But since then, we’ve got some better news. The chart below shows the data (note: I’m using wages for private production and non-supervisory workers here, rather than for all private workers in the May post).

While the overall inflation picture still looks bad, with 7.1% annual inflation in the latest report, we also see that in the past 5 months wage growth has exceeded CPI growth. It’s also been true compared with the PCE price index for the past 4 available months (November PCE data won’t be available until next Friday). Inflation has cooled slightly in the past few months, while wages have continued to grow.

This all means that real (inflation-adjusted) average wages in the US have been rising consistently since June 2022. Finally, some good news!

If you have spent any time on social media in the past week, you’ve probably noticed a lot of people using the new AI program called ChatGPT. Joy blogged about it recently too. It’s a fun thing to play with and often gives you very good (or at least interesting) responses to questions you ask. And it’s blown up on social media, probably because it’s free, responds instantly, and is easy to screenshot.

But as with all things AI, there are numerous concerns that come up, both theoretical and immediately real. One immediately real concern among academics is the possibility of cheating by students on homework, short writing assignments, or take-home exams. I don’t want to diminish these concerns, but I think for now they are overblown. Let me demonstrate by example.

This semester I am teaching an undergraduate course in Economic History. Two of the big topics we cover are the Industrial Revolution and the Great Depression. Specifically, we spend a lot of time discussing the various theories of the causes of these two events. On the exams, students are asked to, more or less, summarize these potential causes and discuss them.

How does ChatGPT do?

On the Industrial Revolution:

And on the Great Depression:

Now, it’s not that these answers are flat out wrong. The answers certainly list theories that have been discussed by at various times, including in the academic literature. But these answers just wouldn’t be very good for my class, primarily because they miss almost all of the theories that we have discussed in class as being likely causes. Moreover, the answers also list theories that we have discussed in class as probably not being correct.

These kinds of errors are especially true of the answer about the Great Depression, which reads like it was taken straight from a high school history textbook, ignoring almost everything economists have said about the topic. The answer for the Industrial Revolution doesn’t make this mistake as much as it misses most of the theories discussed by Koyama and Rubin, which was the main book we used to work through the literature. If a student gave an answer like the AI, it suggests to me that they didn’t even look at the chapter titles in K&R, which provide a roadmap of the main theories.

So, my message to students: don’t try to use this to answer questions in class, at least not right now. The program will certainly improve in the future, and perhaps it will eventually get very good at answering these kinds of academic questions.

But I also have a message to fellow academics: make sure that you are writing questions that aren’t easily answered by an AI. This can be hard to do, especially if you haven’t thought about it deeply, but ultimately thinking in this way should help you to write better exam and homework questions. This approach seems far superior to the one that the AI suggests.

Remember the “Fight for $15”? It’s a 10-year-old movement to raise the federal minimum wage to $15 per hour. While there hasn’t been any increase in the federal minimum wage since the movement began in 2012, plenty of states and localities have done so.

I won’t rehash the entire debate on the minimum wage here, but I will point you to this post from Joy on large minimum wage changes, and here are several other posts on this blog on the same topic. But lately I have seen an increasing call for even larger minimum wage increases, well beyond $15.

A prominent recent call for a higher wage comes from the SEIU, the second largest labor union in the nation. They are calling for a $25 minimum wage in Chicago, where the legal minimum wage just recently crossed $15 last year. Again, without getting into the detailed debates about the economics of the minimum wage, we can recognize that this would be a massively high minimum wage, given that median hourly wage for the Chicago MSA was $22.74 in May 2021. It’s certainly a bit higher in 2022, and the city of Chicago is probably a bit higher than the entire MSA. Still, we are talking about a minimum wage that would cover roughly half the workforce. Well, at least half the current workforce. The negative employment effects would potentially be large.

Here I will dabble a little bit in the minimum wage literature. One of the most famous recent papers that suggests increasing the minimum wage doesn’t have large negative employment effects is a 2019 paper by Cengiz, et al. This paper only looks at legal minimum wages that go up to 59% of the median market wage, which is the highest wages have been pushed up so far. By contrast, that $25 minimum wage in Chicago would be somewhere around 100% (!) of the local median market wage. That’s huge, and goes far beyond what even the most sympathetic-to-the-minimum-wage research has looked at.

But here’s the most recent minimum wage call that really takes the cake: over $40 per hour in Hawaii. That comes from, in a way, a Tweet from Hal Singer:

Working full time at the minimum wage won’t cover a two-bedroom rental in any state. So the Economist proposes expanding the housing supply. It can’t fathom raising the minimum wage to address homelessness. pic.twitter.com/8GFYyMynVm

Now in fairness, he doesn’t exactly call for a $40 minimum wage in Hawaii, but he does say we should use the minimum wage as a tool to address homelessness, and then points to a study showing that you would need to earn $40/hour in Hawaii to afford a two-bedroom apartment. That’s pretty close. The median wage in Hawaii? About $23 in May 2021. In fact, the 75th percentile wage in Hawaii was $36.50 in 2021! So, depending on exactly how much wage growth there has been in Hawaii since May 2021, we are likely talking about a $40 minimum wage covering 75% of the workforce! That would likely have some “bite,” as economists say.

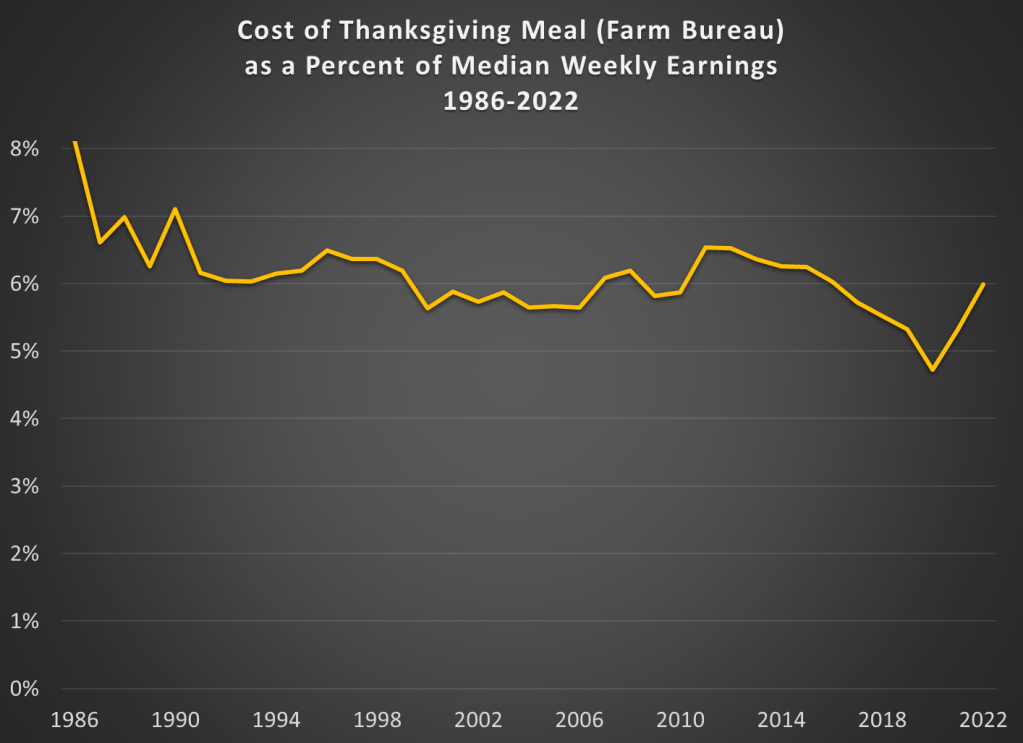

Last year inflation hadn’t quite hit the levels we would see in 2022, but they were already rising. When Thanksgiving rolled around, many media sources were reporting that it was the “most expensive Thanksgiving ever.” In nominal terms that was true, though in nominal terms it isn’t that surprising. In a post last year, I compared the prices of Thanksgiving dinners (using the same data from Farm Bureau) to median earnings going back to 1986. While 2021 was more expensive the 2020, it turned out it was still the second lowest it had been since 1986.

As you might expect, this year’s Thanksgiving dinner is even more expensive than last year in nominal terms. It’s up about 20% since last year or over $10 more, according to Farm Bureau. That’s certainly more than the overall rate of inflation (7.7% in the past 12 months) and more than inflation for groceries (12.4% in the past 12 months). But how does that compare with median wages? Comparing the 3rd quarter of this year with the same quarter in 2021, median wages are only up about 7%, certainly not enough to keep up with those rising turkey prices.

When we add 2022 to the historical chart, here’s what it looks like.

The spike in the last 2 years is clear in the chart but notice that at about 6% of median weekly earnings, we have essentially returned to the average level of the entire series. From 2017-2021, we could be thankful that the price of your Thanksgiving dinner had dropped below that 6% level. We’ll have to find something else to be thankful for this year.

In the United States and much of the developed world today, most roads are publicly provided, i.e., they are built and operated by governments. This is not exclusively true, as many private toll roads exist, but the vast majority of roads are owned and operated by governments. Must it be this way?

A recent working paper by Alan Rosevear, Dan Bogart, and Leigh Shaw-Taylor looks at a very important case study: Britain in the 19th century. Britain is important because they were the leading economy in the world at the time, at the forefront of the Industrial Revolution. How were roads built and improved in England and Wales at this time? Here’s what the authors have to say in the abstract:

“non-profit organizations, known as turnpike trusts, built more new roads by attracting private investors and capable surveyors. We also show the Government Mail Road had the highest quality. Nevertheless, most turnpike trust roads were good quality, indicating their practical achievements.”

In the conclusion of the paper, they further add:

“Our analysis demonstrates that turnpike trusts were responsible for building 4,000 miles of new, good quality road in England and Wales, much of it between 1810 and 1838. On a directly comparable basis, the not-for-profit trusts built thirty times the mileage than had been built with direct Government funding during the early 1800s.”

To be clear, this paper is not a completely new discovery. It was already well-known that private companies built roads in Britain, as the authors make clear in their literature review. Similarly, there were many private turnpikes and toll roads in the US in the 19th century, as summarized in an encyclopedia entry by Klein and Majewski.

The Rosevear et al. paper adds new important details. First, they document the extent of private road building and improvements in the 19th century. Second, they show that these roads were generally of good quality, or at least they were of good quality for the time. Prior research had not documented these facts, thus making this a very important advance in our understanding of this time period. But perhaps more importantly, we see the possibility that many more roads today could be privately built and funded with user fee, especially considering that we are much, much wealthier today than 19th century Britain, we have more extensive and functional capital markets for raising the funds, etc.

The all-cause mortality rate in 2021 for men in the US ages 18-39 was about 40% higher than the average of 2018 and 2019. That’s a huge increase, especially for a group that is not in the high-risk category for COVID-19. What’s causing it?

Some have suggested that heart disease deaths, perhaps induced by the COVID vaccines, is the cause. This is not just a fringe internet theory by anonymous Twitter accounts. The Surgeon General of Florida has said this is true.

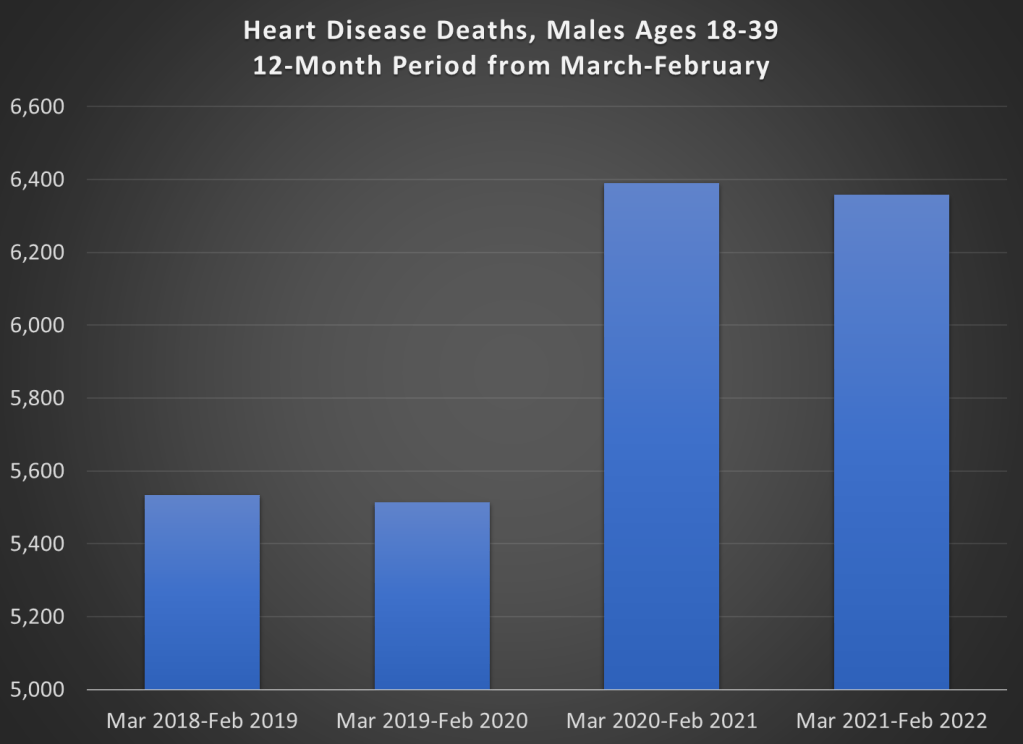

What do the data say? The first thing we can look at is heart disease deaths for men ages 18-39.

The data I’m using is from the CDC WONDER database. This database aggregates data from US states, using a standardized system of reporting deaths. The most important thing to know is that in this database, each death can one have one underlying cause, and this is indicated on the death certificate. Deaths can also have multiple contributing causes (and most deaths do), and the database allows you to search for those too. But for this analysis, I’m only looking at the underlying cause.

Here’s the heart disease death data for men ages 18-39, presented two different ways. First the trailing 12-month average. Don’t focus too much on that dip at the end, since the most recent data is incomplete. Instead, notice three things. First, there was a clear increase in heart disease deaths. Second, that rise began in mid-2020, well before the introduction of vaccines. Third, once vaccines started being administered to this age group in Spring 2021, the number of deaths leveled off (though it didn’t return to pre-pandemic levels).

Here’s another way of looking at the data: 12-month time periods, rather than a trailing average. I created 12-month time periods starting in March and ending in February of the following year. I’ve also truncated the y-axis to show more detail, not to trick you. But don’t be tricked! The deaths are up 2-3%, not a more than doubling as the chart appears to show.

We can see in the chart above that the rise in heart disease deaths for young males completely preceded the vaccination period. Something changed, for sure, but the change wasn’t the introduction of vaccines. Heart disease deaths (by underlying cause) are only up 2-3%, while overall deaths are up around 40%.

So, to repeat the title question, what is killing these young men?

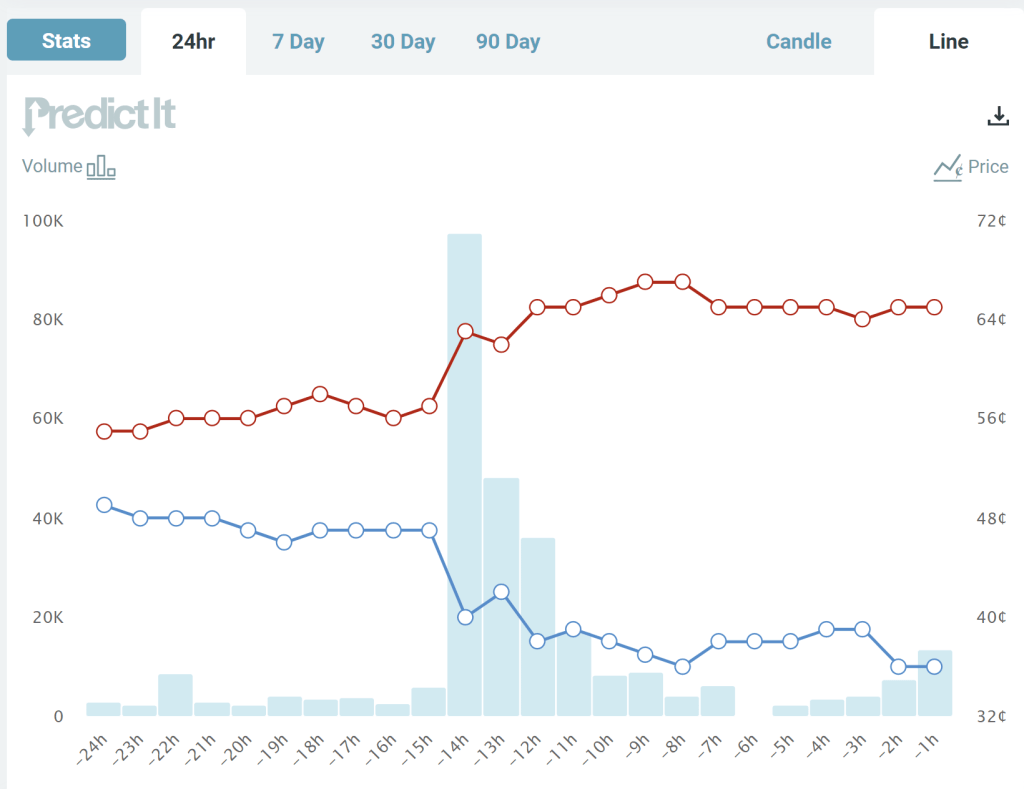

Last night the major party candidates for Senate in Pennsylvania had their first and only debate. I didn’t watch it, since I don’t live in Pennsylvania. But judging by my Twitter feed, a lot of people did watch it, including (bizarrely to me) lots of people who don’t live in Pennsylvania. And overnight, tons of articles were written analyzing the debate, saying who “won” the debate, and so on (“5 Things You Need to Know About the Pennsylvania Senate Debate” etc.).

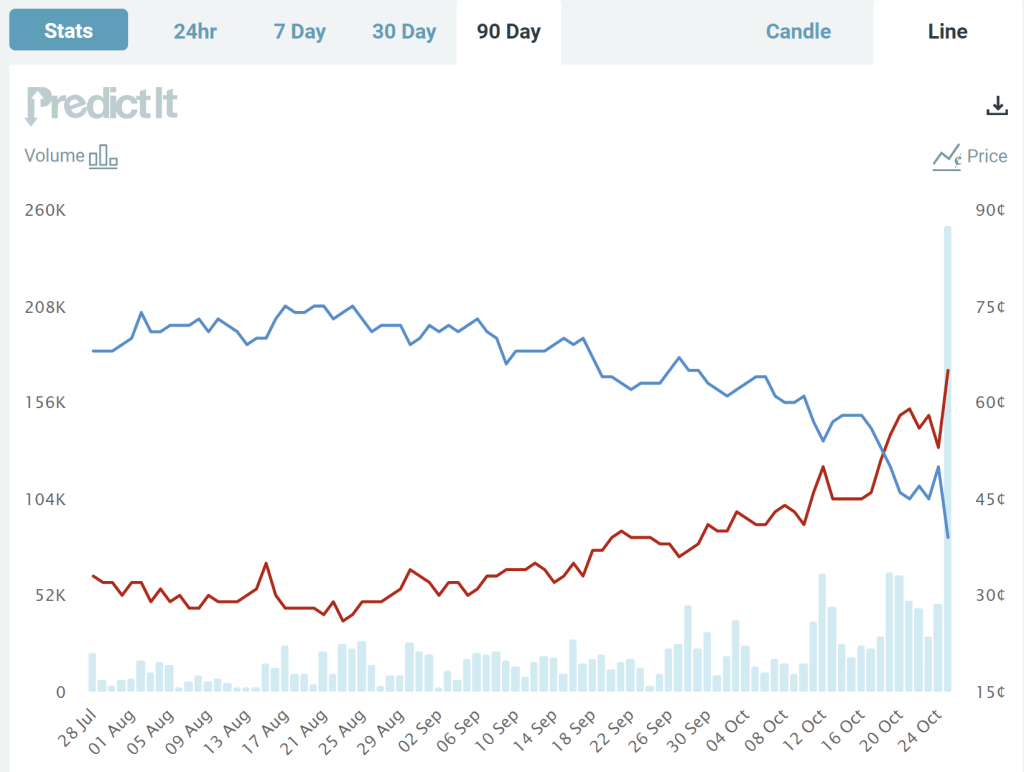

But this blog post is the only thing you need to read about that debate. And these charts are really all you need to look at.

These two charts come from the prediction market website PredictIt. The charts show the “odds” (more on that below) that each candidate will win the Pennsylvania Senate race, over a 90-day time horizon (first chart) and the last 24 hours (second chart). What do we see? The Democratic candidate has been leading for the entire race up until a week ago, though with his odds falling gradually over the past month or two.

Notice though the big jump last night during the debate. The Republican candidate moved up from odds of about 57% to odds of about 63%, close to where it stands as I write (67%). Based on this result, it’s safe to say that the Republican candidate “won” the debate, though not so decisively that the election is now a foregone conclusion. You don’t need to wait for the polls, which have consistently showed the Democratic candidate in the lead (though with the gap closing in recent weeks) — though of course, these betting odds could change as new polling data is released.

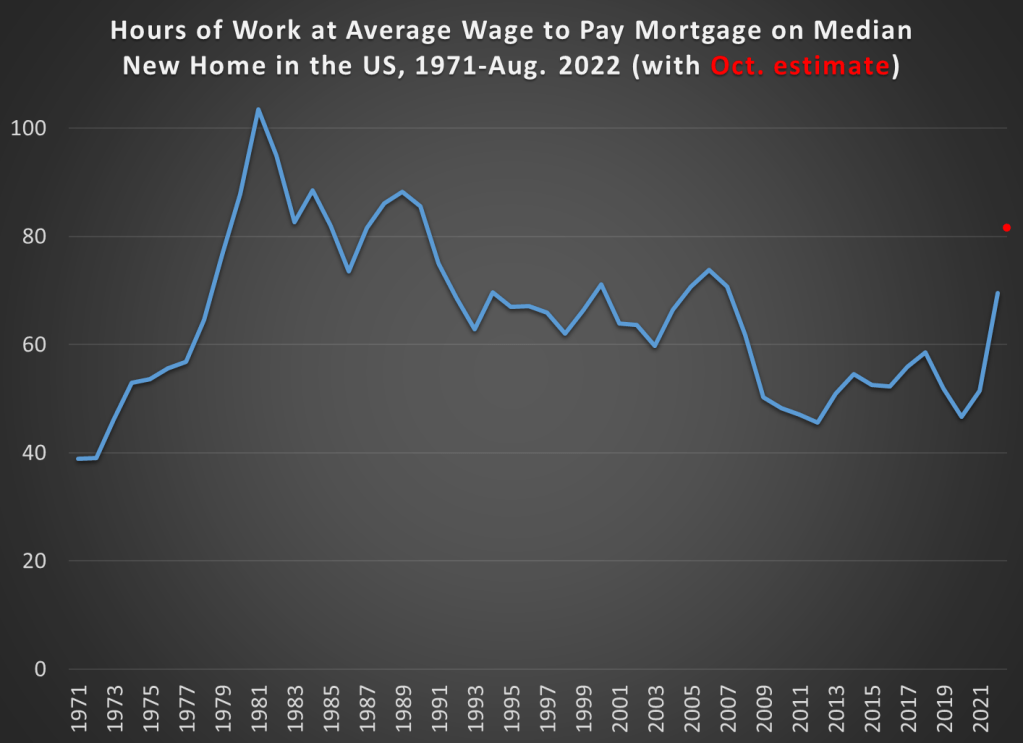

Mortgage interest rates are climbing quickly, while housing prices are still mostly high. These factors combined means that it is much more expensive to buy a home than in the recent past. But how much more expensive? And how does this compare with the past 50 years of history?

The chart below is my attempt to answer those questions. It shows the number of hours you would need to work at the average wage to make a mortgage payment (principal and interest) on the median new home in the US.

My goal here was to provide the most up-to-date estimate of this number consistent with the historical data. Thus, I had to use average wage data rather than median wage data, since the median hourly wage data is not available for 2022 yet. But as I’ve discussed before, while median and average wages are different, their rate of increase is roughly the same year-to-year, so it would show the same trends.

The final point plotted on the blue line in the chart is for August 2022, the last month for which we have median home price data, average wage data, and 30-year mortgage rates. Mortgage rates are the yearly average (or monthly average in the case of August 2022).

You’ll also notice a red dot at the very end of the series. This is my guess of where the line will be in October 2022, once we have complete data for these three variables (right now only mortgage rates are available in October for the three series I am using). I’m doing my best here to provide as much of a real-time picture as possible, given that rates are rising very sharply right now, while still providing consistent historical comparisons. If that estimate is roughly correct, mortgage costs on new homes are now less affordable than any year since 1990.

The Mont Pelerin Society was founded 75 years ago. The title of this post was the opening sentence of the Statement of Aims the new Society agreed upon. They had many concerns about what they considered “central values,” but primary among those concerns were the dangers related to market economies: “a decline of belief in private property and the competitive market” and “the growth of theories which question the desirability of the rule of law.”

How has the world done since 1947? It’s easy to point to the decline of communism and socialism, both in practice and as a dominant theory, as a victory for the goals of the Mont Pelerin Society. However, we might be concerned that in the non-communist world, economic freedom has declined even as communism has failed. Let’s dig a little deeper.

One source we can use is an extension of the Fraser Institute’s Economic Freedom of the World index. The primary index only extends back to 1970, but recently Lawson and Murphy have constructed a version of the index which goes all the way back to 1950 for some countries. As far as I’m aware, they haven’t yet perfectly mapped the pre-1970 index with the primary index that extends to the present, but I’ll make a quick comparison using the available data. The 1950 data brings us very close to the date of the first MPS meeting.

Here’s a list of countries relevant to the discussion at MPS in 1947. The list includes countries where attendees came from, as well as other countries of interest to the discussion, such as China and Russia (I’m using the list from Caldwell’s recent edited transcripts of the 1947 meeting). Caveat: this isn’t a chain-linked index, so the 1950 and 2020 numbers are perfectly comparable. Also, the 2020 number only includes Areas 1-4 of the index, since that’s what the pre-1970 data contains.

The table above should give us some optimism about the state of market economies in the world from the perspective of 1947. Not only have China and Russia, clearly improved their economic freedom scores, but all of the Western market economies have as well. Again, exercise caution in interpreting these, since it’s not a chain-linked index, and it excludes one area of economic freedom (regulation, which surely has grown substantially since 1947). Despite those cautions, the picture in 2020 looks pretty good compared with 1950.

But what of other liberal institutions? While the MPS statement of aims doesn’t specifically mention democratic institutions, the threat to democracy seems to clearly be a concern in 1947 (“extensions of arbitrary power” and “freedom of thought and expression”).