication, making it susceptible to misuse….

We asked investigative journalist and writer Maria Genova about her vision on TikTok. … Genova says: “There’s a reason several countries have banned it. It’s unbelievable how much information an app like that pulls from your phone”…

TikTok needs access to your camera and microphone in order to work properly… However, there aren’t any specifications explaining how exactly these permissions are used. Therefore, TikTok could theoretically record conversations and sounds using your microphone, even when you aren’t filming a TikTok video.

We could go on and on with the technical details here, but you get the point. The fact that “IP addresses aren’t anonymized“ is really a big, bad deal. The article concludes:

The current findings and concerns surrounding TikTok are reason enough for us [the staff at VPNOverview] to remove the app from our devices. Whether TikTok’s main target group – young people between 14 and 25 – is sensitive to the privacy concerns that have come to light, remains to be seen.

Indeed.

One more quote , from Brendan Carr of the U.S. Federal Communications Commission (FCC), regarding the reliability of TikTok’s claims that they do not share data with the Chinese government:

“China has a national security law that compels every entity within its jurisdiction to aid its espionage and what they view as their national security efforts,” Carr said earlier this year, alluding to the fact that Chinese companies must make all the data they collect available to the Chinese Communist Party (CCP).

Stay tuned for Part 2, dealing with some larger market ramifications of TikTok’s evasion of Apple and Android privacy protections.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

This just in from BuzzFeed (added to original post here):

“Leaked Audio From 80 Internal TikTok Meetings Shows That US User Data Has Been Repeatedly Accessed From China”

For years, TikTok has responded to data privacy concerns by promising that information gathered about users in the United States is stored in the United States, rather than China, where ByteDance, the video platform’s parent company, is located. But according to leaked audio from more than 80 internal TikTok meetings, China-based employees of ByteDance have repeatedly accessed nonpublic data about US TikTok users — exactly the type of behavior that inspired former president Donald Trump to threaten to ban the app in the United States.

The recordings, which were reviewed by BuzzFeed News, contain 14 statements from nine different TikTok employees indicating that engineers in China had access to US data between September 2021 and January 2022, at the very least. Despite a TikTok executive’s sworn testimony in an October 2021 Senate hearing that a “world-renowned, US-based security team” decides who gets access to this data, nine statements by eight different employees describe situations where US employees had to turn to their colleagues in China to determine how US user data was flowing. US staff did not have permission or knowledge of how to access the data on their own, according to the tapes.

“Everything is seen in China,” said a member of TikTok’s Trust and Safety department in a September 2021 meeting.

On Elon, Twitter, and updating priors

I am not interested in ad hominem attacks, being a part of an internet mob, or signaling group affliation by attacking the internet’s “main character” of the day. But a significant determinant of our (hopefully always evolving) world views are how we feel about individuals who are prominent in the discourse, endowed with political power, and influential in markets. Not necessarily because we want to align or distance our selves from them as markers on a political mapping, but because at the core of our sensibilities are what we believe to be the optimal constraints and opportunities that shape the wielding of power.

<invokes best middle-aged-dude-from-a-midwestern-city-with-a-mustache accent>

Which brings me to this friggin’ guy:

- Made prescient investment in PayPal. Could be luck, but it took some real insight to see the merits of PayPal over other transactions start-ups at the time, so he’s probably a very keen observer of nascent tech companies and talent.

- Tesla was run with a deep understanding that the cars would get the attention, but the money was to be made in battery innovation while circumventing the autodealers lobby and their fully-entrenched protections against market entrants. Clever.

- He’s excellent at getting attention, even if it isn’t always positive attention. Not sure he knows the difference. Not sure it matters.

- Obsessive workaholic, possibly to the point of some mild self-destructive tendencies. Decent chance he leverages prescription amphetamines when his body and mind can’t hold onto a task as long as his ego would prefer.

- Funnier than most people think he is. Not as funny as he thinks he is.*

- Highly likely (>98%) to be very, very smart. Likely (>75%) to be an excellent engineer. Highly likely (<98%) to be an excellent pitchman.

Since then I’ve listened to people call him dumb, malevolent, and childish. I mostly disregarded those as “social media ideas”, the kind of only lightly-considered opinions that are fun to have, grant you the light dopamine drip of both feeling superior to a famous billionaire while also implicitly reminding listeners that any deficiency in your own status is at least in part a product of the unfairness and stupidity of the world. It all struck me as kind of silly and deeply unconsidered. To this point – if we accept the premise that Elon Musk is a malevolent person, then we also have to accept that the market incentives combined with targeted government subsidies harnessed the powers of a smart, dedicated, malevolent person towards the creation and management of a company that measurably reduced the amount of carbon in the atmosphere. Are there a 100 people on the planet who can be credited with a greater impact mitigating global climate change? Are the fiercest critics of Elon Musk also willing to stipulate that the (neoliberal? new liberal?) melding of markets and governance can manipulate horribly selfish people to dedicate their lives to producing massive public goods?

So yeah, my estimation was pretty strong. Then he he decided to buy Twitter. That, and his subsequent public statements, have forced my periodic reconsideration.

First, while owning Twitter could certainly be considered the stewardship of a valuable public good, it seems unlikely to be a good investment relative to the price paid. Maybe more importantly, it seems outside his comparative advantage as an investor. It’s not a moonshot and there is no engineering marvel behind the customer-facing product. It is big and already expensive, so even if it plays out incredibly well over the next ten years, it yields, what, a 15% annual return?

Second, if there’s going to be a political victory, it’s not going to happy via lobbying or creative circumvention. It will always come back to free speech, which means if a conflict happens it will be settled in the courts over many, many years. Patience and constitutional nuance do not strike me as in his comparative advantage.

It might not matter that he is getting a lot bad attenion, but it does seem like he is getting, and engaging with, too much attention. How much of his bandwidth is actually left for the other companies he ostensibly runs?

He’s saying a lot of weird stuff. Or maybe the weird fraction of his public persona is just getting a greater share of the attention. I can’t tell.

If he’s not building something or re-engineering something, he must be selling something. What is he selling? The only thing I can come up with is that he’s selling himself, just not to me. Who’s he selling himself to?

My updated beliefs, as of 11-6-2022:

- He’s probably a very keen observer of nascent tech companies and talent, but has become distracted from that comparative advantage by ego and age.

- Tesla was run with an eye towards engineering, subsidy, and sales opportunities, but that has left him overconfident in his ability to manufacture an engineering opportunity by dint of his own interest in something.

- He’s still excellent at getting attention, even if it is polarizing attention that will have negative effects on how large swaths of the population feel about him. He’s acting more like a politician than an executive.

- Obsessive, and not just about work.

- He’s still funnier than most people think he is, but his sense of humor is becoming meaner. Some people like cruelty and their admiration comes with consequences.

- Likely (>85%) to be very, very smart, but there is a growing probability (<15%) that what he is actually exceptional at is taking credit where brilliance has occurred. I’ve met a non-trivial number of people in my life who were good at “playing the part” of the genius, full of quirks and big statements and bad hair, whose real gift was standing in front of other people’s contributions. Of course, there is a certain sales and political genius in manufacturing the appearance of deep foresight.

Now that I’ve impugned (probabilistically, at leat) the capacities of a highly accomplished individual who has never done any personal harm to me or been (to my knowledge) ever accused of anything explicitly destructive, I should at least note why. I think it is important to make a regular practice of reconsidering our heroes and villains in the public sphere. It’s just good political hygiene. The sheer quantity of narratives we consume, particularly the infovores among us, is simply too much to continually process without constructing heuristic reductions of public figures: genius engineer, corrupt monster, generous savior, doddering fool, etc. And, to be clear, I think those heuristic models are probably necessary just to stay mentally afloat, but if we’re going to do that we need to update those models regularly.

I used to think Elon Musk was a tech genius whose confidence was earned and of limited consequence. Now I think he’s a tech very-smart-guy whose overconfidence has yielded an investment decision with potentiallly disasterous consequences for both his own wealth and the broader discourse in our country. Who knows what I’ll think of him next week or if I’ll even think of him at all? Maybe Elon will save an island of puppies while a genius he casually fired resurrects Tumblr into the pivotal social media of a new American golden age. We’ll have so much to reconsider!

*To be fair, neither am I.