Economics textbooks differ in their treatment of price controls. None of them does a great job, in my opinion. The reason is mostly due to the purpose of textbooks. Despite what you might suspect, most undergraduate textbooks are not used primarily to give students an understanding of the world. They are often used as a bound list of things to know and to create easy test questions. If a textbook has to change the assumptions of a model too much from what the balance of the chapter assumes, then the book fails to make clear what students are supposed to know for the test.

I think that this is the most charitable reason for books’ poor treatment of price controls – even graduate level books. The less charitable reasons include sloppy exposition due to author ignorance or an over-reliance on math. I honestly would have trouble believing these less charitable reasons.

I picked up 5 microeconomics text books and the below graph is typical of how they treat a price ceiling.

The books say that the price ceiling is perfectly enforced. They identify producer surplus (PS) as area C and consumer surplus (CS) as areas A & B. There are very good reasons to differ with these welfare conclusions.

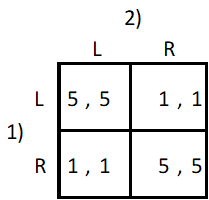

In game theory, coordination games reflects the benefits of everyone settling on the same rules. Settling on the same rules can avoid a conflict and destructive competition. For example, some rules may be arbitrary, such as on which side of the road we’ll all drive. It doesn’t much matter whether a country’s vehicles drive along the right or left side of the street. As long as everyone is in the same lane, we overwhelmingly benefit from our coordination. The matrix below describes the game.

The above game reflects that whether we agree to drive on the left or on the right is trivial and that the important detail is that we agree on what the rule is. Rules like this are arbitrary. No amount of cost benefit analysis changes the answer. Other coordination rules are seemingly arbitrary, but do have different welfare implications. For example, according to English common law, a farmer was entitled to prohibit a herdsman’s flock from trampling his crops even if the farmland had no fence. Herdsmen were responsible for corralling their flocks or paying damages if they grazed on the farm. With lots of nearby farms, total welfare was higher with a rule of cultivation rights rather than grazing rights.

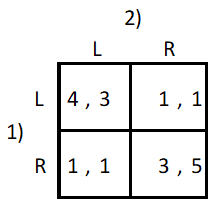

But the property rights could have been assigned to the herdsman instead. The law could have said that the sheep were free to graze with impunity and that the onus was on the farmer to build fences in order to keep the sheep at bay. In a world where there are a lot of farmers who are very nearby to one another, a small flock of sheep can do a lot of damage. And so, the cost-benefit analysis prescribes that herdsmen bear the cost of restricting the flock rather than the farmer. The matrix that describes this circumstance is below.

The above matrix reflects that agreeing on any rule is better than no rule at all. And, the rule that is selected has societal welfare implications. Choosing the ‘wrong’ rule means that we could get stuck in a rut of lower payoffs because coordinating a change in the rules is hard.

Schools

Another way in which the specific rule can be important is by whether it instantiates or works contrary to pre-existing incentives. Before compulsory schooling laws were passed, US states already had very high school attendance rates. Most parents sent their kids to school because it was a good investment. The ages at which children should be required to attend is largely, though not entirely, arbitrary. And wouldn’t you know it, most states applied their compulsory schooling legislation to the age groups for which the vast majority of children were already attending school. Enforcing a law against the natural incentives of human capital investment would have been more costly. The particular ages of compulsory schooling had different welfare implications due to the differing costs of enforcement.

I am not worried about inflation and I’m not worried about the total spending in the economy. As I’ve said previously, total spending is on track with the pre-pandemic trend and, I think, that helped us experience the briefest recession in US history. When output growth declines below trend, we face higher prices or lower incomes. The former causes inflation, the latter causes large-scale defaults. Looking at the historical record, I’m for more concerned about the latter.

I do, however, want to call special attention to the composition of the Fed’s balance sheets. Specifically, its Mortgage Backed Security (MBS) assets. Having learned from the 2008 recession, the Fed was very intent on maintaining a stable and liquid housing market. Purchasing MBS is one way that it maintained that stability. Its total MBS holdings almost doubled from March of 2020 to December of 2021 to $2.6 trillion. Should we be concerned?

At first, a doubling sounds scary. And, anything with the word ‘trillion’ is also scary. Even the graph below looks a little scary. MBS holdings by the Fed jumped and have continued to increase at about a constant rate. Is the housing market just being supported by government financing? What happens when the Fed decides to exit the market?

Luckily for us, there is precedent for Fed MBS tapering. The graph below is in log units and reflects that a similar acceleration in MBS purchases occurred in 2013. Fed net purchases were practically zero by 2015 and total MBS assets owned by the Fed were even falling by 2018. Do you remember the recession that we had in 2013 when the Fed stopped buying more MBS’s? Wasn’t 2018-2019 a rough time for the economy when the Fed started reducing its MBS holdings? No. We experienced a recession in neither 2013 nor 2018. Financial stress was low and RGDP growth was unexceptional.

Although there was no macroeconomic disruption, what about the residential sector performance during those times? Here is a worrisome proposed chain of causation:

Relative to a heavier MBS balance sheet, the Fed reducing its holdings increases supply on the MBS market.

This means that the return on creating new MBS’s falls (the price rises).

A lower return on MBS’s means that there is less demand from the financial sector for new loans from loan originators.

A tighter secondary market for mortgages decreases the eagerness with which banks lend to individuals.

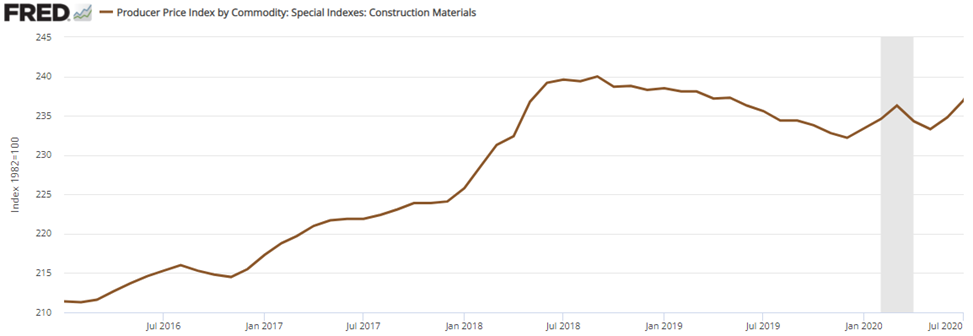

Fewer loans to individuals puts downward pressure on the demand for houses and on the price of the associated construction materials.

The data fits this story, but without major disruption.

Less eager lenders went hand-in-hand with higher mortgage rates and less residential construction spending. The substitution effect pushed more real-estate lending and spending to the commercial side. Whereas residential spending was almost the same in late 2019 as it was in early 2018, commercial real-estate spending rose 13% over the same time period.

But, importantly in the story, the income effect of a Fed disruption should have been negative, resulting in less total spending and lower construction material prices. And that’s not what happened. Total Construction spending rose and so did construction material prices. Both of these are the opposite of what we would expect if the Fed had caused disruption in the housing construction sector due to its MBS holding changes. Spending on residential construction fell understandably. But spending on commercial construction and the price of construction materials rose.

My point is that you should not listen to the hysteria.

The Fed has a variety of assets on its balance sheet and it pays special attention to the residential construction sector. Do you think that there is a residential asset bubble? Ok. Now you have to address whether the high prices are due to demand or supply. Do you suspect that the Fed unloading its MBS’s will result a popped bubble and maybe even contagion? It’s ok – you’re allowed to think that. But the most recent example of the Fed doing that didn’t result in either a macroeconomic crisis or substantial disruption in the construction markets.

The Fed has a track record and it has a reputation that serves as valuable information concerning its current and prospective activities. The next time that someone gets hysterical about Fed involvement in the housing sector, ask them what happened last time? Odds are that they don’t know. Maybe that information doesn’t matter for their opinion. You should value their opinion accordingly.

A person’s optimal choice depends on what they know. To consume more ice cream? Or to consume more alcohol? It depends on what we know about the expected utility across time. If a person thinks that alcohol has few calories, then it is understandable that they would choose to drink rather than eat. The person might be totally wrong, but they are acting optimally contingent on their knowledge about the world. (FWIW, 4oz of ethanol has 262 calories and 4oz of typical ice cream has 228 calories.)

The case is analogous for good government policy. The best policy is contingent on accessing the distribution of knowledge that’s inside of multiple people’s heads. It’s not sensible to assert that a policy is suboptimal if the optimal policy requires knowledge that neither a single individual nor all people together have. Even if the sum of all knowledge does exist, it may not be possible to access it.

Economists like to tell their undergraduate classes that it doesn’t matter who you tax. But that’s contingent on 1) identical compliance costs among buyers and sellers and 2) identical relevant information. If a tax comes as a surprise to the buyer or the seller, then it absolutely matters who is taxed.

When I was in 1st grade in North Carolina, my class went on a field trip to a Christmas tree farm. We learned a bunch about maintaining the farm and we got to choose a pumpkin to take home. At the end of our visit we took turns perusing the gift shop. My mother had generously given me a dollar to spend and I was eager to spend it (I rarely had money to spend). Unfortunately, even in the early mid-90s, most of the things in the shop cost more than $1. So, I settled on purchasing some beef jerky that cost 99 cents.

While I was listening to The New Bazaar and enjoying an episode with Tim Harford, I was reminded that economists don’t just have the job of understanding the world. We have a responsibility to our fellow man of keeping fallacy and economic misunderstanding at bay (a Sisyphean task). That doesn’t mean that we just teach economic theory. We can and should advocate for good economic policy ideas and try to think up some policy alternatives that fit our political climate.

Here I was sitting, being grumpy at the US Federal deficit, when an idea came to me. I am full of ideas. Especially unpopular ones. So, I especially like ideas that make political sense to me given that the political parties care about their policy values and re-election. Asserting that people in congress actually care about policy apart from re-election is kind of a pie-in-the-sky assertion. But, here we go none the less.

Mancur Olson liked to emphasize the role of concentrated benefits and diffused costs in political decision making. Economists point to it and explain the billion-dollar federal subsidies that go to interest groups. A favorite example is Sugar subsidies. As of 2018 there were $4 billion in subsidies and sugar growers earned $200k on average. The typical family of four pays about $50 more in subsidies each year as a result. The additional tax burden of higher sugar prices is also relatively small. Therefore, says the economist, the few sugar beet and sugar cane farmers have a large incentive to ensure the subsidy’s survival while others pay a relatively small cost to maintain it. That small cost means that there is little money saved and little gain for any individual who might try to fight the applicable legislation.

That’s the standard story. But it’s so much worse than a story of concentrated benefits and diffused costs. The laity don’t know how the world works in two important ways. First, many people will simply say that they are happy to protect American producers for an additional $50 per year. That’s a small price to pay for ensuring the employment and production of our fellow Americans, they say. An economist might reply, in a manner that so automatic that it appears smug, that that $50 would instead go to producers of other goods and that our economy would be more productive if the sugar-producing resources were diverted elsewhere. This is Bastiat’s seen and unseen. Honestly, I suspect that neither economists nor non-economists can adopt the idea without a little bit of faith.

Secondly, people don’t know what causes a particular price to change. Hayek painted this characteristic as a feature of the price system. We are able to communicate information about value and scarcity without evaluating the values of others or the actual quantity of an available resource. However, lacking causal knowledge of prices makes for some bad policies. Say that the subsidies and protections subsided and the price of US sugar declined. The consumer would likely not know anything about the subsidies in the first place, much less that they were rescinded. Further, the world is a complicated place and people are apt to thank/blame irrelevant causes otherwise (corporate greed, anyone?).

When economists blame concentrated benefits and diffused costs, they often assume that there is perfect information. THERE ISN’T. People don’t know how the world works well enough to predict with confidence what will happen in an alternate version of reality without subsidies. Nor do they understand the particular determinants of prices in our current world. Half the battle is a lack of knowledge about the functioning of the world – not just that the costs and benefits fail to provide a strong enough incentive for legislative change.

Did you notice that social media had much less traffic and activity today? It seems like even less than on Christmas.

I was instantly sick about all of the emails that went out early in the COVID times from companies that said that “we’re in this together”. Frankly – no we weren’t. Lots of people dissented and still do today.

To a great degree, we share a great deal in common. If you didn’t work today, then you probably spent time with family and friends – it’s a relatively secular holiday. Even if you did work, you probably resented it a little.

But, we do share common experiences otherwise. Make sure that you get home safely tonight. Maybe check-in on your friends in the morning. Be sure to reflect on your life from the past year. Plan like you have many years in front of you and live like you have a single day in front of you.

Economists like to hate on gift giving. Many of them consider purchasing a gift for another person as a futile attempt at imagining the preferences of another person. Given that you can’t perfectly know another person’s preferences, your gift selection will be sub-optimal. The argument goes that your friend or spouse or whomever would have been better off if you had given them money instead. Then they could have made the gift decision fully equipped with the information that is necessary to make them happiest.

There are some obvious things that are glossed over. Purchasing a good gift – or even writing a card – carries a big load of signaling value. People like to be liked and receiving a good gift signals that the giver cared enough to research appropriate gifts. Also, receiving money as a gift puts the onus of research and transaction costs on the receiver. If the recipient’s value of time is adequately high, then cash payments are even more resource destructive than giving a non-pecuniary gift. Especially if there is an expectation that the giver will later enquire about how the funds were used. At that point, the giver is saddling the recipient with all of the anxieties and costs of choosing a gift that makes another person happy.

But I want to talk about a non-obvious benefit of gift giving.

First, I want to talk about student loans (I promise, it’s relevant). Plenty of people argue that college students don’t understand debt and that they therefore don’t understand the future cost that they will bear by borrowing. When the lender is the department of education, there is no defaulting with the hope of bankruptcy. The debt will get repaid…. So far anyway.

If it’s true that students don’t understand debt, then we can appropriately construe future student loan payments as lump-sum costs. Of course there is deferment and forbearance – but put those to the side. The bottom line is that, almost regardless of a debtor’s activities, they must repay their debt. It doesn’t matter how the debtor earns or consumes, the debt must be paid. This fits the description of a lump-sum cost. Usually, things like lump-sum taxes are hypothetical and unpopular among the laity. But, if we accept that the decision-making-student has incomplete information in regard to the debt’s future payment implications, then the debt payments are exogenous and unavoidable from the future debtor’s perspective.

This is a good thing for the productivity of our economy. Because people are making tradeoffs between the two goods of leisure and consumption, a lump-sum tax causes individuals to work more than they would have worked otherwise. Lump-sum taxes don’t reduce the marginal benefit of working. Essentially, a debtor’s first several hours of work pay-off his debt first and then he gets to work for his own consumption.

Importantly, this ignores any human capital effects of the education. It doesn’t matter whether education actually makes people more productive. The seemingly exogenous debt payments cause debtors to work more and produce more for others. The RGDP per capita of our economy rises and we know that most of the benefits of work do not accrue to producers. Student debt, with the accompanying assumptions laid out above, therefore increases our incomes because it acts as a lump-sum tax.

Now it’s time to save presents from the economists.

As families get older and siblings drift apart, gift-giving begins to become less exciting. I’m tempted to say there is a natural process in which the first couple of adult-sibling Christmases include decent gifts. Then, the gifts become not-so-great as siblings become less familiar with each others’ preferences. Knowing this and still wanting to give a suitable gift, siblings may turn to gift cards. The less that a sibling knows the preferences of another, the more general the gift card.

If you’ve grown more distant from your brothers/sisters and you know that you’ll receive a gift, then it’ll probably be an Amazon, or Walmart, or some other gift card that permits spending on a broad variety of gifts. There comes a point when you’re spending $X on gift cards each year where $X = $x(n). That is, you’re spending some amount on each sibling for a total of $X each year. And for the sake of social cohesion and norms, all of your siblings are doing the same thing and spending the same amounts.

Importantly, you don’t control the social norms, nor your number of siblings. It might seem like you’re all just trading dollar bills at a unitary exchange rate, leaving no-one better or worse-off. But, trading cash is gauche. So, distant siblings trade broadly attractive gift cards in order to achieve that gift-like aura.

Social norms also say that gift giving is not a trade. If you don’t receive a gift, then you’re supposed to be ‘ok’ with that. So, each year you will spend $X on gift cards for your distant siblings and there is some probability that you get nothing in return. If you can’t control the number of siblings that you have and you can’t control whether you receive a gift card in return, then giving cash or cash-like gift cards to your siblings each year is a lot like a lump-sum cost. Socially – or maybe morally – you shouldn’t just ignore your siblings and it is incumbent upon you to give a gift.

Having to give away a lump-sum of money or money-like things no matter what else you do is a lump-sum cost. If people bear lump-sum costs, then they will work a little bit more and produce a little bit more for society. If gifts suboptimal but at least considered a ‘good’, then we’re better off: we work more to make others somewhat better off with resources that wouldn’t exist if we hadn’t chosen to give to others.

There are some caveats, of course. Economists are often not so popular at parties for a variety of reasons. One reason is that they flout social conventions. An economist might scoff at the social constraints as unbinding. Others would disagree. Another point of contention may be that an individual can choose to work no more, but to invest less instead. But this really just pushes the problem off until the individual has less income in the future and works more to compensate for it at a later time. A 3rd caveat is that we can choose the amount that we spend in others. But that just implies that at least part of the gift giving ritual isn’t a lump-sum cost. It does not imply that none of gifting giving is a lump sum cost.

Regardless, the social convention of giving gifts can provide for a Schelling point that makes us a more productive as a society. We spend on others, to a great degree beyond our individual control, in order to avoid severe social stigma. And, if we can’t control all of who counts as a worthy recipient of gifts, then we have a lump-sum cost to some degree. Giving gifts makes sense as a productive convention because it makes us a richer as part of a general equilibrium – if not a partial equilibrium. Merry Christmas.

I remember people talking about Covid-19 in January of 2020. There had been several epidemic scare-claims from major news outlets in the decade prior and those all turned out to be nothing. So, I was not excited about this one. By the end of the month, I saw people making substantiated claims and I started to suspect that my low-information heuristic might not perform well.

People are different. We have different degrees of excitability, different risk tolerances, and different biases. At the start of the pandemic, these differences were on full display between political figures and their parties, and among the state and municipal governments. There were a lot of divergent beliefs about the world. Depending on your news outlet of choice, you probably think that some politicians and bureaucrats acted with either malice or incompetence.

I think that the Federal Reserve did a fine job, however. What follows is an abridged timeline, graph by graph, of how and when the Fed managed monetary policy during the Covid-19 pandemic.

February, 2020: Financial Markets recognize a big problem

The S&P begins its rapid decent on February 20th and would ultimately lose a third of its value by March 23rd. Financial markets are often easily scared, however. The primary tool that the Fed has is adjusting the number of reserves and the available money supply by purchasing various assets. The Fed didn’t begin buying extra assets of any kind until mid-March. There is a clear response by the 18th, though they may have started making a change by the 11th. One might argue that they cut the federal funds rate as early as the 4th, but given that there was no change in their balance sheet, this was probably demand driven.

March, 2020: The Fed Accommodates quickly and substantially.

In the month following March 9th, the Fed increased M2 by 8.3%. By the week of March 21st, consumer sentiment and mobility was down and economic policy uncertainty began to rise substantially – people freaked out. Although the consumer sentiment weekly indicator was back within the range of normal by the end of April, EPU remained elevated through May of 2020. Additionally, although lending was only slightly down, bank reserves increased 71% from February to April. Much of that was due to Fed asset purchases. But there was also a healthy chunk that was due to consumer spending tanking by 20% over the same period.

In the 18 months prior to 2020, M2 had grown at rate of about 0.5% per month. For the almost 18 months following the sudden 8.3% increase, the new growth rate of M2 almost doubled to about 1% per month. The Fed accommodated quite quickly in March.

April, 2020: People are awash with money

Falling consumption caused bank deposit balances to rise by 5.6% between March 11th and April 8th. The first round of stimulus checks were deposited during the weekend of April 11th. That contributed to bank deposits rising by another 6.7% by May 13th.

By the end of March, three weeks after it began increasing M2, the Fed remembered that it really didn’t want another housing crisis. It didn’t want another round of fire sales, bank failures, disintermediation, collapsed lending, and debt deflation. It went from owning $0 in mortgage-backed securities (MBS) on March 25th to owning nearly $1.5 billion worth by the week of April 1st. Nobody’s talking about it, but the Fed kept buying MBS at a constant growth rate through 2021.

May, 2020 – December, 2021: The Fed Prevents Last-Time’s Crisis

Jerome Powell presided over the shortest US recession ever on record. The Fed helped to successfully avoid a housing collapse, disintermediation, and debt deflation – by 2008 standards. The monthly supply of housing collapsed, but it had bottomed out by the end of the summer. By August of 2021, the supply of housing had entirely recovered. The average price of new house sales never fell. Prices in April of 2020 were typical of the year prior, then rose thereafter. A broader measure of success was that total loans did not fall sharply and are nearly back to their pre-pandemic volumes. After 2008, it took six years to again reach the prior peak. A broader measure still, total spending in the US economy is back to the level predicted by the pre-pandemic trend.

The Fed can’t control long-run output. As I’ve written previously, insofar as aggregate demand management is concerned, we are perfectly on track. The problem in the US economy now is real output. The Fed avoided debt deflation, but it can’t control the real responses in production, supply chains, and labor markets that were disrupted by Covid-19 and the associated policy responses.

What was the cost of the Fed’s apparent success? Some have argued that the Fed has lost some of its political insulation and that it unnecessarily and imprudently over-reached into non-monetary areas. Maybe future Fed responses will depend on who is in office or will depend on which group of favored interests need help. Personally, I’m not so worried about political exposure. But I am quite worried about the Fed’s interventions in particular markets, such as MBS, and how/whether they will divest responsibly.

Of course, another cost of the Fed’s policies has been higher inflation. During the 17 months prior to the pandemic, inflation was 0.125% per month. During the pandemic recession, consumer prices dipped and inflation was moderate through November. But, in the 16 months since April of 2020, consumer prices have grown at a rate of 0.393% per month – more than three times the previous rate. Some of that is catch-up after the brief fall in prices.

Although people are genuinely worried about inflation, they were also worried about if after the 2008 recession and it never came. This time, inflation is actually elevated. But people were complaining about inflation before it was ever perceptible. The compound annual rate of inflation rose to 7% in March of 2021. But it had been almost zero as recent as November, 2020. That March 2021 number is misleading. The actual change in prices from February to March was 0.567%. Something that was priced at $10 in February was then priced at $10.06 in March. Hardly noticeable, were it not for headlines and news feeds.

Opinions on game theory differ. To most of the public, it’s probably behind a shroud of mystery. To another set of the specialists, it is a natural offshoot of economics. And, finally a 3rd non-exclusive set find it silly and largely useless for real-world applications.

Regardless of the camp to which you claim membership, the Pure Strategy Nash Equilibrium (PSNE) is often misunderstood by students. In short, the PSNE is the set of all player strategy combinations that would cause no player to want to engage in a different strategy. In lay terms, it’s the list of possible choices people can make and find no benefit to changing their mind.

In class, I emphasize to my students that a Nash Equilibrium assumes that a player can control only their own actions and not those of the other players. It takes the opposing player strategies as ‘given’.

This seems simple enough. But students often implicitly suppose that a PSNE does more legwork than it can do. Below is an example of an extensive form game that illustrates a common point of student confusion. There are 2 players who play sequentially. The meaning of the letters is unimportant. If it helps, imagine that you’re playing Mortal Kombat and that Player 1 can jump or crouch. Depending on which he chooses, Player 2 will choose uppercut, block, approach, or distance. Each of the numbers that are listed at the bottom reflect the payoffs for each player that occur with each strategy combination.

Again, a PSNE is any combination of player strategies from which no player wants to deviate, given the strategies of the other players.

Students will often proceed with the following logic:

Player 2 would choose B over U because 3>2.

Player 2 would choose A over D because 4>1.

Player 1 is faced with earning 4 if he chooses J and 3 if he chooses C. So, the PSNE is that player 1 would choose J.

Therefore, the PSNE set of strategies is (J,B).

While students are entirely reasonable in their thinking, what they are doing is not finding a PSNE. First of all, (J,B) doesn’t include all of the possible strategies – it omits the entire right side of the game. How can Player 1 know whether he should change his mind if he doesn’t know what Player 2 is doing? Bottom line: A PSNE requires that *all* strategy combinations are listed.

The mistaken student says ‘Fine’ and writes that the PSNE strategies are (J, BA) and that the payoff is (4,3)*. And it is true that they have found a PSNE. When asked why, they’ll often reiterate their logic that I enumerate above. But, their answer is woefully incomplete. In the logic above, they only identify what Player 2 would choose on the right side of the tree when Player 1 chose C. They entirely neglected whether Player 2 would be willing to choose A or D when Player 1 chooses J. Yes, it is true that neither Player 1 nor Player 2 wants to deviate from (J, BA). But it is also true that neither player wants to deviate from (J, BD). In either case the payoff is (4, 3).

This is where students get upset. “Why would Player 2 be willing to choose D?! That’s irrational. They’d never do that!” But the student is mistaken. Player 2 is willing to choose D – just not when Player 1 chooses C. In other words, Player 2 is indifferent to A or D so long as Player 1 chooses J. In order for each player to decide whether they’d want to deviate strategies given what the other player is doing, we need to identify what the other player is doing! The bottom line: A PSNE requires that neither player wants to deviate given what the other player is doing – Not what the other player would do if one did choose to deviate.

What about when Player 1 chooses C? Then, Player 2 would choose A because 4 is a better payoff than 1. Player 2 doesn’t care whether he chooses U or B because (C, UA) and (C, BA) both provide him the same payoff of 4. We might be tempted to believe that both are PSNE. But they’re not! It’s correct that Player 2 wouldn’t deviate from (C, BA) to become better off. But we must also consider Player 1. Given (C, UA), Player 1 won’t switch to J because his payoff would be 1 rather than 3. Given (C, BA), Player 1 would absolutely deviate from C to J in order to earn 4 rather than 3. So, (C, UA) is a PSNE and (C, BA) is not. The bottom line: Both players must have no incentive to deviate strategies in a PSNE.

There are reasons that game theory as a discipline developed beyond the idea of Nash Equilibria and Pure Strategy Nash Equilibria. Simple PSNE identify possible equilibria, but don’t narrow it down from there. PSNE are strong in that they identify the possible equilibria and firmly exclude several other possible strategy combinations and outcomes. But PSNE are weak insofar as they identify equilibria that may not be particularly likely or believable. With PSNE alone, we are left with an uneasy feeling that we are identifying too many possible strategies that we don’t quite think are relevant to real life.

These features motivated the later development of Subgame Perfect Nash Equilibria (SGPNE). Students have a good intuition that something feels not quite right about PSNE. Students anticipate SGPNE as a concept that they think is better at predicting reality. But, in so doing, they try to mistakenly attribute too much to PSNE. They want it to tell them which strategies the players would choose. They’re frustrated that it only tells them when players won’t change their mind.

Regardless of whether you get frustrated by game theory, be sure to have a drink and make toast to John Nash.

*Below is the normal form for anyone who is interested.

Whether one might socially offend us or whether one commits a crime, we face a fundamental tension between punishment and forgiveness. Punishment is important because it acts as a deterrent to the initial offense or to subsequent offenses. But punishment is also costly. Severing social or commercial ties reduces the number of possible mutually beneficial transactions. We lose economies of scale and lose gains from trade when we exclude someone from the market. Forgiveness is important because it permits those who previously had conflict to acknowledge the sunk cost of the offense and proceed with future opportunities for trade. However, an excess of forgiveness risks failure to deter destructive behaviors.

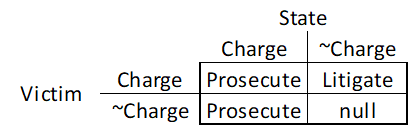

In the US, we enjoy a state that can prosecute alleged offenders and enforce punishments regardless of the economic status of the offended. While not perfect, the state incurs great cost by being the advocate of those who could not enforce great retributive punishment by their own means. A victim may choose to press charges against an offender, or the state can press charges despite a permissive victim.

In fact, our system of prosecution is somewhat asymmetrical. The state can press charges against a suspect, regardless of the victim’s wishes. While a victim can’t compel an unwilling state to press charges, say if the evidence is scant, an individual can engage in litigation against the accused.

Most of the possible combinations of victim and state strategies result in some kind of prosecution of the alleged offender. Except for litigation, our punishments in the US tend not to be remunerative – the victim isn’t compensated for the evils of the offender. ‘Justice’ is often construed as a type of compensation, however.