A periodically recurring conversation on social media is whether imports are bad for GDP. Everyone thinks they are clearly right, and then they lazily defer to brief dismissal of the opposing view. Some of this might be due to media format. Something just a tiny bit more thorough could help to resolve the painfully unproductive online interactions… And just maybe improve understanding.

It starts with the GDP expenditure identity:

The initial assertion is that imports reduce GDP. After all, M enters the equation negatively. So, all else constant, an increase in M reduces Y. It’s plain and simple.

Many economists reply that the equation is an accounting identity and not a theory about how the world works and that the above logic is simply confusing these two things. This reply 1) allows its employers to feel smart, 2) doesn’t address the assertion, & 3) doesn’t resolve anything. In fact, this reply erects a wall of academic distinction that prevents a resolution. What a missed opportunity to perform the literal job of “public intellectual”.

How are Imports Bad/Good/Irrelevant for GDP?

Let’s add a small but important detail to the above equation to distinguish between consumption of goods produced domestically and those produced elsewhere.

There are 62 songs called “Better Man” just on Ultimate Guitar (which doesn’t claim to be comprehensive), plus many more slight variations like “A Better Man” or “Better Man Blues”. Some of these are obscure, but many are from well-known artists including Taylor Swift, Oasis, Ellie Goulding, Justin Bieber, and Pearl Jam; one by Robbie Williams inspired a major motion picture also called Better Man.

Meanwhile there is only one song on Ultimate Guitar called “Better Woman”, plus one variation (“A Better Woman”), both from artists I hadn’t heard of (Sera Cahoone and Beccy Cole). Why such an extreme difference?

Is it that men are the ones who are terrible and need improvement? Or are men the ones who see hope for improvement, while women can’t change or don’t want to? Let’s consider what the lyrics have to say about this. Reading though them all I saw a few recurring categories of “Better Man”:

Wish I Were Better: I count 33 of the 62 songs in this category. A man singing about how he wishes he were better, usually because of a woman, the classic “You Make Me Want to Be a Better Man“. Sometimes this is hopeful that he will be, sometimes regretful that he hasn’t been or despairing that he won’t be. Occasionally the inspiration to be better comes from someone other than a woman he’s in love with, such as Jesus, his dad, or his kids.

You Make Me Better: 13/62. Same idea as the last category, except the man has already become better. Again usually because of a woman, but sometimes because of someone else like God or his kids or his friends. Another 3 are a variation of this, I Got Better, where the man changed without anyone’s help or for a woman who isn’t convinced he really changed.

Wish You Were a Better Man: 4/62, but includes the hit by Taylor Swift. A woman wishes a man she loved were better. Another 2 songs including the Pearl Jam hit are a variant of this, Can’t Find A Better Man, where a woman stays with a bad man because she doesn’t see a better choice. Steven Seagal (yes, that Steven Seagal) reverses things and sings that a woman should leave him because she can do better. Then there’s 1 example of the genre where Hellyeah wishes his father were a better man.

One-offs: There are a few 1-off “Better Man” songs that seem to be in a category of their own: Beth Hart’s celebration of finding a better man, Ellie Goulding‘s odd insistence that “I’m the better man” (even though she’s a woman), and Ryan Innes’ entry which is the closest anyone comes to saying they wish they were a worse man. By the way, there appear to be zero songs out there called “Worse Man”- perhaps some day I’ll write one, but its a free idea and I’d be happy to see one of you beat me to it.

What about our 2 “Better Women”?Sera Cahoone’s song (the only one with the exact title “Better Woman”) is a standard “Wish I Were Better” entry, just as a woman (though the person she wants to be better for might still be a woman as usual):

So I step on up and be a better woman in your eyes From now on I’m gonna love everything about you

Beccy Cole’s “A Better Woman” concludes that she doesn’t actually want or need to become a better woman:

I ain’t changin’ nothin’ Just to have your lovin’ Yeah, I’m alright with who I am I don’t need to be a better woman – I just need a better man

The boring explanation for the gender discrepancy is that “Better Man” just scans better rhythmically. But I don’t think can explain a 60-2 (or 60-1 if we’re being strict) difference, and there seems the be a big underlying difference in the prevalence of these themes for men and women, not just titles. This matches up with the classic sayings from Camille Paglia:

A woman simply is, but a man must become

Or this one often attributed (probably incorrectly) to Einstein:

Women marry hoping that the man will change. Men marry hoping the woman will stay the same. Both are usually disappointed.

Whatever the cause, you can find the playlist I made of all 60 “Better Man” songs I could find on Youtube Music here:

I liked most of them (surprisingly given the range of genres and the fact that I hadn’t heard of most of the artists), but my favorite in this vein is to forget being a Better Man or Better Woman, and instead be “A Better Son/Daughter” like Rilo Kiley says:

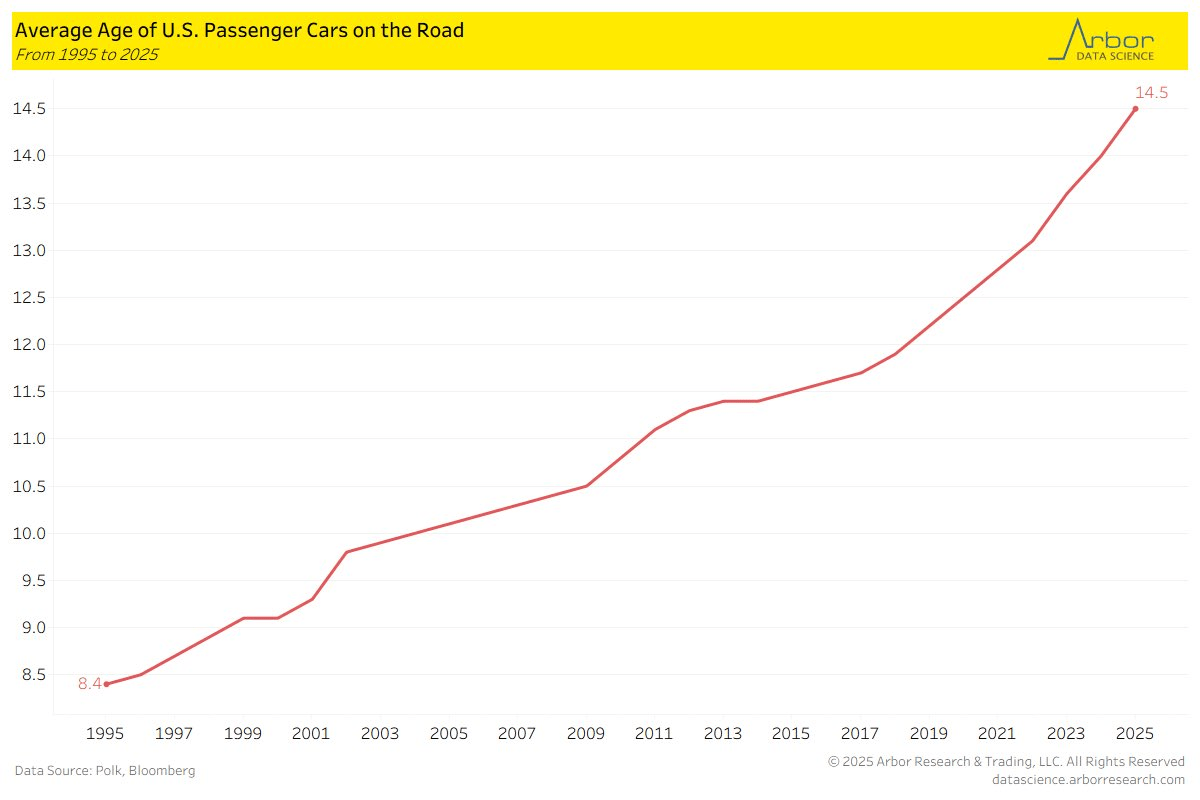

The following chart from Arbor Research shows that the average age of cars on the road in the US is 14.5 years. If we go back to 1995, it was almost half that, and the increase has been steady since over the past 30 years. Similar data from the Bureau of Transportation Statistics confirms these numbers.

Why would this be? I see two primary explanations that are possible. One is that cars are becoming more reliable (better quality), so consumers are happy to drive them longer. The other is that cars today are less affordable, so people are only hanging onto old cars because they are forced to. One of these is a happy explanation, one is consistent with a narrative of stagnation. Which is true?

On the affordability question, we do have some good data, but it points in the opposite direction: cars are much more affordable today than in 1995, or even before that.

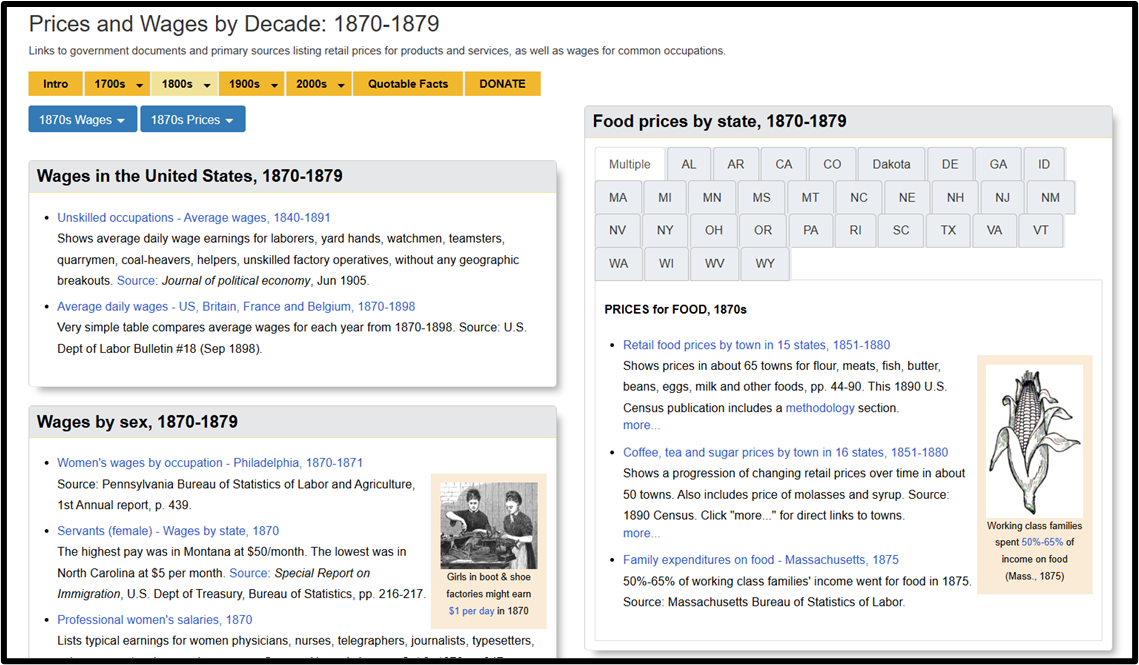

Today I’m just sharing a truly awe-inspiring resource. The University of Missouri has what is essentially a central clearinghouse for prices and wages. If you want the price of anything, then they should be your first stop.

See the screenshot at the bottom. The website links to the original sources for household consumption prices, occupation wages, etc. They make it easy to cut the data by date, industry, location, etc. Because they cite their sources, you can see some data series that are not even available on FRED – without having to perform the painful sleuthing on a government website.

I especially like this site for its historical data. One of the challenges of historical US data is that individual cities may not have prices that are representative of the national levels or trends. Lower levels of market integration make representative samples even more important than in modern data. But really, that was more of a concern for 20th century researchers. Now, we love our panel data. So, the historically less integrated markets of the US provide ‘toy economies’ that include greater regionalism and local shocks.

Although David Jacks has loads of tabulated data, he doesn’t have it all. The Missouri library site links to PDFs of original statistical publications which, while digitized, have never been tabulated into useable data fit for modern researchers.

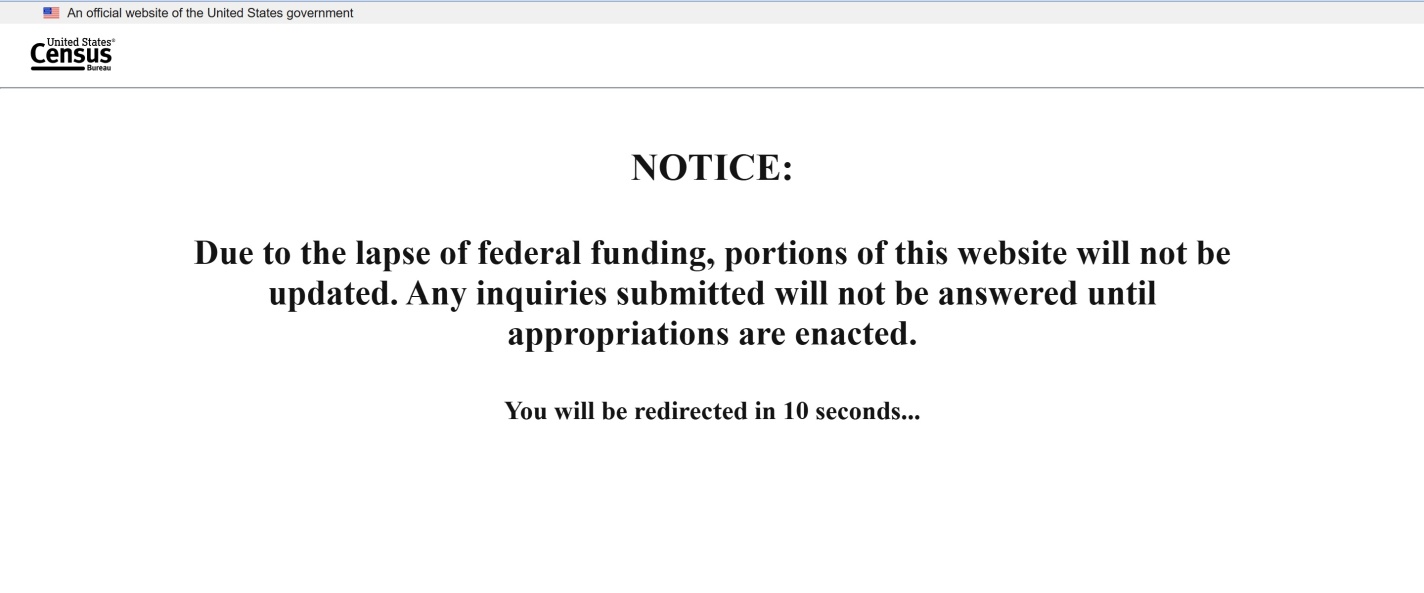

Datasets can be pulled offline for all sorts of reasons. As I wrote in February, this shows the value of being a data hoarder– just downloading now any data you think you might want later:

Several major datasets produced by the federal government went offline this week…. This serves as a reminder of the value of redundancy- keeping datasets on multiple sites as well as in local storage. Because you never really know when one site will go down- whether due to ideological changes, mistakes, natural disasters, or key personnel moving on.

The US Federal government shutdown this month provides another reminder of this. So far most datasets are still up, but I’ve seen some availability issues:

The good news is that a number of institutions have stepped up in 2025 to host at-risk datasets (joining those like IPUMS, NBER, and Archive.org that have been hosting datasets for many years, but are scaling up to meet the moment):

Restore CDC hosts all CDC data as it was in January 2025.

Harvard Library’s project is less user-friendly but more powerful, archiving all 16 terabytes of Data.gov.

Yesterday on Twitter I shared a chart showing the age at first marriage for white men and women in the US, with data going back to 1880. I pointed out an interesting fact: at least for men, the age was essentially the same in 1890 and 1990 (27), though for women it was a bit higher in 1990 than in 1890 (by about 1 year).

This Tweet generated quite a bit of interest (over 800,000 impressions so far), and (of course!) a lot of skeptical responses. One skeptical response is that I cut off the data in 1990, when trends since then have shown continuously rising ages at first marriage, and by 2024 the comparable figures were much higher than in 1890 (by about 4 years for men and 6.5 years for women). In one sense, guilty as charged, though I only came across this data when looking through the Historical Statistics of the US, Millennial Edition, and that was the most current data available when it was printed. Here is a more updated chart from Census:

But there is another interesting fact about that data: the massive decline age of first marriage in the first half of the 20th century. Between 1890 and 1960, the median age at first marriage fell by about 3 years for men and 2 years for women. For men, most of the decline (about 2 years) had already happened by 1940. Thus, if we start from the low-point of the 1950s and 1960s (as many charts do, such as this one), it appears marriage is continuously getting less common in US history, while the fuller picture shows a U-shaped pattern.

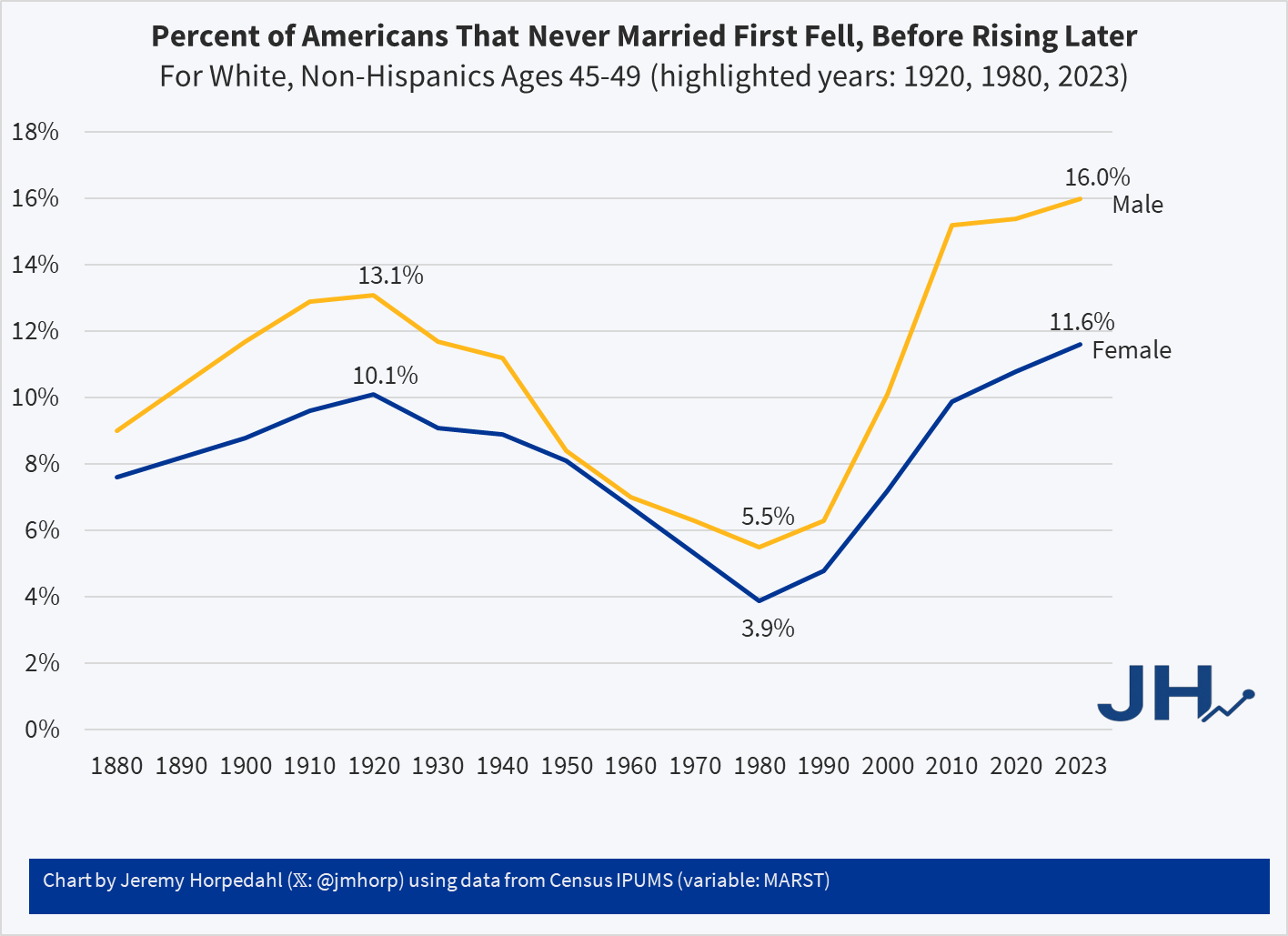

This same pattern shows up in another measure of marriage data: the percentage of people that never get married. If we look at White, Non-Hispanic Americans in their late 40s, the picture looks something like this (keen observers will note that the Hispanic distinction is a modern one dating from the 1970s, but Census IPUMS has conveniently imputed this classification back in time based on other demographic characteristics):

Looking at people in their late 40s is useful because, at least for women, they are past their childbearing years. And using, say, the late 50s age group doesn’t alter the picture much: even though some people get married for the first time in their 50s, it’s always been a small number.

Here we can see an even more dramatic pattern. 100 years ago, it was not super rare for people to never marry: over 1/10 of the population didn’t! But by 1980 (thus, for people born in the early 1930s), it was much rarer: less than 4% of women were never married (among White, Non-Hispanics). In fact, the peak in 1920 of 10% unmarried women wasn’t surpassed again until 2013! And it’s not substantially higher today than 1920 for women, especially when considering the full swing downward. Men are quite a bit higher today, though the 1920 peak of 13% wasn’t surpassed again until 2006.

For a measure that peaks in 1920, we might wonder if new immigrants are skewing the data in some way, given that this is right at the end of about 4 decades of mass immigration. But just the opposite: if we focus on native-born women, the 1920 level was even higher at 11.1%, which wasn’t surpassed until 2022, and even in the latest figures it is less than 1 percentage point higher than 1920.

Precisely why we observed this U-shaped pattern in marriage (both first age and ever married) is debated among scholars, though my sense among the general public is that it isn’t much thought about. Most people (from my casual observation) seem to assume that marriage rates and ages were always lower in the past, and that modern times are the outliers. But in reality, the middle part of the 20th century seems to be the outlier. The “Baby Boom” of roughly 1935-1965 is possibly better understood as a “Marriage Boom,” with more babies naturally following from more and younger marriages.

Academics generally agree on the changing patterns of mortality over time. Centuries ago, people died of many things. Most of those deaths were among children and they were often related to water-borne illness. A lot of that was resolved with sanitation infrastructure and water treatment. Then, communicable diseases were next. Vaccines, mostly introduced in the first half of the 20th century, prevented a lot of deaths.

Similarly, food borne illness killed a lot of people before refrigeration was popular. The milkman would deliver milk to a hatch on the side of your house and swap out the empty glass bottles with new ones full of milk. For clarity, it was not a refrigerated cavity. It was just a hole in the wall with a door on both the inside and outside of the house. A lot of babies died from drinking spoiled milk.

Now, in higher income countries, we die of things that kill old people. These include cancer, falls that lead to infections, and the various diseases related to obesity. We’re able to die of these things because we won the battles against the big threats to children.

What prompts such a dreary topic?

I was perusing the 1870 Census schedules and I stumbled upon some ‘Schedule 2s’. Most of us are familiar with schedule 1, which asks details about the residents living in a household. But schedule 2 asked about the deaths in the household over the past year. Below is a scan from St. Paul, Minnesota.

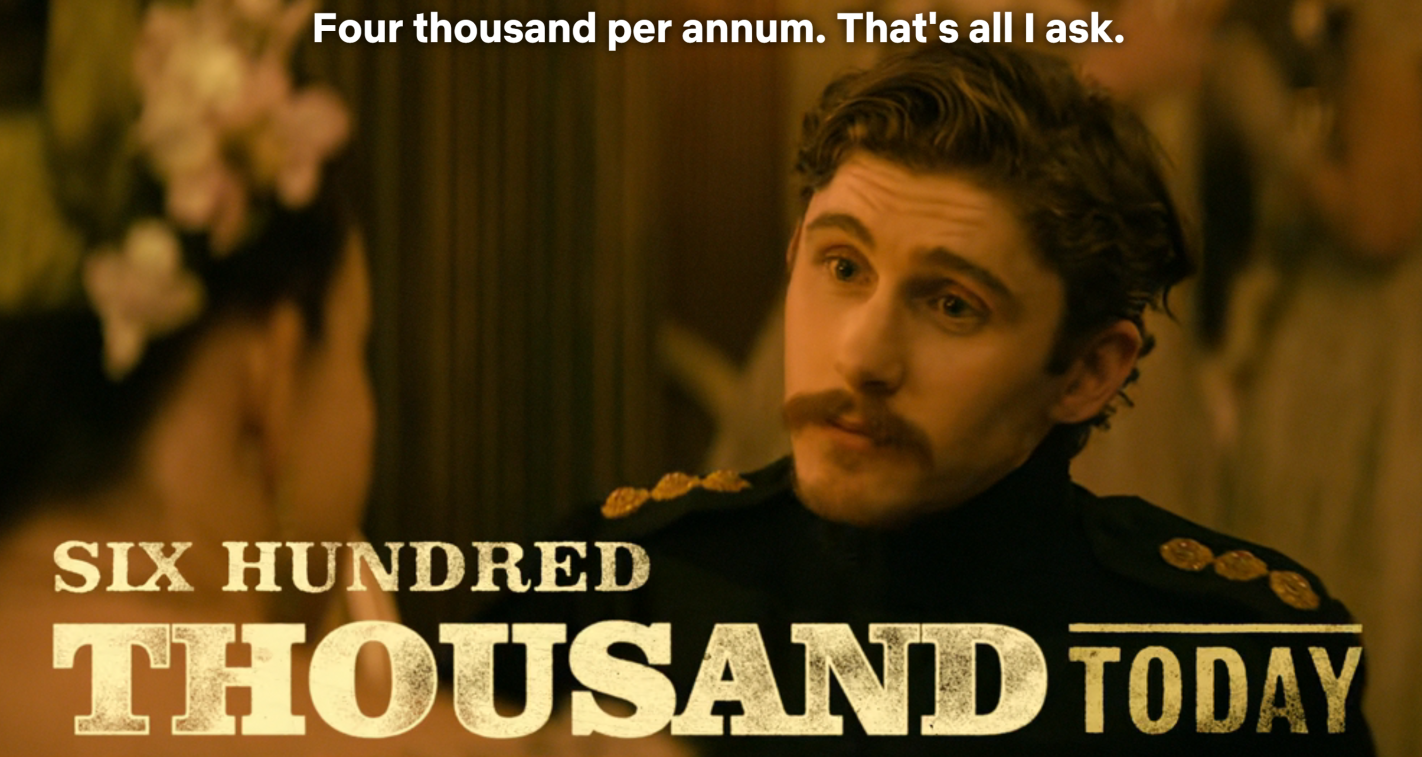

When reading an old novel or watching a period drama movie or TV show, it is almost inevitable that some historical currency amounts will be mentioned. This is especially true when the work is dealing with money and wealth, for example the series “The Gilded Age” is about rich people in late 19th century America. So money comes up a lot. I wrote a post a few weeks ago trying to contextualize a figure of $300,000 from 1883 for that show.

A new Netflix series “The House of Guinness” is another period piece that spends a lot of time focusing on rich people (the family that produces the famous beer), as well as their interactions with poorer folks. So of course, there are plenty of historical currency values mentioned, this time denominated in British pounds (the series is primarily set in Ireland, where the pound was in use). On this series, though, they have taken the interesting approach of giving the viewers some idea of what historical currency values are worth today, by overlaying text on the screen (the same way they translate the Gaelic language into English).

For example, in Episode 4 of the first season, one of the Guinness brothers is attempting to negotiate his annual payment from the family fortune. He asks for 4,000 pounds per year. On the screen the text flashes “Six Hundred Thousand Today.”

The creators of the show are to be commended for giving viewers some context, rather than leaving them baffled or pausing the show to Google it. But is 600,000 pounds today a good estimate? Where did they get this number? As with the “Gilded Age” estimate, it’s complicated, but it is probably more than you think.

My new article, “Prohibition and Percolation: The Roaring Success of Coffee During US Alcohol Prohibition”, is now published in Southern Economic Journal. It’s the first statistical analysis of coffee imports and salience during prohibition. Other authors had speculated that coffee substituted alcohol after the 18th amendment, but I did the work of running the stats, creating indices, and checking for robustness.

My contributions include:

National and state indices for coffee and coffee shops from major and local newspapers.

A textual index of the same from book mentions.

I uncover that prohibition is when modern coffee shops became popular.

The surge in coffee imports was likely not related to trade policy or the end of World War I

Both demand for coffee and supply increased as part of an intentional industry effort to replace alcohol and saloons.

An easy to follow application of time series structural break tests.

An easy to follow application of a modern differences in differences method for state dry laws and coffee newspaper mentions.

Evidence from a variety of sources including patents, newspapers, trade data, Ngrams, naval conflicts, & Wholesale prices.

Generally, the empirical evidence and the main theory is straightforward. I learned several new empirical methods for this paper and the economic logic in the robustness section was a blast to puzzle-out. Finally, it was an easy article to be excited about since people are generally passionate about their coffee.

Bartsch, Zachary. 2025. “Prohibition and Percolation: The Roaring Success of Coffee During US Alcohol Prohibition.” Southern Economic Journal, ahead of print, September 22. https://doi.org/10.1002/soej.12794.

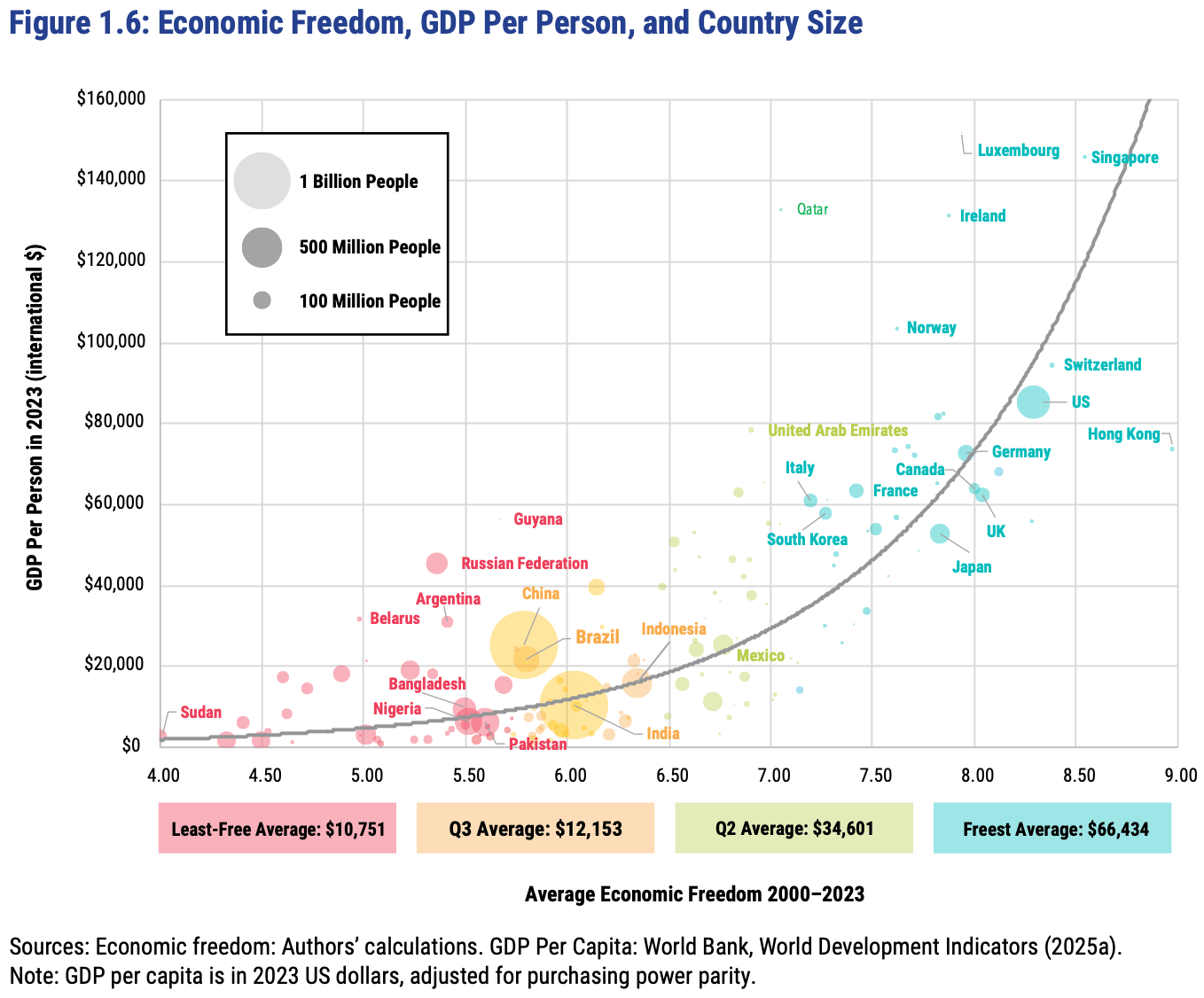

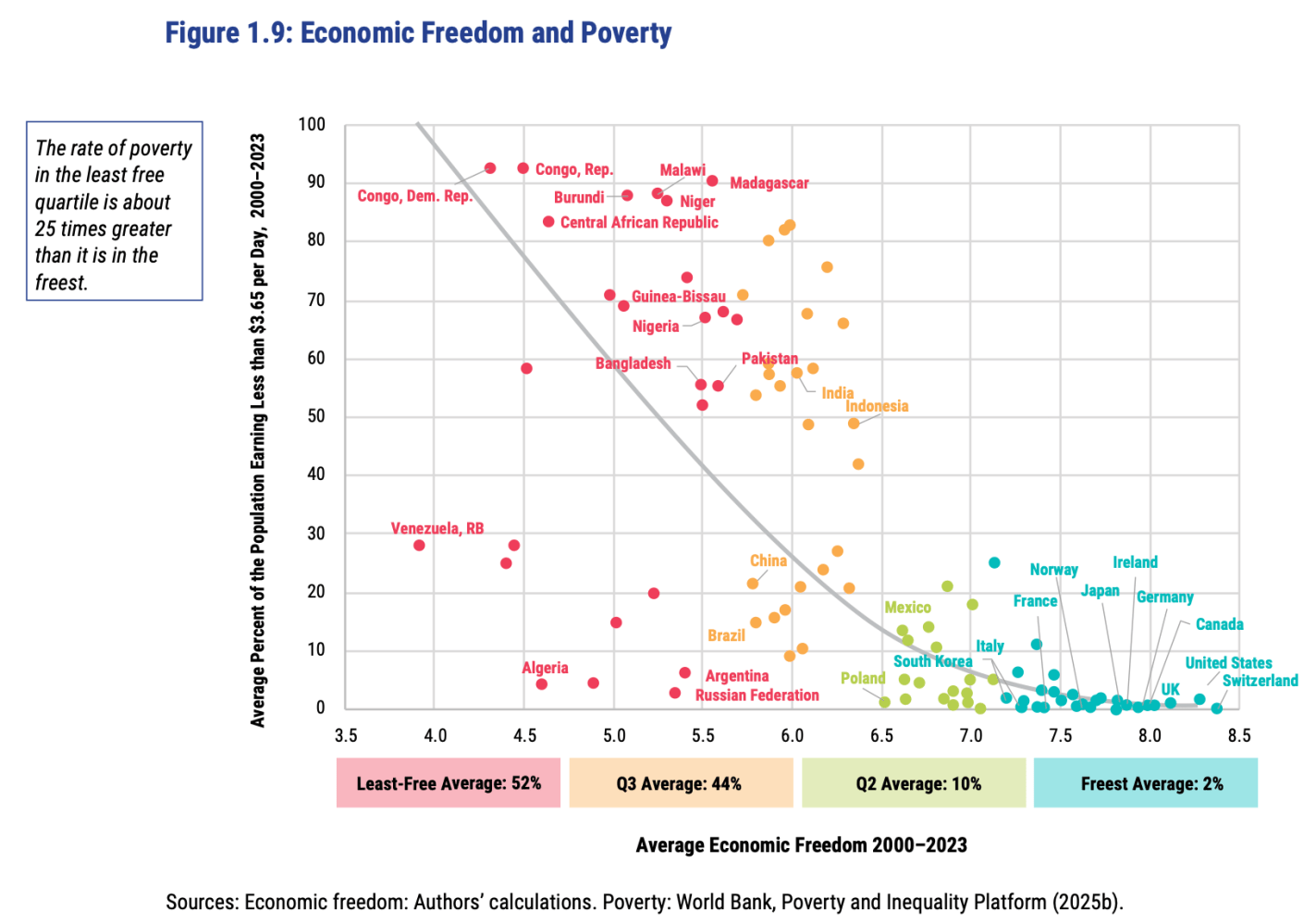

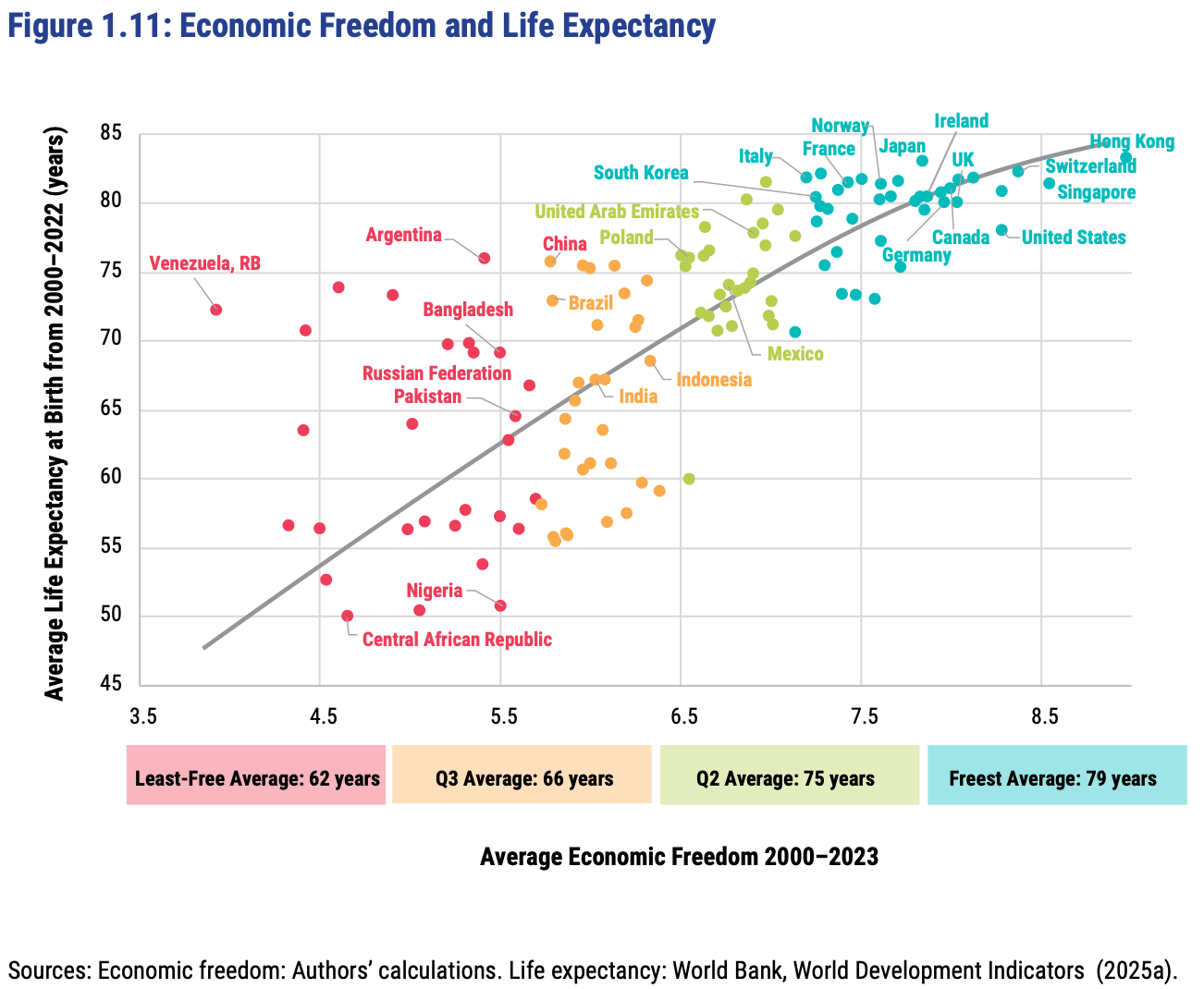

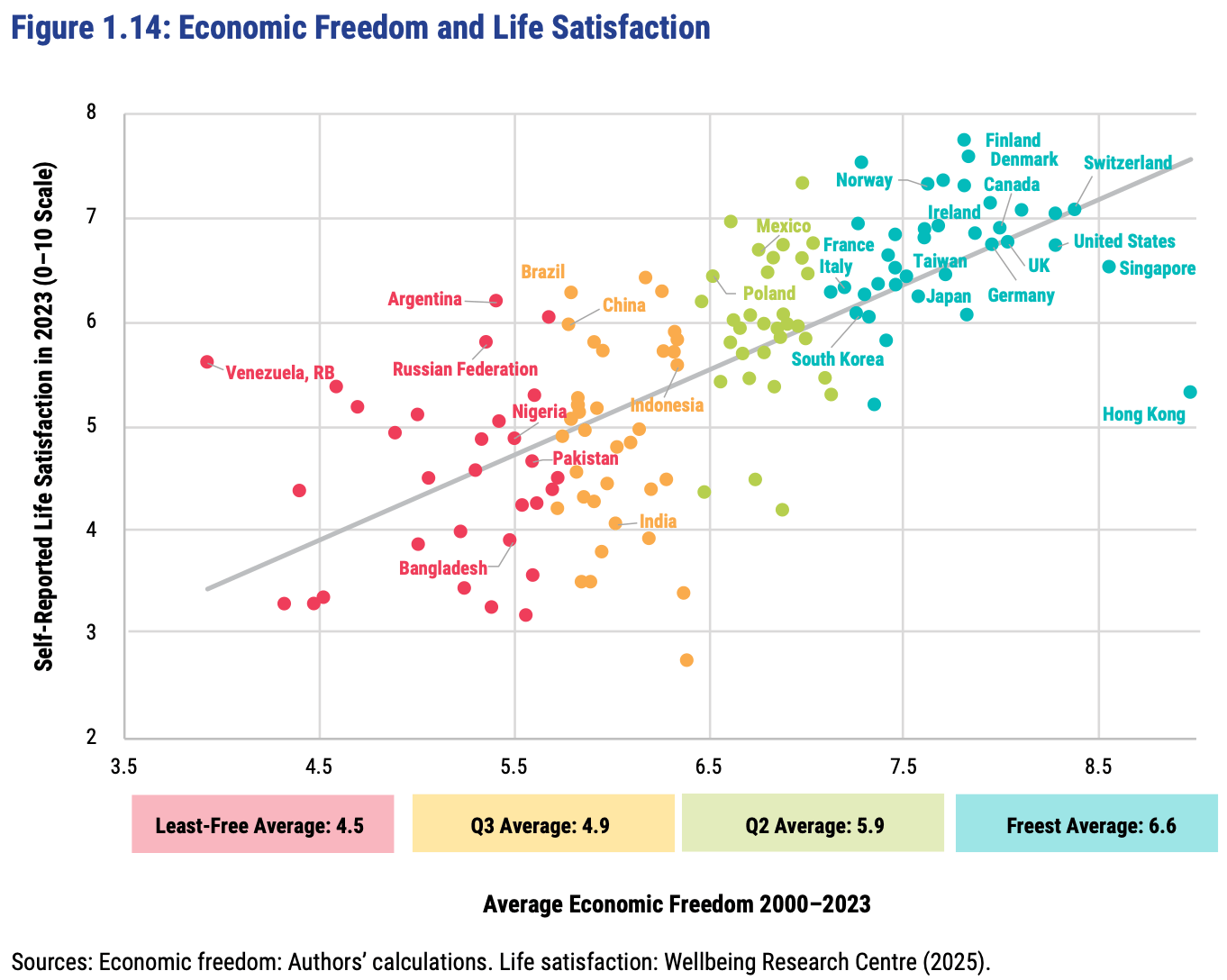

The Fraser Institute released their latest report on the Economic Freedom of the World today, measuring economic policy in all countries as of 2023. They made this excellent Rosling-style graphic that sums up their data along with why it matters:

In short: almost every country with high economic freedom gets rich, and every country that gets rich either has high economic freedom or tons of oil. This rising tide of prosperity lifts all boats:

This greater prosperity that comes with economic freedom goes well beyond “just having more stuff”:

The full report, along with the underlying data going back to 1970, is here. The authors are doing great work and releasing it for free, so no complaints, but two additional things I’d like to see from them are a graphic showing which countries had the biggest changes in economic freedom since last year, and links to the underlying program used to create the above graphs so that readers could hover over each dot to identify the country (I suppose an independent blogger could do the first thing as easily as they could…).

FRDM is an ETF that invests in emerging markets with high economic freedom (I hold some), I imagine they will be rebalancing following the new report.