In August, I listed the Top EWED Posts of 2025. Here are a few more highlights. This list is roughly based on web traffic, starting with the highest number of views for 2025, since the August list.

- Our breakout post for the entire year is Jeremy Horpedahl with:

The Poverty Line is Not $140,000

It has been cited in the Washington Post and the Financial Times, and shared many times.

Mr. Green has understated typical family income by something like 70 percent. Knowing this fact alone would, I think, cause him to reconsider his entire essay. But it’s worse than that: he also overstates the amount of spending required to support a family!

Jeremy wrote a follow-up the next week: Poverty Lines Are Hard to Define, But Wherever You Set Them Americans Are Moving Up (And The “Valley of Death” is Less Important Than You Think)

2. James Bailey’s biggest hit this year is:

What a great title!

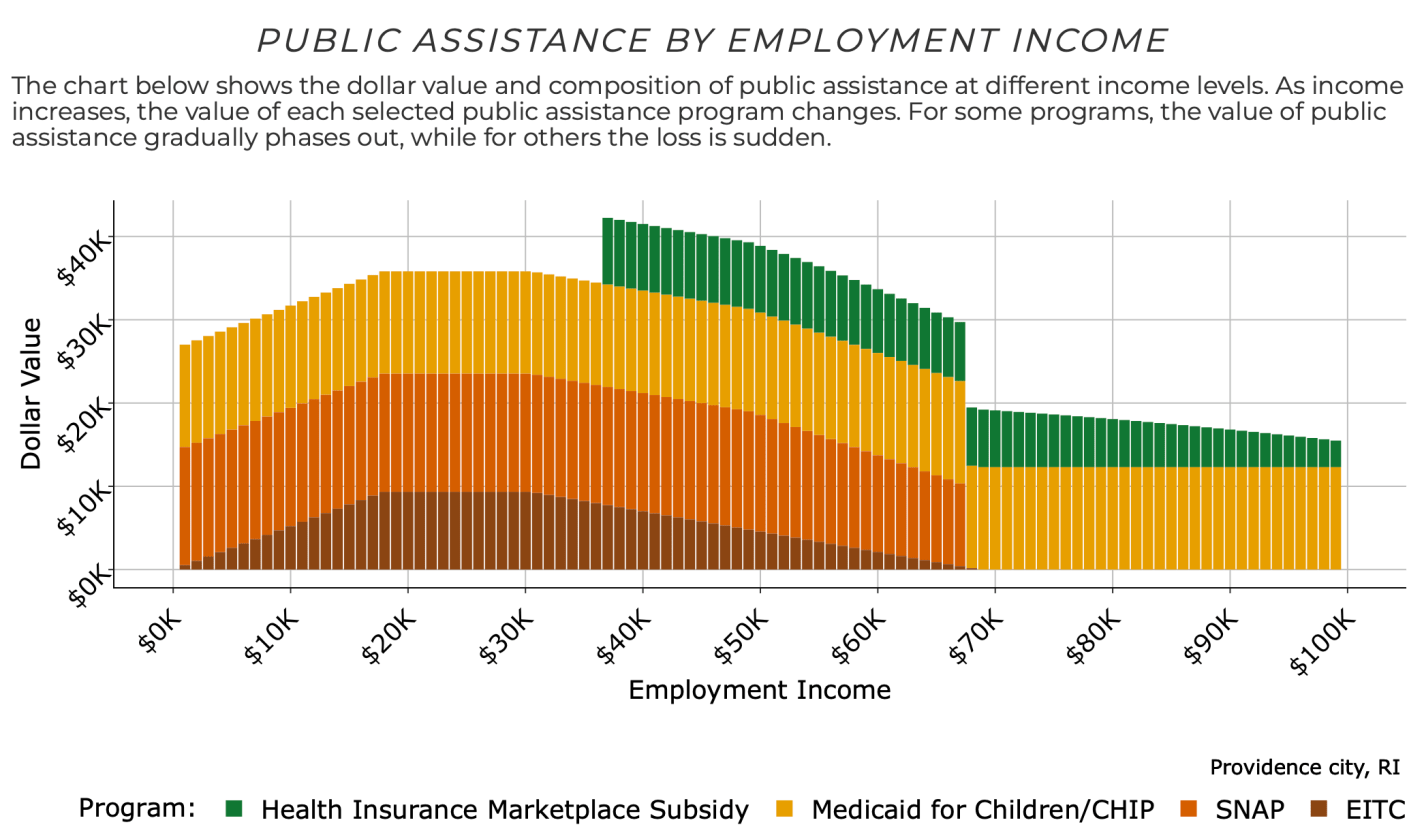

3. Many have clicked on Jeremy’s Bad Claims About Food Stamps (SNAP)

On Twitter I joked that if it is true, you should just run all of GDP through SNAP and we could be 80% richer. But my joke isn’t quite fair, because it could be true at the margin, but the effects might dissipate at some point. At what point? Well, a key assumption by USDA’s model is that the recipients of SNAP benefits have a higher marginal propensity to consume than the average household…

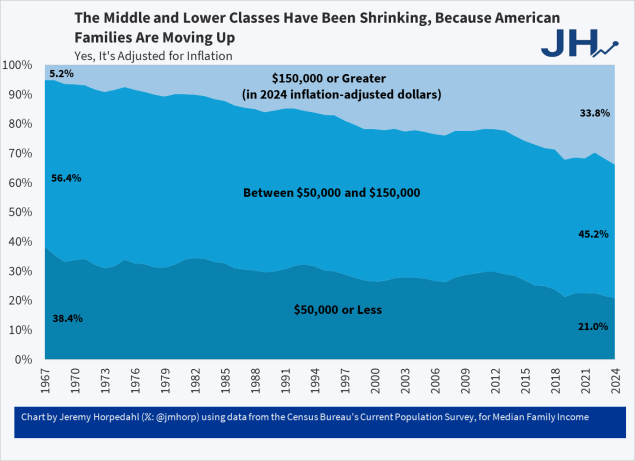

4. Did you know that One-Third of US Families Earn Over $150,000

5. Have you wondered about: What is $300,000 from “The Gilded Age” Worth Today?

6. I rarely do this in top post roundups, but I’ll mention that Mike Makowsky’s post from 2022 generated a lot of interest this year, possibly because of the rise of interest in “agents”: Why Agent-Based Modeling Never Happened in Economics

I, myself, am embarking on a research project about AI agents. More to come on that.

7. In case you struggle to accept that the world is getting better along at least some margins: The Growth of Family Income Isn’t Primarily Explained by the Rise of Dual-Income Families

8. Many people searched and found their answer from Scott Buchanan in: “Big Short” Michael Burry Closes Scion Hedge Fund: “Value” Approach Ceased to Add Value?

Funds are nearly always shut down because of underperformance, not overperformance.

9. Zachary Bartsch wrote: What is truth? The Bayesian Dawid-Skene Method

The Bayesian Dawid-Skene (henceforth DS) method helps to aggregate opinions and find the truth of a matter given very weak assumptions ex ante.

Is that what happens on a group blog? Trying to tie it all together.

10. A post from Zachary that I have shared with my students considering an economics major: What’s the Best Major to Prepare for Law School?

Money is not everything, but…

11. Not technically Jeremy’s top post, but I make this list and it made me laugh to see the title: Is Everyone Going to Europe This Summer?

Though don’t worry: not everyone went to Europe this summer, despite what social media might have you believe.

Just wait for my posts from Europe, people. I’ll get back there soon.

This cuts against the idea that all progress is just more people staring into their screens. Although, arguably, people travel for the social media engagement it generates. Sometimes I feel like my Facebook friends document their trips so thoroughly that I don’t even need to go.

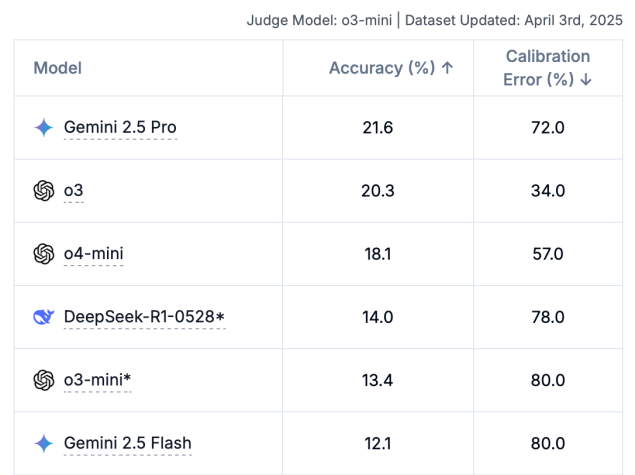

12. I posted an update to our hallucinations result: Counting Hallucinations by Web-Enabled LLMs

13. Here is a take that could come back to make me look stupid in 10 years: Is AI learning just MOOCs again?

14. We have some readers who are also classroom teachers, so here is James: Why I Started Grading Attendance

15. I endorse this message from James: LinkedIn is OK, Actually

We are a little cringe here, too.

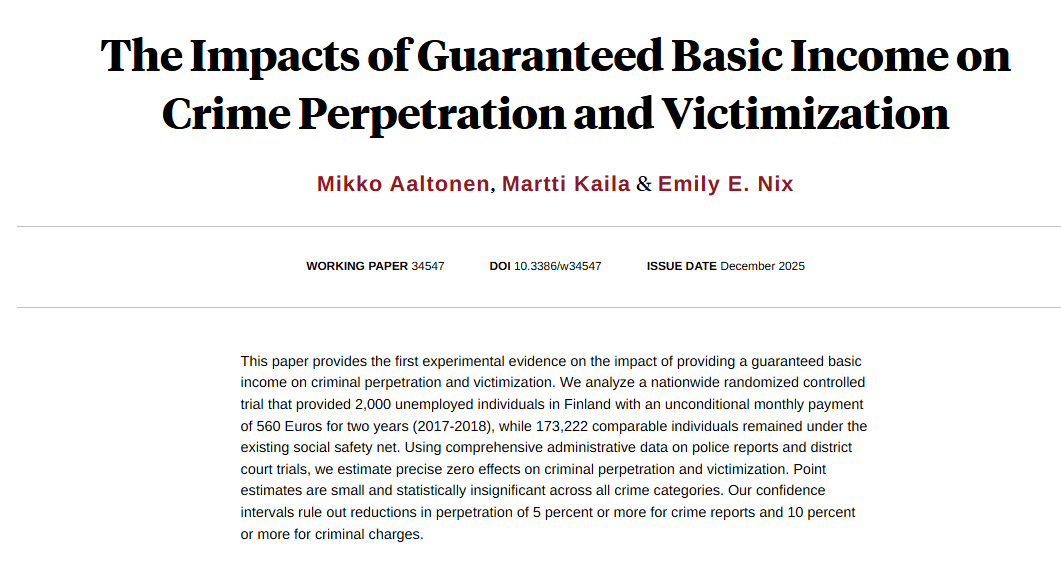

16. This post hasn’t had weeks to pick up a high views score, but Mike was one of the first to this paper, and I subsequently saw big accounts talking about it: Obviously baseline economic security matters, but…

If you asked me five years ago where a new UBI might, at the margin, have a zero effect, I would have picked a Nordic country, but still…

Our biggest source of web traffic is Google search. We get readers who click through links shared by our friends (thank you). And, something that’s way up in percentage terms is referral traffic from a certain “chatgpt.com” – 8 times more than in 2024.

Thanks to all the humans and others who read.