Most US states require hospitals and other healthcare providers to obtain a “Certificate of Need” (CON) from a state board before they are allowed to open or expand. These laws seem to be one reason why healthcare is often so expensive and hard to find. I’ve written a lot about them, partly because I think they are bad policies that could get repealed if more people knew about them, and partly because so many aspects of them are unstudied.

States vary widely in the specific services or equipment their CON laws target- nursing homes, dialysis clinics, MRIs, et c. One of the most important types of CON law that remained unstudied was CON for psychiatric services. I set out to change this and, with Eleanor Lewin, wrote an article on them just published in the Journal of Mental Health Policy and Economics.

We compare the state of psychiatric care in states with and without CON, and find that psychiatric CON is associated with fewer psychiatric hospitals and beds, and a lower likelihood of those hospitals accepting Medicare.

Together with the existing evidence on CON (which I tried to sum up recently here), this suggests that more states should consider repealing their CON laws and letting doctors and patients, rather than state boards, decide what facilities are “economically necessary”.

According to the most recent TSA data, on December 21st of this year there were 1,979,089 people traveling by plane. That’s almost exactly equal to the number of people that flew in the US on the same date in 2019: 1,981,433 travelers. It’s also double the number of people that few on December 21, 2020 (about 992,000). These numbers are encouraging. Does that mean that we’re back to normal levels of travel?

Not quite. We shouldn’t read too much into one day of data, for a variety of reasons, but most importantly because while we’re looking at the same date, travel varies throughout the week and December 21st is a different day of the week every year (Tuesday this year, Saturday in 2019). It’s better to use a weekly average and compare it to 2019. Here’s what the data looks like for 2020 and 2021.

With this data, we can see that airline travel is back to about 85 percent of 2019 levels. That’s not bad, but airline travel was already back to 85 percent by early July 2021, with some variation since then, but generally staying in the 70-90 percent range for most of the second half of the year.

For those that are flying this year, there is good news in terms of prices (unusual to have good prices news right now): airfares are still about 20 percent cheaper than pre-pandemic levels. In fact, airline prices are the cheapest they have been since 1999. In nominal terms! If you are interested in even more historical price data, take a look at my May 2021 post on the “golden age” of flight.

And of course, flying is not the most common way that people travel for Christmas and the holiday season. According to estimates from AAA, only about 6 percent of holiday travelers choose to fly. This was true in 2019, and will be roughly true in 2021 (as usual, 2020 was the exception: around 3 percent). By far the most common mode of travel in the US is driving, accounting for over 90 percent of holiday travel.

If you are traveling by car, there isn’t much good news for prices. As you have no doubt heard constantly for the past few months, gasoline costs a lot more than it did last Christmas, on average about $1 per gallon more. But even compared to Christmas 2019, gasoline prices are almost 29 percent higher. The last time gasoline prices were this high (in nominal terms) around Christmas was in 2013.

I hope you all have safe holiday travels, and we’ll all look forward to better prices in the New Year!

I remember people talking about Covid-19 in January of 2020. There had been several epidemic scare-claims from major news outlets in the decade prior and those all turned out to be nothing. So, I was not excited about this one. By the end of the month, I saw people making substantiated claims and I started to suspect that my low-information heuristic might not perform well.

People are different. We have different degrees of excitability, different risk tolerances, and different biases. At the start of the pandemic, these differences were on full display between political figures and their parties, and among the state and municipal governments. There were a lot of divergent beliefs about the world. Depending on your news outlet of choice, you probably think that some politicians and bureaucrats acted with either malice or incompetence.

I think that the Federal Reserve did a fine job, however. What follows is an abridged timeline, graph by graph, of how and when the Fed managed monetary policy during the Covid-19 pandemic.

February, 2020: Financial Markets recognize a big problem

The S&P begins its rapid decent on February 20th and would ultimately lose a third of its value by March 23rd. Financial markets are often easily scared, however. The primary tool that the Fed has is adjusting the number of reserves and the available money supply by purchasing various assets. The Fed didn’t begin buying extra assets of any kind until mid-March. There is a clear response by the 18th, though they may have started making a change by the 11th. One might argue that they cut the federal funds rate as early as the 4th, but given that there was no change in their balance sheet, this was probably demand driven.

March, 2020: The Fed Accommodates quickly and substantially.

In the month following March 9th, the Fed increased M2 by 8.3%. By the week of March 21st, consumer sentiment and mobility was down and economic policy uncertainty began to rise substantially – people freaked out. Although the consumer sentiment weekly indicator was back within the range of normal by the end of April, EPU remained elevated through May of 2020. Additionally, although lending was only slightly down, bank reserves increased 71% from February to April. Much of that was due to Fed asset purchases. But there was also a healthy chunk that was due to consumer spending tanking by 20% over the same period.

In the 18 months prior to 2020, M2 had grown at rate of about 0.5% per month. For the almost 18 months following the sudden 8.3% increase, the new growth rate of M2 almost doubled to about 1% per month. The Fed accommodated quite quickly in March.

April, 2020: People are awash with money

Falling consumption caused bank deposit balances to rise by 5.6% between March 11th and April 8th. The first round of stimulus checks were deposited during the weekend of April 11th. That contributed to bank deposits rising by another 6.7% by May 13th.

By the end of March, three weeks after it began increasing M2, the Fed remembered that it really didn’t want another housing crisis. It didn’t want another round of fire sales, bank failures, disintermediation, collapsed lending, and debt deflation. It went from owning $0 in mortgage-backed securities (MBS) on March 25th to owning nearly $1.5 billion worth by the week of April 1st. Nobody’s talking about it, but the Fed kept buying MBS at a constant growth rate through 2021.

May, 2020 – December, 2021: The Fed Prevents Last-Time’s Crisis

Jerome Powell presided over the shortest US recession ever on record. The Fed helped to successfully avoid a housing collapse, disintermediation, and debt deflation – by 2008 standards. The monthly supply of housing collapsed, but it had bottomed out by the end of the summer. By August of 2021, the supply of housing had entirely recovered. The average price of new house sales never fell. Prices in April of 2020 were typical of the year prior, then rose thereafter. A broader measure of success was that total loans did not fall sharply and are nearly back to their pre-pandemic volumes. After 2008, it took six years to again reach the prior peak. A broader measure still, total spending in the US economy is back to the level predicted by the pre-pandemic trend.

The Fed can’t control long-run output. As I’ve written previously, insofar as aggregate demand management is concerned, we are perfectly on track. The problem in the US economy now is real output. The Fed avoided debt deflation, but it can’t control the real responses in production, supply chains, and labor markets that were disrupted by Covid-19 and the associated policy responses.

What was the cost of the Fed’s apparent success? Some have argued that the Fed has lost some of its political insulation and that it unnecessarily and imprudently over-reached into non-monetary areas. Maybe future Fed responses will depend on who is in office or will depend on which group of favored interests need help. Personally, I’m not so worried about political exposure. But I am quite worried about the Fed’s interventions in particular markets, such as MBS, and how/whether they will divest responsibly.

Of course, another cost of the Fed’s policies has been higher inflation. During the 17 months prior to the pandemic, inflation was 0.125% per month. During the pandemic recession, consumer prices dipped and inflation was moderate through November. But, in the 16 months since April of 2020, consumer prices have grown at a rate of 0.393% per month – more than three times the previous rate. Some of that is catch-up after the brief fall in prices.

Although people are genuinely worried about inflation, they were also worried about if after the 2008 recession and it never came. This time, inflation is actually elevated. But people were complaining about inflation before it was ever perceptible. The compound annual rate of inflation rose to 7% in March of 2021. But it had been almost zero as recent as November, 2020. That March 2021 number is misleading. The actual change in prices from February to March was 0.567%. Something that was priced at $10 in February was then priced at $10.06 in March. Hardly noticeable, were it not for headlines and news feeds.

The panel on the proposed merger of Rhode Islands two largest hospital systems I mentioned last week happened yesterday, I’ll post some reactions here, there was a lot I didn’t get to say since my section only had 45 minutes split across 4 panelists and Senator Whitehouse naturally got more of the time.

The Lifespan and Care New England CEOs trying to merge their systems opened with what to me seemed like their weakest argument, a general appeal to togetherness. They said that if the Patriots offense and defense had to be kept as separate teams, they wouldn’t be very good. To me the right metaphor is that if you merged all the NFL teams into one super team, they wouldn’t try very hard.

To their credit though, overall the hospital CEOs and President Paxson of Brown University were surprisingly honest about the risks, basically acknowledging that hospital mergers are often just a way to gain market power at everyone else’s expense, but arguing that for various reasons this one is different. They seem to realize that if you define the relevant market area as the state of Rhode Island (as e.g. the Dartmouth Atlas does in their “Hospital Referral Regions”) then the merged entity would have a nearly 80% market share and be challenged by the FTC as an obvious monopoly. So they argue that the relevant market should include Boston and much of Connecticut. They argue that it won’t just be an excuse to raise prices because they are non-profits and the state has rate regulations.

They identified two potential true efficiencies, integrating the electronic medical records of the two systems and being able to easily conduct research across both systems (both systems have many employees who are faculty at Brown Med School, including my wife). In a reasonable world these efficiencies could be gained without merging, though I suspect HIPAA prevents this, meaning one of its many perverse unintended consequences would be incentivizing mergers.

Their biggest admission against interest was that “the primary benefit [of the merger] comes from scale” and that “scale matters for purchasing supplies and staffing”. To me this implies “don’t worry, we won’t use our monopoly power against consumers, we’ll just use it against suppliers and staff”. But the FTC just repealed their consumer welfare standard, and so I think these statements could come back to haunt the merging parties.

According to the Johns Hopkins COVID tracker, the US has now surpassed 800,000 COVID deaths during the pandemic. The CDC COVID tracker is almost to 800,000 too. But is this number right? Confusion about COVID deaths and total deaths has been rampant throughout the pandemic, especially when comparing across countries.

One method that many have suggested is excess deaths, which is generally defined as the number of deaths in a country above-and-beyond what we would expect given pre-pandemic mortality levels. It’s a very rough attempt at creating a counterfactual of what mortality would have looked like without the pandemic. Of course, you can never know for sure what the counterfactual would look like. Would overdoses in the US have increased anyway? Hard to say, though they had been on the rise for years even before the pandemic.

So don’t treat excess deaths as a true counterfactual, but just a very rough estimate. I wrote about excess deaths in the US way back in January 2021 (feels like a lifetime ago!), and at the time for 2020 it looked like the US had about 3 million total deaths (in the first 48 weeks of 2020), which was about 357,000 deaths more than expected (again, based on historical levels of the past few years), or about 13.6% above normal.

But once we had complete data for 2020, deaths were even higher: about 19% above expected, or somewhere around 500,000 excess deaths. This compares with the official COVID death count of about 385,000 in 2020 for the US.

What happens if we update those numbers with the most recent available mortality data for 2021? Keep in mind that data reporting is always delayed, so I’ll just use data through October 2021. The following chart shows both confirmed COVID deaths and total excess mortality, cumulative since the beginning of 2020.

As we can see in the chart, there are a lot more excess deaths than confirmed COVID deaths. There were already over 1 million excess deaths through the end of October 2021 in the US, cumulative since January 2020. This compares with about 766,000 confirmed COVID deaths. That’s a big gap!

We could spend a lot of time trying to understand this gap of 250,000 deaths. Is this under-reporting of COVID deaths? Is it deaths caused by government restrictions? Is it caused by the overwhelming of the health system?

I won’t be able to answer any of those questions today. Instead, let’s ask a different question: is the potential US undercount of COVID deaths unusual?

One reason for opening an account where you can purchase cryptocurrencies is to speculate on their price movements. There have been many cases where some coin has quadrupled in a few weeks, or gone up ten-fold in a few months, or even a hundred-fold within a year.

Another facet of crypto accounts is that in some cases you are paid interest on the coin you have purchased and hold in your account. That was the main draw for me. I already have a little Bitcoin and Ethereum exposure in my brokerage account through the funds GBTC and ETHE, enough to feel the thrill of victory and the agony of defeat when they go up, up, up and down, down, down, but I am not a big speculator at heart. So, I am drawn to the so-called “stablecoins”, whose value is tied to some major regular currency such as the U.S. dollar. It turns out that you can get high, steady interest payments on those stablecoins.

There are several crypto brokers which pay interest on coins. Some names include BlockFi, Celsius, Nexo, and Voyager Digital. Several such firms are reviewed here. Initially I leaned towards Voyager, since it gives access to lots of the new, little alt-coins where you can 10X your money if you pick the right ones and jump in early. However, I still do my own taxes, and the tax reporting from Voyager looked daunting. Last I looked, they just provide a dump of all your transactions in a giant table, and it’s up to you to figure out capital gains/losses. The word on the street is that this is not as straightforward as it seems. Also, Voyager offered only mobile apps, not a desktop interface. All in all, Voyager seems more geared towards intense younger Robin Hood/Reddit crowd, punching daring trades into their phones at all hours.

BlockFi is quite staid by comparison. It only offers a few, mainstream coins. However, it is one of the best-established firms, and it provides a nice clear 1099 tax reporting form at the end of the year. BlockFi is backed by major institutional partners, and manages over $9 billion in assets.

Unlike some of its competitors, it is U.S.-based, and as such it is structured to function well in this jurisdiction. Also, its interest payouts are straightforward. In contrast, many of its competitors incentivize you to receive your interest in special tokens issued by those companies, which adds another element of risk. Finally, BlockFi allows you to immediately transfer money in and out of your account by using a bank ACH link. I wanted that flexibility since I plan to keep a portion of my cash holdings in BlockFi instead of in the bank, but I want to be able to access those cash holdings on short notice and without penalty. (Last week I described some of my struggles over using the Plaid financial app which manages the bank-BlockFi interface, but I was able to get past that).

All in all, BlockFi is boring in a good way. All I want to do is make steady money, with minimal distraction. Here is a listing of the interest rates paid for holdings of Bitcoin and Ethereum:

BlockFi only pays significant interest for smaller holdings of these coins. (We will discuss the reason for this seemingly odd policy in a future blog post; it is basically an outcome of BlockFi’s conservative financial practices).

For Bitcoin, the interest rate is 4.5% for up to 0.10 BTC, which at today’s prices is about $4,700. After that, the interest plummets to 1%, and to a mere 0.10% for more than 0.35 BTC (about $16,000). There is a similar pattern for Ethereum. If your goal is to hold large amounts of these coins and earn substantial interest on them, there are probably better platforms than BlockFi.

However, the interest picture is brighter for the stablecoins. The biggest U.S.-based stablecoin is USD Coin (USDC), which is backed by significant institutions. Gemini Dollar (GUSD) is smaller, but also takes great pains to garner trust. Its issuer, Gemini, operates under the regulatory oversight of the New York State Department of Financial Services (NYDFS). It boasts, “The Gemini Dollar is fully backed at a one-to-one ratio with the U.S. dollar. The number of Gemini dollar tokens in circulation is equal to the number of U.S. dollars held at a bank in the United States, and the system is insured with pass-through FDIC deposit insurance as a preventative measure against money laundering, theft, and other illicit activities.” GUSD is the “native” currency within BlockFi, though users can easily exchange it for other coins. At this point I am holding just GUSD, though if I put in more funds, I would plan to partially diversify into USDC. Besides being much bigger, USDC now runs on multiple platforms, whereas GUSD is limited to Ethereum; if Ethereum finally does switch from proof-of-work to proof-of-stake, it may be more subject to outages or hacking, so it would be nice to not be totally dependent on Ethereum.

For these two stablecoins, BlockFi currently pays 9% interest on holdings up to $40,000, and a respectable 8% on larger holdings:

A complete list of BlockFi interest rates (which change from time to time) is here.

The alert reader may at this point object, “Hey, you are losing most of the purported benefits of blockchain cryptocurrencies – – without holding the coins in your own wallet, you don’t actually own them, so you are back dependent on The System. Moreover, those stablecoins are centrally managed, not deliberately decentralized like Bitcoin and Ethereum. You are treating this like a plain bank account!”

My reply is, “Yes, I am treating it like a plain bank account – – but an account that pays me 9% interest, with no drama.” That is exactly what I wanted.

UPDATE MARCH 2022 – – BLOCKFI INTEREST ACCOUNT NO LONGER AVAILABLE. For some time now, state and federal government authorities have been hassling crypto exchanges that offer interest on crypto holdings. In February, the SEC fined BlockFi $100 million for allegedly violating securities laws, and shut them down from taking in any new funds for interest-bearing accounts. BlockFi hopes someday to provide a regulation-compliant interest product, but don’t hold your breath.

Zealous state and federal regulators have been attacking other crypto firms offering interest, such as Celsius and Voyager. The main player still standing that I am aware of is Gemini. Gemini is very conscientious about audits and has always tried to work closely with regulators. It is offering about 6.5% interest on stablecoins (which is still way better than money markets or CDs), and a measly 1-1.25% on Bitcoin and Ethereum.

Opinions on game theory differ. To most of the public, it’s probably behind a shroud of mystery. To another set of the specialists, it is a natural offshoot of economics. And, finally a 3rd non-exclusive set find it silly and largely useless for real-world applications.

Regardless of the camp to which you claim membership, the Pure Strategy Nash Equilibrium (PSNE) is often misunderstood by students. In short, the PSNE is the set of all player strategy combinations that would cause no player to want to engage in a different strategy. In lay terms, it’s the list of possible choices people can make and find no benefit to changing their mind.

In class, I emphasize to my students that a Nash Equilibrium assumes that a player can control only their own actions and not those of the other players. It takes the opposing player strategies as ‘given’.

This seems simple enough. But students often implicitly suppose that a PSNE does more legwork than it can do. Below is an example of an extensive form game that illustrates a common point of student confusion. There are 2 players who play sequentially. The meaning of the letters is unimportant. If it helps, imagine that you’re playing Mortal Kombat and that Player 1 can jump or crouch. Depending on which he chooses, Player 2 will choose uppercut, block, approach, or distance. Each of the numbers that are listed at the bottom reflect the payoffs for each player that occur with each strategy combination.

Again, a PSNE is any combination of player strategies from which no player wants to deviate, given the strategies of the other players.

Students will often proceed with the following logic:

Player 2 would choose B over U because 3>2.

Player 2 would choose A over D because 4>1.

Player 1 is faced with earning 4 if he chooses J and 3 if he chooses C. So, the PSNE is that player 1 would choose J.

Therefore, the PSNE set of strategies is (J,B).

While students are entirely reasonable in their thinking, what they are doing is not finding a PSNE. First of all, (J,B) doesn’t include all of the possible strategies – it omits the entire right side of the game. How can Player 1 know whether he should change his mind if he doesn’t know what Player 2 is doing? Bottom line: A PSNE requires that *all* strategy combinations are listed.

The mistaken student says ‘Fine’ and writes that the PSNE strategies are (J, BA) and that the payoff is (4,3)*. And it is true that they have found a PSNE. When asked why, they’ll often reiterate their logic that I enumerate above. But, their answer is woefully incomplete. In the logic above, they only identify what Player 2 would choose on the right side of the tree when Player 1 chose C. They entirely neglected whether Player 2 would be willing to choose A or D when Player 1 chooses J. Yes, it is true that neither Player 1 nor Player 2 wants to deviate from (J, BA). But it is also true that neither player wants to deviate from (J, BD). In either case the payoff is (4, 3).

This is where students get upset. “Why would Player 2 be willing to choose D?! That’s irrational. They’d never do that!” But the student is mistaken. Player 2 is willing to choose D – just not when Player 1 chooses C. In other words, Player 2 is indifferent to A or D so long as Player 1 chooses J. In order for each player to decide whether they’d want to deviate strategies given what the other player is doing, we need to identify what the other player is doing! The bottom line: A PSNE requires that neither player wants to deviate given what the other player is doing – Not what the other player would do if one did choose to deviate.

What about when Player 1 chooses C? Then, Player 2 would choose A because 4 is a better payoff than 1. Player 2 doesn’t care whether he chooses U or B because (C, UA) and (C, BA) both provide him the same payoff of 4. We might be tempted to believe that both are PSNE. But they’re not! It’s correct that Player 2 wouldn’t deviate from (C, BA) to become better off. But we must also consider Player 1. Given (C, UA), Player 1 won’t switch to J because his payoff would be 1 rather than 3. Given (C, BA), Player 1 would absolutely deviate from C to J in order to earn 4 rather than 3. So, (C, UA) is a PSNE and (C, BA) is not. The bottom line: Both players must have no incentive to deviate strategies in a PSNE.

There are reasons that game theory as a discipline developed beyond the idea of Nash Equilibria and Pure Strategy Nash Equilibria. Simple PSNE identify possible equilibria, but don’t narrow it down from there. PSNE are strong in that they identify the possible equilibria and firmly exclude several other possible strategy combinations and outcomes. But PSNE are weak insofar as they identify equilibria that may not be particularly likely or believable. With PSNE alone, we are left with an uneasy feeling that we are identifying too many possible strategies that we don’t quite think are relevant to real life.

These features motivated the later development of Subgame Perfect Nash Equilibria (SGPNE). Students have a good intuition that something feels not quite right about PSNE. Students anticipate SGPNE as a concept that they think is better at predicting reality. But, in so doing, they try to mistakenly attribute too much to PSNE. They want it to tell them which strategies the players would choose. They’re frustrated that it only tells them when players won’t change their mind.

Regardless of whether you get frustrated by game theory, be sure to have a drink and make toast to John Nash.

*Below is the normal form for anyone who is interested.

The largest hospital system in Rhode Island, Lifespan, is trying to merge with the second-largest hospital system in Rhode Island, Care New England. Next Wednesday I’ll be on a panel discussing the proposed merger, following a panel with the Presidents of the three institutions involved (Lifespan, CNE, and Brown University). I’ll summarize my thoughts here.

Basic economics tells us that if a company with 50% market share buys a company with 25% market share in the same industry, they have strong market power and are likely to use this monopoly position to raise prices.

The real world is often more complicated, especially when it comes to health care, but in this case I think basic economics holds up well. A wealth of empirical evidence, including studies of previous hospital mergers, suggest that reduced hospital competition leads to higher prices without bringing commensurate benefits in quality or efficiency.

I think the Federal Trade Commission will almost certainly challenge the merger, and that they will likely succeed in doing so. The FTC merger guidelines more or less demand it, and current FTC leadership if anything seems to want to be more aggressive than required on antitrust. To me the biggest question is whether they will try to stop the merger entirely, or whether they would allow it to proceed subject to conditions (e.g. spin off one or two hospitals to remain independent)- I’ll be watching with interest and letting you know how it goes.

In the post-WW2 era, by many different measures the US economy performed better before about 1970 than after. You can apparently see this in many different statistics. For example, the productivity slowdown is a well-known and well-studied phenomenon. And even given the productivity slowdown, median wages don’t seem to have kept pace with productivity growth.

I think there are good reasons to doubt these particular statistics. For example, on wages and productivity see this working paper by Stansbury and Summers.

But even considering all these criticisms of the statistics, we do observe that overall GDP growth has been slower since about 1970. Why might this be?

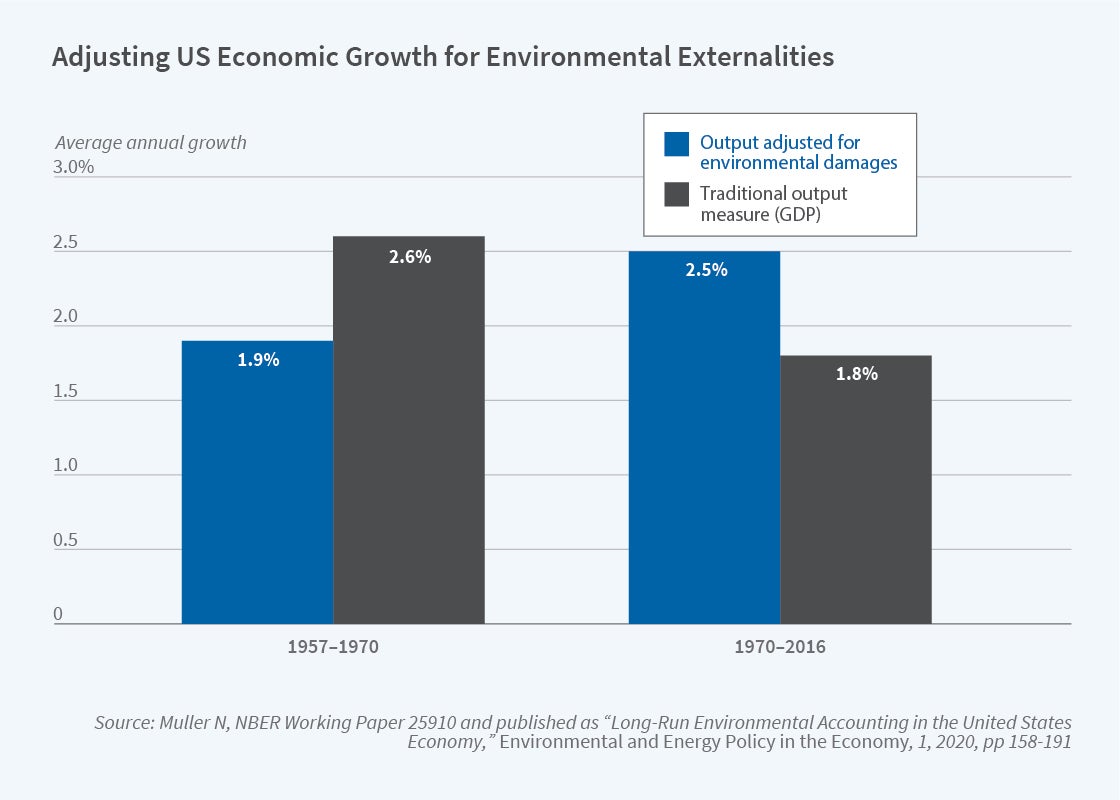

In an NBER summary of his research, Nicholas Muller argues that a big part of the GDP growth slowdown is because we aren’t including environmental damage in the calculation. This is not a new argument (Muller is an important contributor to this literature), and the exclusion of environmental damage is a well-known flaw of GDP, but Muller’s paper does a great job of quantifying how much we are mismeasuring GDP. The following figure is a nice summary of what GDP growth looks like when we consider environmental damage.

If we use the standard measure of GDP, growth indeed slowed down after 1970. If instead we augment GDP for environmental damages, the period after 1970 was actually faster! The adjustment both slows down growth from 1957-1970, and speeds up growth after 1970.

There are lots of things we can draw from this, but if the results are close to accurate, there is a clear implication: environmental regulations (such as the Clean Air Act) do reduce GDP growth, as traditionally measured. So the skeptics of regulation are partially right: regulation reduces growth!

However, this seems to be a clear case where standard critiques of GDP (as you can find in just about any Econ 101 textbook — yes, really!) need to be incorporated into the complete cost-benefit analysis of the impacts of environmental regulation.

I finally got around to opening an account at BlockFi where I can buy cryptocurrencies directly. Later I will discuss why I chose BlockFi and what I plan to do there. For now I’d like to mention one roadblock I hit in starting it up.

Signing up for the BlockFi account itself was pretty straightforward. But when it came to actually funding it, I was required to use Plaid to handle transfers of funds to and from my bank accounts – – and Plaid wanted me to tell them my full username and password that I use to log into my bank account. “No,” I said to myself, “they can’t really mean that.” But yes, they do mean that.

Armed with these credentials Plaid is able to not only pull money out of my account (like, for instance, PayPal does), but they can also login as me and have access to every financial transaction I have ever done, every check I have ever written. It’s not that I have anything interesting to hide, but this level of privacy invasion creeps me out. Also, the sad truth is that any company, including Plaid and its partners, are vulnerable to hacking, so I am not thrilled at having my bank login information floating out there in cyberspace.

On their website, Plaid is nice enough to disclose the scope of its snooping:

We collect the following types of identifiers, commercial information, and other personal information from your financial product and service providers:

Information about an account balance, including current and available balance;

Information about credit accounts, including due dates, balances owed, payment amounts and dates, transaction history, credit limit, repayment status, and interest rate;

Information about loan accounts, including due dates, repayment status, balances, payment amounts and dates, interest rate, guarantor, loan type, payment plan, and terms;

Information about investment accounts, including transaction information, type of asset, identifying details about the asset, quantity, price, fees, and cost basis;

Identifiers and information about the account owner(s), including name, email address, phone number, date of birth, and address information;

Information about account transactions, including amount, date, payee, type, quantity, price, location, involved securities, and a description of the transaction; and

Professional information, including information about your employer, in limited cases where you’ve connected your payroll accounts or provided us with your pay stub information.

The data collected from your financial accounts includes information from all accounts (e.g., checking, savings, and credit card) accessible through a single set of account credentials.

Plaid promises not to sell or rent this personal data. Fine. But even if they don’t formally sell it, they may simply give it away widely. In their words:

We share your End User Information for a number of business purposes:

With the developer of the application you are using and as directed by that developer (such as with another third party if directed by you);

To enforce any contract with you;

With our data processors and other service providers, partners, or contractors in connection with the services they perform for us or developers;

With your connected financial institution(s) to help establish or maintain a connection you’ve chosen to make;

If we believe in good faith that disclosure is appropriate to comply with applicable law, regulation, or legal process (such as a court order or subpoena);

In connection with a change in ownership or control of all or a part of our business (such as a merger, acquisition, reorganization, or bankruptcy);

Between and among Plaid and our current and future parents, affiliates, subsidiaries and other companies under common control or ownership;

[etc., etc.]

Yeesh.

I’m sure Plaid means well, but I just didn’t like the sound of all that. So, I came up with a plan: I would start up a second account at my bank, with a slightly different name and a different account number, and just give Plaid access to that one account. The only thing I would do with that account is to fund my BlockFi account, so it would not have years and years of my other financial transactions embedded in it.

In the end, that worked, but it took a more time and phone calls than I expected. Opening the new account was a surprising pain, for reasons I won’t go into here. Then, it turns out that the bank doesn’t have a category for one person having two accounts with two different logins. There was nothing I could do about it online, so I had to talk to someone at the bank who had the power to limit my login authority to my new account. This meant that I now have to use my wife’s login to access my/our old account, which is OK. But it probably would have been cleaner simply to start my new account at some different (online) bank.

Anyway, just in time for the current crypto meltdown (Bitcoin is down more than 20% from its high a month ago), my account is active and funded. More on that in future installments.