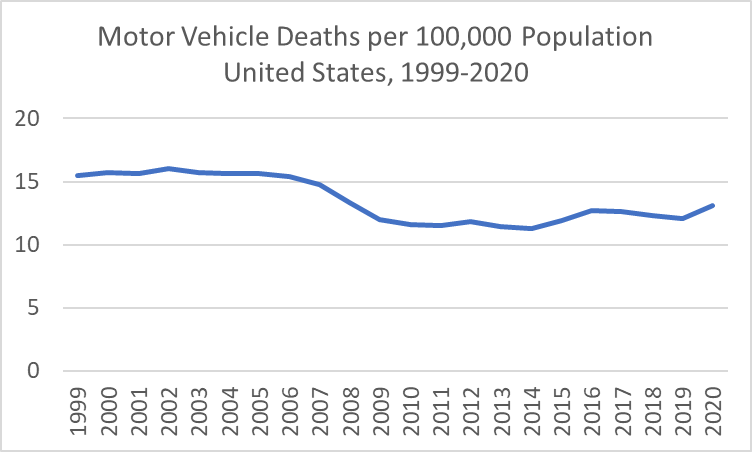

Of all the increases in mortality in 2020, one that is notable is motor vehicle accidents. There were 43,045 deaths from motor vehicle accidents, according to the final CDC data. This means motor vehicle accident was listed on the death certificate, even if it was not determined to be the “underlying cause,” though for 98% of these deaths the accident was listed as the underlying cause.

The increase from past years was large. Compared with 2019, there were over 3,000 more motor vehicle deaths, though such as increase is not unheard of: 2015 and 2016 each saw increases of around 2,500. Even so, the crude death rate from motor vehicle accidents in 2020 was the highest it has been since 2008.

If that weren’t bad enough, another theory emerged in 2020 and continues to be suggested today: that car crashes are being labeled as “COVID deaths,” artificially inflating the COVID death count. While one can find this claim made almost daily by anonymous Twitter users, one of the most prominent statements was on Fox News in December 2020. Host Raymond Arroyo said that car accidents were being counted as COVID deaths, and that due to errors like this COVID deaths could be inflated by as much as 40 percent. Senator Marco Rubio made a similar claim on Twitter in December 2021, though he was talking about hospitalizations, not deaths.

Back in 2020, many doctors and medical professionals tried to debunk the “car accidents being labeled as COVID deaths” claim, but the problem was we didn’t have complete data. Anonymous anecdotes were cited, but medical professionals tried to reassure the public this wasn’t the case or at least wasn’t widespread.

But now, we have the data! That is, the complete CDC mortality data for 2020 available through the CDC WONDER database.

What does this data show us? Short answer: there aren’t that many car accidents being labeled as COVID deaths. At most, it’s about 0.03% of COVID deaths.

Economics involves human beings making decisions. Where there are humans, drama is never absent. Hence, somewhere in the broader financial sphere, there is always some drama. The chart below displays gyrations in the exchange rate of the Turkish lira which may be fairly characterized as “dramatic”. This chart shows the lira-per-dollar exchange rate over the past six months; a higher number here means lower lira valuation.

Foreign Exchange Market Prices, Turkish Lira per Dollar. Source: TradingView.com

What is going on here? Why the spike up in November/December, followed by an even more sudden drop?

As usual, loss of value in foreign exchange goes hand in hand with domestic inflation. Inflation within Turkey for the month of December was reported to 36% on an annualized basis. Now, an orthodox economic response to runaway inflation includes raising interest rates. Higher interest rates tend to make a currency more valuable. Higher interest rates encourage people to hold onto their currency, since they are rewarded by interest on their savings. Conversely, low interest rates, especially when coupled with inflation, motivates people to spend down their money before it loses more value. In the case of emerging market countries like Turkey, high inflation/low interest drives people to exchange their local currency for more stable foreign currencies, like dollars or euros (or crypto stablecoins like Tether).

But Turkey is Turkey, and Turkey is run by the authoritarian President Erdogan. He has economic views which might most charitably characterized as “heterodox”. Erdogan claims that high interest rates actually cause inflation. His views may be influenced by the prohibition on charging interest in classic Islamic practice. The Turkish president has stated, “My belief is that interest rates are the mother of all evils. Interest rates are the cause of inflation. Inflation is a result, not a cause. We need to push down interest rates.” President Erdogan has sacked numerous treasury officials who disagreed with him, and pressured the central bank to implement four interest rates cuts in the last four months of 2021.

It seems he hopes to stimulate enough internal growth to paper over any other problems. I think there could be some merit to that notion, but the current inflation level is toxically high. Lower- and middle-class Turks find it hard to purchase necessities.

Lowering the value of your currency to make your exports more attractive has been practiced successfully by various Asian nations, but Turkey is too exposed to foreign exchange to weather such a huge drop in the value of the lira. A large part of Turkey’s recent economic growth has been funded by foreign investors, and that may dry up because of the currency instability. Turkey is dependent on imports for many essentials, including all of its energy needs, so imports have become much more expensive for Turks as their currency depreciates. Furthermore, because of the fluctuating value of the local currency, many loans are denominated in dollars or euros. This makes it burdensome for borrowers to keep up payments of interest and principal, when these foreign currencies have become more expensive.

Modern currencies have essentially no intrinsic value. Money is a big confidence game. A shopkeeper will take my dollar bill in exchange for some candy, because he is confident that some other party will in turn accept that dollar bill in exchange for something else of value. If confidence in a currency collapses, so does its exchange value.

Foreign creditors and domestic Turkish consumers were becoming more and more nervous about the prospects for the lira in late 2021, as inflation was fueling further inflationary expectation. It crashed to a record high exchange rate of 13.44 against the dollar on November 23 after the Turkish leader insisted that rate cuts would continue.

Things really started getting out of control in mid-December. Turks frantically ditched their currency in exchange for euros and dollars, which led to further devaluation of the lira. On December 21st, however, the Turkish government unleashed an innovative initiative. They offered to backstop the value of the lira deposits of Turkish residents, as long as those deposits were held in lira for a certain period of time. Besides offering interest on the deposits, the offer was to compensate depositors for any loss in value against the dollar. The intent was to motivate residents to keep their lira as lira.

Turkey’s new Finance Minister Nureddin Nebati has no real finance background; his main qualification for office appears to be a willingness to do what his boss wants. When Nebati was asked to give details of this initiative, he reportedly answered thus: “”I won’t give a number now. Can you look into my eyes? What do you see?… The economy is the sparkle in the eyes.” Hmm.

President Erdogan has said he is protecting the country’s economy from attacks by “foreign financial tools that can disrupt the financial system.” Western economists are not impressed. Market strategist Timothy Ash commented, “ More complete and utter rubbish from Erdogan…Foreign institutional investors don’t want to invest in Turkey because of the absolutely crazy monetary policy settings imposed by Erdogan.”

At any rate, this unusual measure, combined with old-fashioned central bank intervention (the Turkish central bank is believed to have used some 10 billion dollars’ worth of its foreign reserves to buy lira), seemed to stem the immediate panic. Within a day, the exchange rate thudded down from about 18 to about 13, which is roughly the level today.

It has been pointed out that it simply is not feasible for the government to backstop all relevant bank deposits against a huge currency depreciation; the Turkish government and central bank would burn through all their foreign reserves, and have to resort to printing ever more worthless lira. However, sometimes the mere promise of such a guarantee (whether or not it is practical) is enough to restore some measure of confidence, which in turn means that the currency will not collapse and thus the resources of the central bank will not be put to the test. As we said, confidence is what it is all about. We will see how this plays out.

David Friedman recently got into an online debate with Walter Block that could be seen as a boxing match between “Austrian economics” and the “Chicago School of Economics”. In the wake of this debate, Friedman assembled his thoughts in this piece which is supposed (if I understand properly) to be published as a chapter in an edited volume. Upon reading this piece, I thought it worthy of providing my thoughts in part because I see myself as being both a member of both schools of thought and in part because I specialize in economic history. And here is the claim I want to make: I don’t see any meaningful difference between both and I don’t understand why there are perpetual attempts to create a distinction.

But before that, let’s do a simple summary of the two views according to Friedman (which is the first part of the essay). The “Chicago” version is that you can build theoretical models and then test them. If the model is not confirmed, it could be because a) you used incorrect data, b) relied on incorrect assumptions, c) relied on an incorrect econometric specification. The Austrian version is that you derive axioms of human action and that is it. The real world cannot be in contradiction with the axioms and it only serves to provide pedagogical illustrations. That is the way Friedman puts the differences between the schools of thought. The direct implication from this difference is that there cannot be (or there is no point to) empirical/econometric work in the Austrian school’s thinking.

After all, all models are true if they are logically consistent. I can go to my blackboard and draw up a model of the economy and make predictions about behavior. That is what the Austrians do! The problem is that predictions rely on assumptions. For example, we say that a monopoly grant is welfare-reducing. However, when there are monopolies over common-access resources (fisheries for example), they are welfare-enhancing since the monopoly does not want to deplete the resource and compete against its future self. All we tweaked was one assumption about the type of good being monopolized. Moreover, I can get the same result as the conventional logic regarding monopolies by tweaking one more assumption regarding time discounting. Indeed, a monopoly over a common access resource is welfare-enhancing as long as the monopolist values the future stream of income more than than the future value of the present income. In other words, something on the brink of starvation might not care much about not having fish tomorrow if he makes it to tomorrow.

If I were to test the claims above, I could get a wide variety of results (here are some conflicting examples from Canadian economic history of fisheries) regarding the effects of monopoly. All of these apparent contradictions result from the nature of the assumptions and whether they apply to each case studied. In this case, the empirical part is totally in line with the Austrian view. Indeed, empirical work is simply telling which of these assumptions apply in case X, Y, or Z. In this way of viewing things, all debates about methods (e.g. endogeneity bias, selection bias, measurement, level of data observation) are debates about how to properly represent theories. Nothing more, nothing less.

It is a most Austrian thing to start with a clear model and then test predictions to see if the model applies to a particular question. A good example is the Giffen-good. The Giffen good can theoretically exist but we have yet to find one that convinces a majority of economist. Ergo, the Giffen good is theoretically true but it is also an irrelevant imaginary pink unicorn. Empirically, the Giffen good has simply failed to materialize over hundreds of papers in top journals.

In fact, I see great value to using empirical work in an Austrian lens. Indeed, I have written articles (one is a revise and resubmit at Public Choice, another is published in Review of Austrian Economicsand another is forthcoming at Essays in Economic and Business History) using econometric methods such as difference-in-difference and a form of regression discontinuity to test the relevance of the theory of the dynamics of interventionism (which proposes that government intervention is a cumulative process of disequilibrium that planners cannot foresee). n each of these articles, I believe I demonstrated that the theory has some meaningful abilities to predict the destabilizing nature of government interventions. When I started writing these articles, I believed that the body of theory I was using was true because it was logically consistent. However, I was willing to accept that it could be irrelevant or generally not applicable.

In other words, you can see why I fail to perceive any meaningful difference between Austrian theory and other schools of economic thought. For year, I realized I was one of the few to see like this and I never understood why. A few months ago, I think I put my finger on the “why” after reading a forthcoming piece by my colleague Mark Koyama: Austrians assume econometrics to be synonymous with economic planning.

I admit that I have read Mises’ Theory and History and came out not understanding why Austrians think that Mises admonished the use of econometrics. What I read was more of the domain of the reaction to the use econometrics for planning and policy-making. Econometrics can be used to answer questions of applicability without in any way rejecting any of the Austrian framework. Maybe I am an oddball, but I was a fellow Austrian traveler when I entered the LSE and remained one as I learned to use econometrics. I never saw any conflict between using quantitative methods and Austrian theory. I only saw a conflict when I spoke to extreme Rothbardians who seemed to conflate the use of tools to weigh theories and the use of econometrics to make public policy. The former is desirable while the latter is to be shunned. Maybe it is time for Austrians to realize that there is good reason to reject econometrics as a tool to “plan” the economy (which I do) and accept econometrics as a tool of study and test. After all, methods are tools and tools are not inherently bad/good — its how we use them that matters.

In middle school, I broke my leg in a soccer tournament game. I needed to go to the hospital and get extra support for the next month. Some of the workers who helped me were not highly paid, but my value of their services was very high.

Why bring this up? There has been conversation about the label “low skill” work this week. Brian Albrecht summarized the debate. Brian tangentially mentioned the “diamond-water paradox,” but I think it is worth talking more about that. Economists have a few models and stories that change the way you think about the world.

When I teach Labor Economics, we read an excerpt from Average is Over and then I explain the diamond-water paradox in class. I ask the students why diamonds cost more than water, even though water is more important. The answer can help us understand how wages get set for human workers (I say “human” because by that time we are deep in the topic of robot workers as substitutes).

I tell my students that some of the low-pay work performed by humans is extremely important. I’m still looking for the perfect illustration here. The one I use goes something like this, which is related to my broken leg anecdote… imagine if you tripped on train tracks and couldn’t get yourself out of the way of an oncoming train. How much would you pay a human to haul you to safety? Almost any human could perform the task. That service would be as valuable as a glass of water if you are about to die from thirst, which is to say that your value for it is almost infinite.

The key to understanding the market price of cleaners as opposed to the high wages for repairing Facebook code is marginal thinking. There is a lot of water, so the next glass is going to be cheap.

In writing Average is Over, Tyler Cowen is trying to understand why wages for the-less-highly-paid-skills have stagnated recently, while wages for the-highly-paid-skills are increasing along with GDP. He brings computers and technology into the conversation, as one culprit for recent changes. There is a limited supply of humans who can show up to a tech job and contribute reliably. “Programmers” are not the only highly paid class of workers, but it’s easy to see that the supply of people who are proficient with Python is limited.

I see two opposing forces in the tech world, which I have been following for a few years. First, we have boot camps, code clubs and all kinds of resources to both equip and encourage people to go into tech. I volunteer to advise a club that provides resources for female college students taking a technical route. On the other hand, lots of people who do get a foot into the door of a tech company become upset and quit.

You can read about this specific situation at this woman’s website. It seems like she made the right choice for herself. She is actually on a mission to change tech for women. I’ll reproduce the text here, in case someone can’t see the tweet: “first day at my new job! i am now a ceramicist because it lets me have no commute, make my own hours, decide the value of my work, and bring people joy. make no mistake, i wanted to code, but tech fulfilled none of that. so i hand off the baton. please fix tech while i make pots!”

The point is that she is one of many people who have dropped out of the tech workforce. Those employees who remain are pushed up toward the “diamond market price” and away from the “water market price”. Here is a blog about “burnout” survey data from 2018.

Populations in rich countries are not growing and labor force participation is down. Could the market wage for lower-skill-requirement jobs in the US rise dramatically in the next century, or at least keep pace with the wage increases that were recently enjoyed by those-with-the-capabilities-that-are-highly-valued? Marginal utility still apply, but prices will change if supply shifts.

See my old blog about Andrew Weaver who is researching skills that are in demand.

A person’s optimal choice depends on what they know. To consume more ice cream? Or to consume more alcohol? It depends on what we know about the expected utility across time. If a person thinks that alcohol has few calories, then it is understandable that they would choose to drink rather than eat. The person might be totally wrong, but they are acting optimally contingent on their knowledge about the world. (FWIW, 4oz of ethanol has 262 calories and 4oz of typical ice cream has 228 calories.)

The case is analogous for good government policy. The best policy is contingent on accessing the distribution of knowledge that’s inside of multiple people’s heads. It’s not sensible to assert that a policy is suboptimal if the optimal policy requires knowledge that neither a single individual nor all people together have. Even if the sum of all knowledge does exist, it may not be possible to access it.

Economists like to tell their undergraduate classes that it doesn’t matter who you tax. But that’s contingent on 1) identical compliance costs among buyers and sellers and 2) identical relevant information. If a tax comes as a surprise to the buyer or the seller, then it absolutely matters who is taxed.

When I was in 1st grade in North Carolina, my class went on a field trip to a Christmas tree farm. We learned a bunch about maintaining the farm and we got to choose a pumpkin to take home. At the end of our visit we took turns perusing the gift shop. My mother had generously given me a dollar to spend and I was eager to spend it (I rarely had money to spend). Unfortunately, even in the early mid-90s, most of the things in the shop cost more than $1. So, I settled on purchasing some beef jerky that cost 99 cents.

Universities have been around for about a thousand years, but for much of that time it was typical for cutting-edge research to happen outside of them. Copernicus wasn’t a professor, Darwin wasn’t a professor. Others like Isaac Newton, Robert Hooke, and Albert Einstein became professors only after completing some of their best work. Scientists didn’t need the resources of a university, they simply needed a means of support that gave them enough time to think. Many were independently wealthy (Robert Boyle, Antoine Lavoisier) or supported by the church (Gregor Mendel). Some worked “real jobs”, David Ricardo as a banker, Einstein famously as a patent clerk.

Over time academia grew and an increasing share of research was done by professors, with most of the rest happening inside the few non-academic institutions that paid people to do full time research: national labs, government agencies, and a few companies like Xerox Parc, Bell Labs and 3M. In many fields research came to require expensive equipment that was only available in the best-funded labs. “Researcher” became a job, and research conducted by those without that job became viewed with suspicion over the 20th century.

But the Internet Age is leading to the growth in opportunities outside academia, opportunities not just economic but intellectual. Anyone with a laptop and internet can access most of the key tools that professors use, often for free- scientific articles, seminars, supercomputers, data, data analysis. Particularly outside of the lab sciences, the only remaining barrier to independent research is again what it was before the 20th century- finding a means of support that gives you time to think. This will never be easy, but becoming a professor isn’t either, and a growing number of people are either becomingindependently wealthy, able to support themselves with fewer work hours (even vs academics), or finding jobs that encourage part time research. If you work for the right company you might even get better data than the academics have.

Particularly in artificial intelligence and machine learning, the frontier seems to be outside academia, with many of the best professors getting offers from industry they can’t refuse.

Strange turn of events: I declined the NSF CAREER Award. The holy grail of grants. I would have never seen this coming! Here's to starting a new adventure soon. 🙂

I think it’s great for science that these new opportunities are opening up. A natural advantage of independent research is that it allows people to work on topics or use methods they couldn’t in academia because they are seen as too high risk, too out there, make too many enemies, or otherwise fall into an academic “blind spot“.

I’m still happy to be in academia, and independent research clearly has its challenges too. But over my lifetime it seems like we have shifted from academia being the obvious best place to do research, to academia being one of several good options. Even as research has begun to move elsewhere though, universities still seem to be doing well at their original purpose of teaching students. Almost all of the people I’ve highlighted as great independent researchers were still trained at universities; most of the modern ones I linked to even have PhDs. There are always exceptions and the internet could still change this, but for now universities retain a near-monopoly on training good researchers even as the employment of good researchers becomes competitive.

As an academic I may not be the right person to write about all this, so I’ll leave you with the suggestion to listen to this podcast where Spencer Greenberg and Andy Matuschak discuss their world of “para-academic research”. Spencer is a great example of everything I’ve said- an Applied Math PhD who makes money in private sector finance/tech but has the time to publish great research, partly in math/CS where a university lab is unnecessary, but more interestingly in psychology where being a professor would actually slow him down- independent researchers don’t need to wait weeks for permission from an institutional review board every time they want to run a survey.

The latest CPI inflation data was released this morning. Mostly the new data just confirms what we’ve seen the past few months: consumer price inflation is at the highest levels in decades, and it is now very broad based.

To see how broad based the inflation is, we can look at any of the “special aggregates” that the BLS produces. CPI less food. CPI less shelter. CPI less food, shelter, energy, used cars and trucks (what a mouthful!). All of these are up substantially over the past year. The lowest number you can get is that last aggregate I listed, which excludes almost 60% of consumer spending, and even it is up 4.7% over the past year — the largest increase since 1991 for that particular special index.

Or, you can just look at food. We all have probably observed that meat prices are way up recently — about 15% over the past year. But it’s not just meat. It’s fruit, vegetables, grains, dairy… the whole darn food pyramid. In fact, there are only two food categories (hot dogs and cheese) and two drinks (tea and wine) that are actually down since December 2020.

The only categories of food and drinks in the CPI that are down since last year are hot dogs, cheese, tea, and wine

— Jeremy 'adjusted for inflation' Horpedahl 📈 (@jmhorp) January 12, 2022

I’ve covered the symbolic importance of hot dog prices before, but the fact that only four food or drink categories had price decreases are indications that food-price inflation is extremely broad-based.

Inflation is colloquially defined as, “Too much money chasing too few goods (and services)”. Supply chain constraints get talked about, and these are widely blamed for the inflation we are seeing. Of course, supply limitations play into inflation, but to focus on them is to miss the elephant in room. The primary driver of this inflation is not “too few goods”, but “too much money.”

While the headlines tend to focus on the micro elements of the supply shock (the LA port, coal in China, natural gas in Europe, semiconductors globally, truckers in the UK, etc.), this perspective largely misses the macro cause that is likely to persist and for which there is no idiosyncratic solution. This is not, by and large, a pandemic-related supply problem: as we’ll show, supply of almost everything is at all-time highs. Rather, this is mostly an MP3-driven upward demand shock. [emphases in the original]

In Bridgewater’s terminology, “MP3” is “Monetary Policy #3”, and refers to massive deficit spending combined with central bank quantitative easing. We saw this implemented in 2020-2021 when the federal government pumped out trillions of dollars of stimulus payments and enhanced unemployment benefits, and the Fed instantly soaked up the bonds that were issued to pay for these trillions. This fed/Fed combo amounts to simply printing money on an enormous scale.

Those trillions of dollars funded a huge surge in durable goods purchases. By late 2021 the supply of these goods was well above 2019 (pre-COVID) levels, and even above normal growth trendlines. However, the supply and transport systems simply could not grow fast enough to accommodate this insatiable demand. Charts below substantiate this. To focus on supply chain bottlenecks of themselves is misleading. The primary driver for this inflation has been the trillions of dollars of federal largesse. The Fed knows all this, obviously, but Jay Powell (the Chief Enabler of this deficit spending) would likely not have been reappointed if he spoke too directly about the cause of this inflation. Hence the endless prattle about supply chains.

Puzzle: the Large Hadron Collider cost $279 million per mile to build. It has 10,000 superconducting magnets, 96 tons of liquid helium for cooling, and is all custom made.

New York City's subway costs between $1.5 to $3.5 *billion* per new mile to build 🤯

This isn’t just expensive or inefficient. This is obstructive at a level only just short of an executive veto. Regardless of what sits at the top of your dream infrastructure list, this is the problem you have to solve first. Doesn’t matter if it’s high speed rail, the hyperloop, or offshore windfarms. Heck, maybe your big policy dream is universal healthcare or public education. If governments can’t build anything short of a 10X markup, then every large scale government provided solution has no value besides giving us something to argue over.

If I might put my even-more-cynical-than-usual hat on for a moment, the fact that this isn’t a top line item in every policy discussion is politically telling. This is relevant to the policy ambitions for everyone to the left of the politest anarchist you know. However, the urgency and relevance should increase exponentially as we move leftward across our political spectrum since those are the people most excited about the government actually building things. With a handful of exceptions, that’s just not what I am seeing, quite the contrary even.

Maybe it’s union indolence, conservative obstructionism, or just the quiet manifestation of all the reasons that public choice theory is actually more relevant as a left-wing school of thought than a conservative one. The fact remains that the incentives within modern politics and governance has brought us here, to a place where people want the same thing they always have: everything. And they’re willing to pay exactly as much as they always have: nothing. The difference is that our institutions used to give people incentive to bargain within the political marketplace and hammer out a deal where prices, both in dollars and political support, led to an an actual outcome where everyone ended up better off. Maybe it wasn’t as efficient as the private marketplace, but that’s almost besides the point. Sometimes the most important thing isn’t maximizing efficiency, but just managing to build the public good at all.

Instead, we seemed to have arrived at an equilibrium with enough legacy rent-seekers that the system is choking on them, with no one willing to flinch unless they continue to enjoy the previously established flow of benefits. We can try to blame this on conservative obstruction, but the fact remains that there just isn’t that much work for them to do. It’s a lot easier to tell voters they shouldn’t have to pay taxes when those taxes are disappearing into the suppurating maw of insatiable contractors, unfunded pension obligations, unplacatable union reps, and a menagerie of regulations that accomplish nothing but make a advocate 2 years removed from an overpriced BA in communications feel good about levying just one more papercut on a bloated corpse.

I have no idea if “supply-side” progressivism will gain anymore purchase than any of the other ad hoc attempts to coin a school of thought or political identity. But the idea stands, and I think it’s unescapable: if we want the government to be able to build stuff while leaving the 13th Amendment intact, they’re going to have to be able to pay market prices, and market wages, for it. Not much more, not much less.