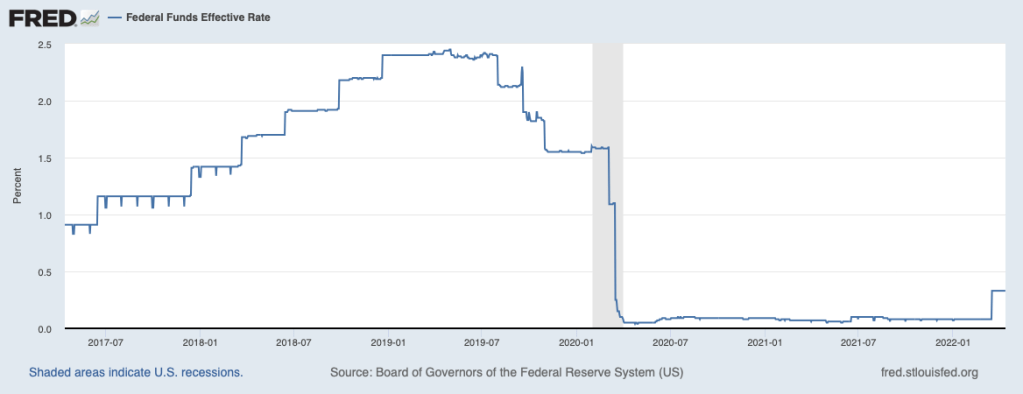

In March the Federal Reserve raised rates for the first time since Covid began:

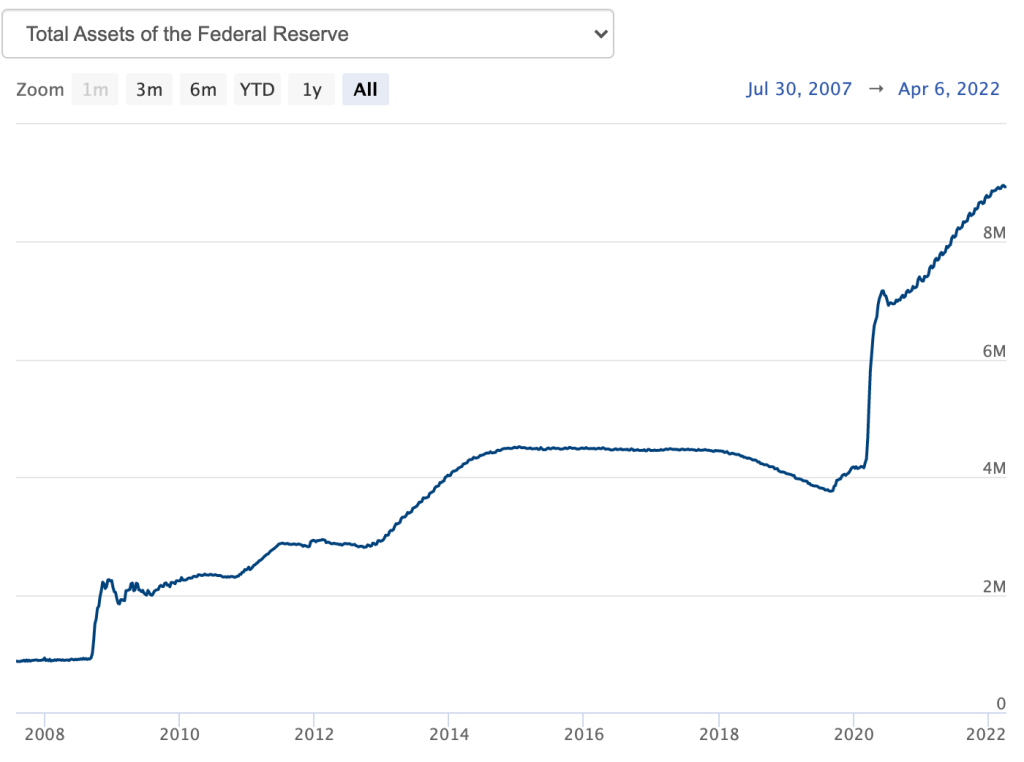

They also began to shrink their balance sheet:

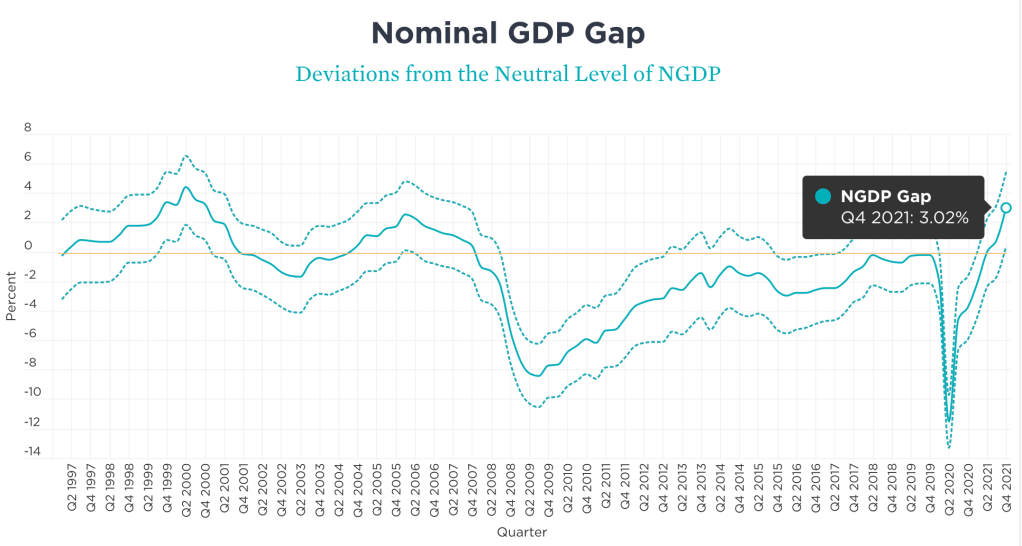

These moves are in the right direction, but represent a slow start to tackling inflation that is the highest of my lifetime, with the CPI up 8.5% over the last year. While temporary supply constraints are contributing to this, it seems clear to me that excessive aggregate demand is a major driver of this inflation. The labor market has already recovered, with unemployment at 3.6% like it was in late 2019. The Covid-induced output gap is fully eliminated by one standard measure:

But market-based measures of inflation expectations remain high. The TIPS spread predicts that inflation rates over the next 10 years will be much closer to 3% than to the Fed’s target of 2%:

My preferred measure, the NGDP gap, is at 3% (i.e., 3% over the ideal level of 0)

Overall, its seams clear that Fed policy is currently too loose. The harder question is, what exactly to do about it? How much should they raise rates? The simplest way to answer this is to use the Taylor Rule. Using the version of the rule that Bernanke describes here and using core PCE as the inflation measure (currently just 5.4% yoy, vs 8.5% for headline CPI) implies that the Fed Funds rate should be:

5.4% + 0.5*0% + 0.5*(5.4%-2) + 2 = 9.1%

As Bernanke and many others have explained, you don’t want to take the Taylor rule literally, and the Fed raising rates to 9.1% Volcker-style at their next meeting would be a terrible idea. But keeping the Fed Funds rate under 0.5% would also be a terrible idea. Markets do expect the Fed to keep raising rates this year, but slowly, so that they would be around 2.25% by December. I’ll go on record as worrying that this is too slow, and recommending that they raise rates by at least 0.5% at their next meeting, and continue doing so until market-based measures of medium-run inflation are down to 2%.

Disclaimer: I’m a microeconomist whose last post on inflation was at best only directionally right. Consider this the view of one “insider-outsider” and then go read smarter people like Scott Sumner.