Saturday Night Live fans were introduced to Non-Fungible Tokens (NFTs) a year ago with this skit. Most people know that an NFT is a digital ownership certificate of some asset. That could be a physical asset, or a purely digital asset, like a crude graphic of an ape wearing a sailor’s hat which people are willing to pay hundreds of thousands or millions of dollars for.

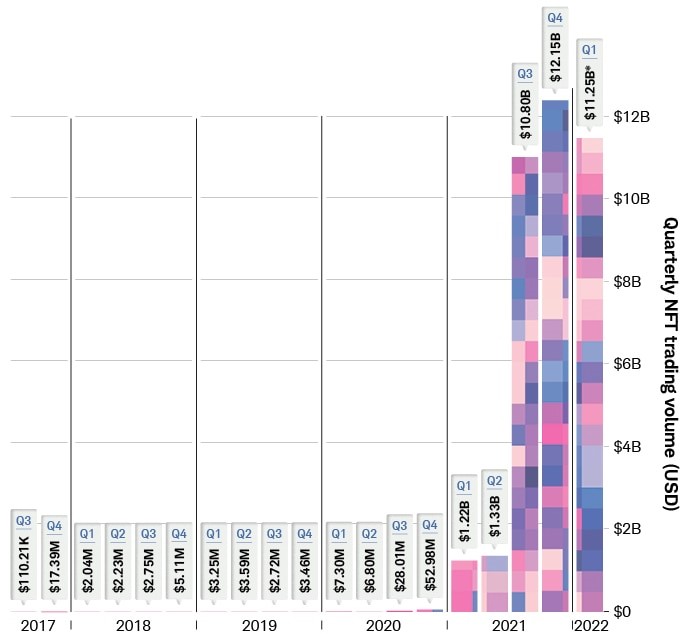

The NFT market volume exploded in the second half of 2021:

On-line chain transactions as tracked by DappRadar. Source: Schwab.

The global NFT market is projected to grow from $1.9 billion in 2021 to $5.1 billion by 2028, an annual growth rate of some 18%.

But, why??? Why would people plunk down millions of dollars for just a certificate of ownership of something which may not be particularly beautiful or functional? It is just not something that would ever occur to me.

Part of the answer must be that there are a lot of people who have a lot of money that they don’t really need. This may be a function of the ever-increasing income inequality, but we will not go down that rabbit hole. But still, assuming some 30-something has 50 grand that he doesn’t need — why spend it on an NFT?

I did a real quick search on this topic. The most common reason appears to be the same reason many people buy rare coins or rare wines or other “collectibles” – they hope that someone else will pay them a higher price in the future. There also seems to be a sense of participating in some “community”, e.g., of Bored Ape Yacht Club aficionados. Much of it comes down to the psychology of what others will pay for something, which can be often explained in hindsight, but can be hard to predict if some asset class has not yet become “hot”.

It turns out that there are some other nuances to NFTs beside just hoping some “greater fool” will pay you more for the ownership of your ape drawing five years from now. I will conclude by pasting in some excerpts from an article on the Hyperglade blog, which frames the discussion partly in terms of the familiar economic concept of scarcity:

The key value proposition that NFTs often claim is scarcity. NFTs, as their name suggests, are each inherently unique on the blockchain, i.e. they can be attributed to a specific ‘hash’ or ID. But scarcity alone doesn’t drive value – it has to be a ‘scarcity’ that people want.

One of the first types of scarcity that people want is exclusivity. Exclusivity in this context means something that is very rare and has attributes of originality. Long before NFTs existed, collectibles took center stage in this arena. For example, trading cards, comic books, and antique toys were very valuable due to their scarcity and history associated with them. For example, the Captain America Comics No. 1, from 1941 sold for over $3 million! The NFT equivalent of this would be Jack Dorsey’s first tweet, which went for $2.9 million. Jack’s tweet illustrates the quintessential NFT qualities; distinct historical moment, a special creator, and only one of them.

Collectible NFTs come in many forms (in image, audio, or video formats), but the primary category is art (e.g. the Beeple NFT), followed by music, and sports moments (e.g. NBA top shot). Subsequently, given the depth of the cultural penetration of the content involved, collectibles are the most popular reason for investing in NFTs. According to Crypto.com’s NFT survey of ~30,000 polled users, 47% of those who own NFTs bought them for collectible value. Their primary motive – to be able to ‘flip’ (sell) at a higher price.

Access to a Network

More recently however, is the emergence of NFT collections that empower communities. These collections give holders access to special privileges, primarily access to special cryptocurrency related services and benefits (e.g. higher investment rates). For example, The famous Bored Ape Yacht club holders get to attend special events, E.g. in October 2021, members celebrated annual Ape Fest in New York City, Bright Moments Gallery.

Assets in virtual worlds and gaming

If you haven’t heard of them already, Virtual digital worlds are computer-simulated environments in which users roam around using their personal avatars. So NFTs neatly solve the problem of immutable land ownership. And depending on the demand, access and foot-traffic to certain places in these simulated world prices for virtual lands have skyrocketed. For example, even the cheapest land in decentraland exceeds $10,000. In a very similar way, web 3.0 games are expanding the use case by digitizing in-game assets so that they can be physically owned by players on the blockchain. In-game assets can include characters, cards, skins, etc. a list of which you can find here.